The battle for primacy in consumer banking has never been more consequential—or more contested. Every year, Pinwheel surveys 500 American consumers to take the pulse of the industry: who holds the primary banking relationship, what customers value, and where financial institutions are falling short. The 2026 Consumer Banking Sentiment Study delivers a clear message: consumers are frustrated, underserved in financial management, and ready to move their money to institutions that meet them where they are.

For banks, credit unions, and fintechs tracking consumer banking trends, this year’s findings illuminate a landscape defined by two major forces: a fierce competition for primary bank status anchored in direct deposit, and a tidal wave of subscription spending that consumers can’t see, can’t control, and can’t afford to ignore.

Here’s what the data says—and what financial institutions should do about it.

Banking primacy in 2026: Who owns the primary relationship?

One of the most foundational questions in retail banking is deceptively simple: who is the customer’s primary financial institution? With multi-bank behavior and ‘soft switching’ having been the trend over the past 5 years, does the concept of primacy even exist for consumers today?According to the 2026 study, 89% of American consumers identify one bank as their primary provider—a signal that despite the proliferation of fintech apps and multi-bank households, most people still anchor their financial life around a single institution.

But the definition of “primary” varies. The research reveals two dominant consumer interpretations:

- 44% define their primary bank as the account where their direct deposit lands.

- 36% go further—defining primacy as the account where they both receive direct deposit and pay the majority of their bills.

This distinction matters enormously for financial institutions. Winning direct deposit is necessary, but it is not sufficient to cement a primary relationship in the minds of a third of your customers. Those consumers expect their primary bank to be an active financial hub—not just a paycheck receptacle.

When consumers were asked which type of institution holds their primary relationship, the breakdown among the general population looks like this:

National banks continue to dominate primary banking relationships, but the 12% fintech primacy figure is notable given how recently that category emerged. Fintechs have made meaningful inroads, particularly among younger and middle-income consumers—but the affluent segment tells a different story.

Among households earning $200,000–$250,000 annually, national bank dominance surges to 67%, community banks capture 22%, credit unions hold 11%, and fintechs register zero percent. High-income households have not embraced fintechs as primary providers, even as those same platforms have captured significant wallet share among less affluent demographics. For premium-tier fintechs and community banks competing for affluent clients, this represents both a challenge and an opportunity.

