primacy day 1

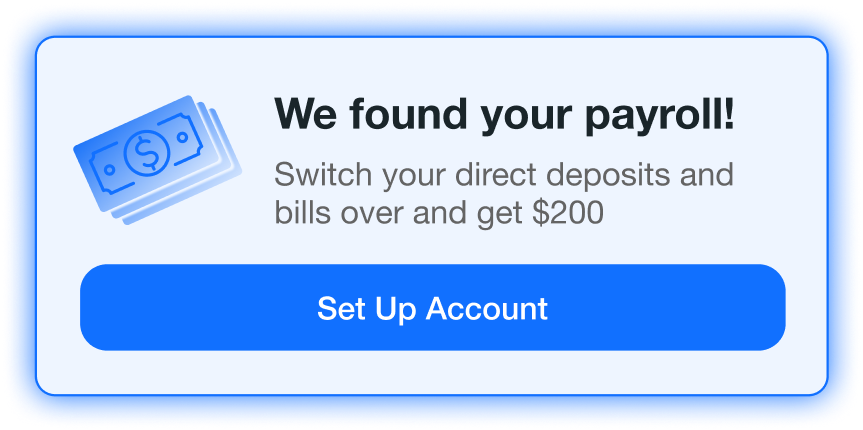

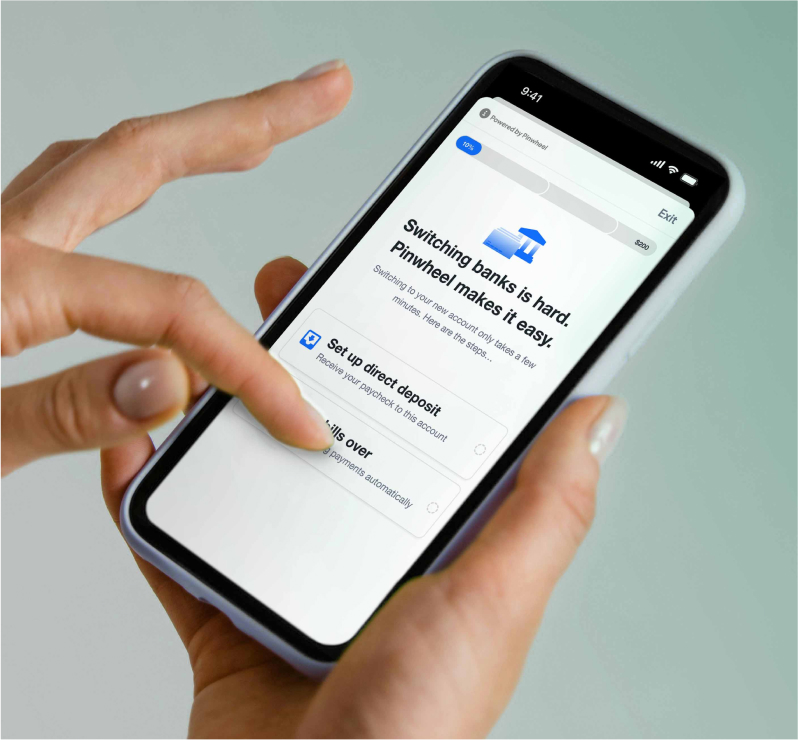

Capture customers' deposits and bills during onboarding with the Switch Kit.

Try the Switch Kit demoCapture customers' deposits and bills during onboarding with the Switch Kit.

Try the Switch Kit demo

By integrating with Pinwheel, we are ensuring our users have the best possible experience when managing their direct deposits and finances.

Pinwheel delivers 30% more switches than any other provider with our conversion-optimized solution waterfall.

Pinwheel delivers 30% more switches than any other provider with our conversion-optimized solution waterfall.

We’re constantly exploring ways to drive digital primacy. Pinwheel is building the interface that enables the onboarding behaviors we want.

Achieve 2x better conversion with the industry's only 100% credential-less switch.

The industry's best conversion rates with the only 100% credential-less solution.

Help customers cut ties with their legacy bank with in-app ACH and credit card bill switching.

Help customers cut ties with their legacy bank with in-app ACH payment and card-on-file switching.