The subscription economy is breaking consumer budgets—and

banks can help

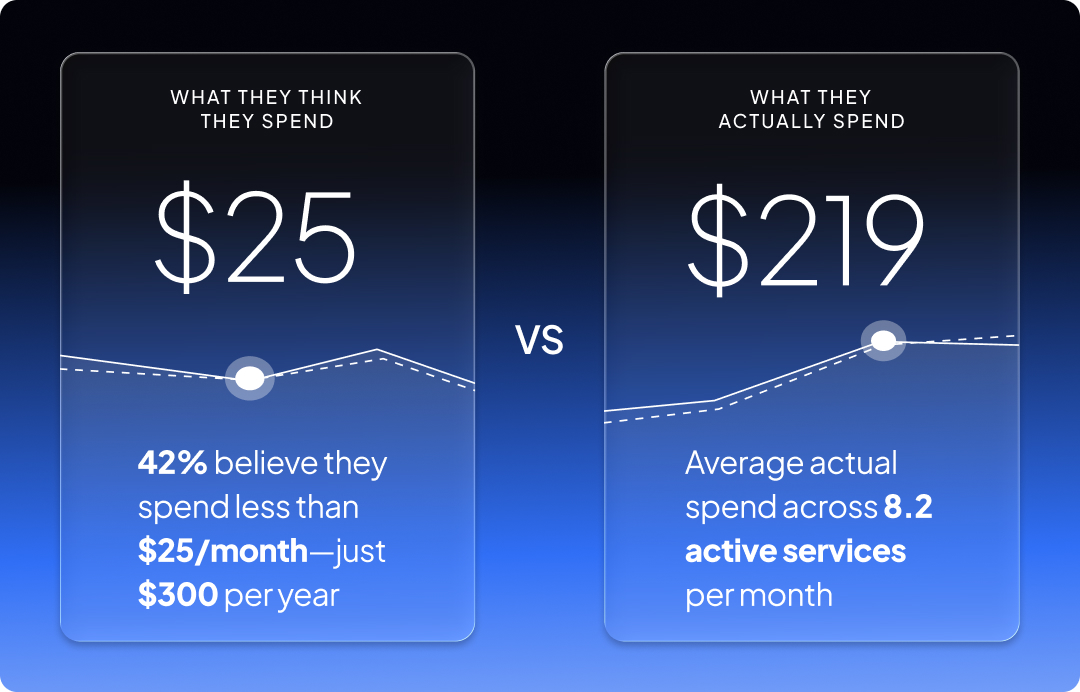

Perhaps the most striking consumer banking trend in this year’s study is the staggering gap between what Americans think they spend on subscriptions and what they actually spend. This disconnect is a defining feature of modern consumer financial behavior—and a wide-open opportunity for financial institutions.

Survey respondents were asked to estimate their monthly subscription spending. The results reveal a profound blind spot: 42% of consumers believe they spend less than $25 per month on subscriptions—just $300 per year. In reality, according to a 2026 Fortune Business Insights study, the average American spends $219 per month across 8.2 active services.

The numbers get even more striking by generation. Older consumers tend to overestimate their subscription costs—while younger consumers dramatically underestimate them:

- 19% of Gen X and 14% of Millennials report spending over $100/month on subscriptions

- Only 9% of Gen Z say the same—yet Gen Z actually leads all generations in subscription spending at $377/month

- Millennials follow at $276/month

In other words, the consumers who are most financially exposed to runaway subscription costs are the least aware of it. Gen Z and Millennials are the top candidates for subscription monitoring and management services—not because they spend the most carelessly, but because the gap between their perception and reality is the widest.

The financial consequences of this blind spot are real and measurable. According to the study:

Those dispute rates carry significant secondary consequences. Among credit union members who had a subscription dispute declined, 38% say they considered changing banks. Among households earning $100,000–$125,000 annually, that figure rises to 50%. Failed disputes aren’t just customer service failures—they are attrition events.

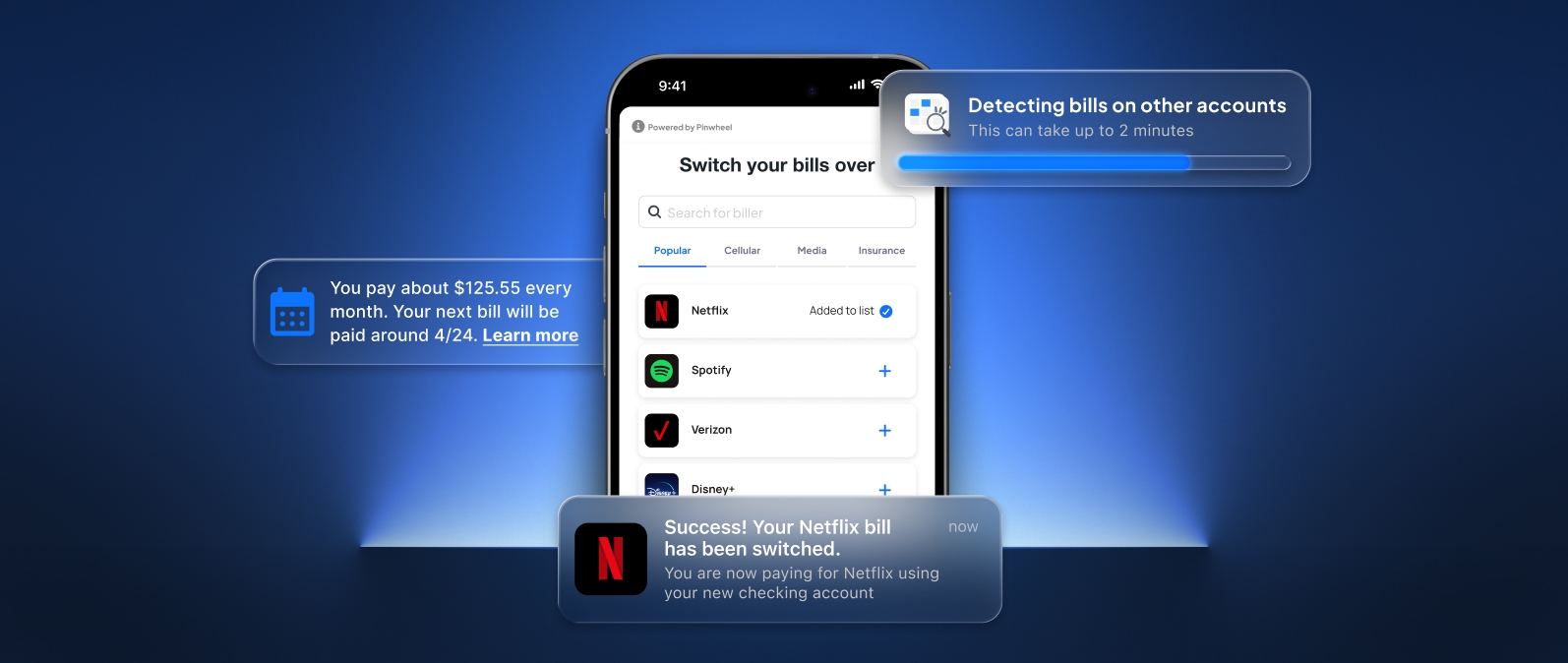

Subscription management: The feature that could redefine primary banking

If the problem is clear, so is the opportunity. Pinwheel’s research makes a compelling case that subscription management—the ability to identify, track, and cancel unwanted recurring charges—is not merely a nice-to-have feature. It is a potential driver of account primacy, bill payment consolidation, and even new revenue for banks.

Consumer demand is broad and crosses income levels:

The willingness to link external accounts is particularly significant. It suggests consumers are not just willing to consolidate bill payments—they want a unified view of their financial life, and they will grant account access to the institution that provides it. For banks seeking to deepen relationships and improve data richness, this is a meaningful opening.

Consumers will pay for premium banking—If the value is clear

One of the more counterintuitive findings in this year’s consumer banking report concerns monetization. Despite broader consumer resistance to fees, a majority of respondents say they would pay to upgrade their banking tier to access subscription management services.

Interestingly, only 38% of willing payers said they would pay $50 per year—which is actually less than the $60 annual cost of the $5/month option. The research suggests that monthly pricing creates a stronger perception of value, even when the annual total is higher. This is a textbook lesson in consumer pricing psychology and has direct implications for how financial institutions looking to increase average revenue per customer with added value services should structure premium banking tiers.

The credit card angle is equally compelling. When asked how motivated they would be to apply for a credit card that included subscription monitoring and auto-identification of unwanted charges with one-click or guided cancellation, approximately half of respondents said they would be “Very Motivated to Apply,” and 80% expressed at least moderate interest.

For card issuers and their bank partners, this data suggests subscription management could be a meaningful card acquisition lever—not just a retention feature.

Strategic implications: What banks, credit unions, and fintechs

should do now

Taken together, this year’s consumer banking trends paint a clear picture of where the industry needs to go. Here are the key takeaways for financial institutions of every size and type:

Closing thoughts on consumer banking trends in 2026

The 2026 Consumer Banking Sentiment Study from Pinwheel reveals an industry at an inflection point. National banks remain dominant, but the data clearly shows that consumer loyalty is not guaranteed—it is earned through utility, transparency, and financial intelligence. The subscription economy has created a new category of consumer pain that most financial institutions have yet to address, and the first movers who solve it will be rewarded with deeper relationships, consolidated bill payments, new revenue streams, and reduced attrition.

For banks, credit unions, and fintechs looking to understand consumer behavior in retail banking and act on the latest banking trends, the message from consumers is unambiguous: help us understand where our money is going, and we will give you more of it.

About Pinwheel | Pinwheel is the financial data infrastructure company helping banks, credit unions, and fintechs win primacy with next-generation banking experiences. Pinwheel’s industry-leading Switch Kit, enabling embedded deposit and bill switching at onboarding, delivers 2x the conversion rates of competitive solutions. The 2026 Consumer Banking Sentiment Study is based on a survey of 500 American consumers conducted on behalf of Pinwheel by Savanta in May 2026.