We throw around the term “primacy” a lot, but something like Pinwheel’s Switch Kit really puts that ethos into action.

Let’s talk about how Pinwheel can deliver game-changing results for your acquisition funnel.

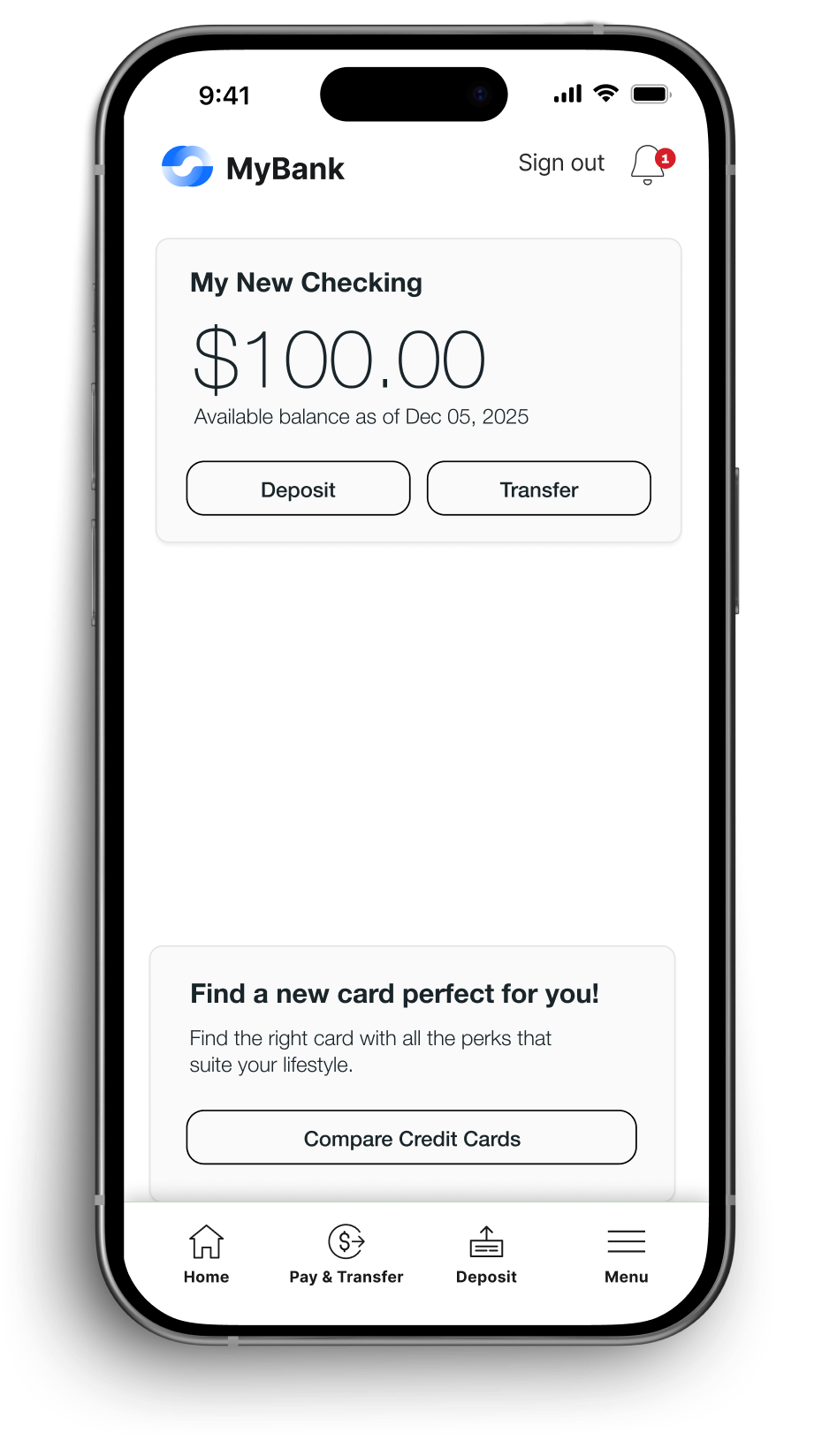

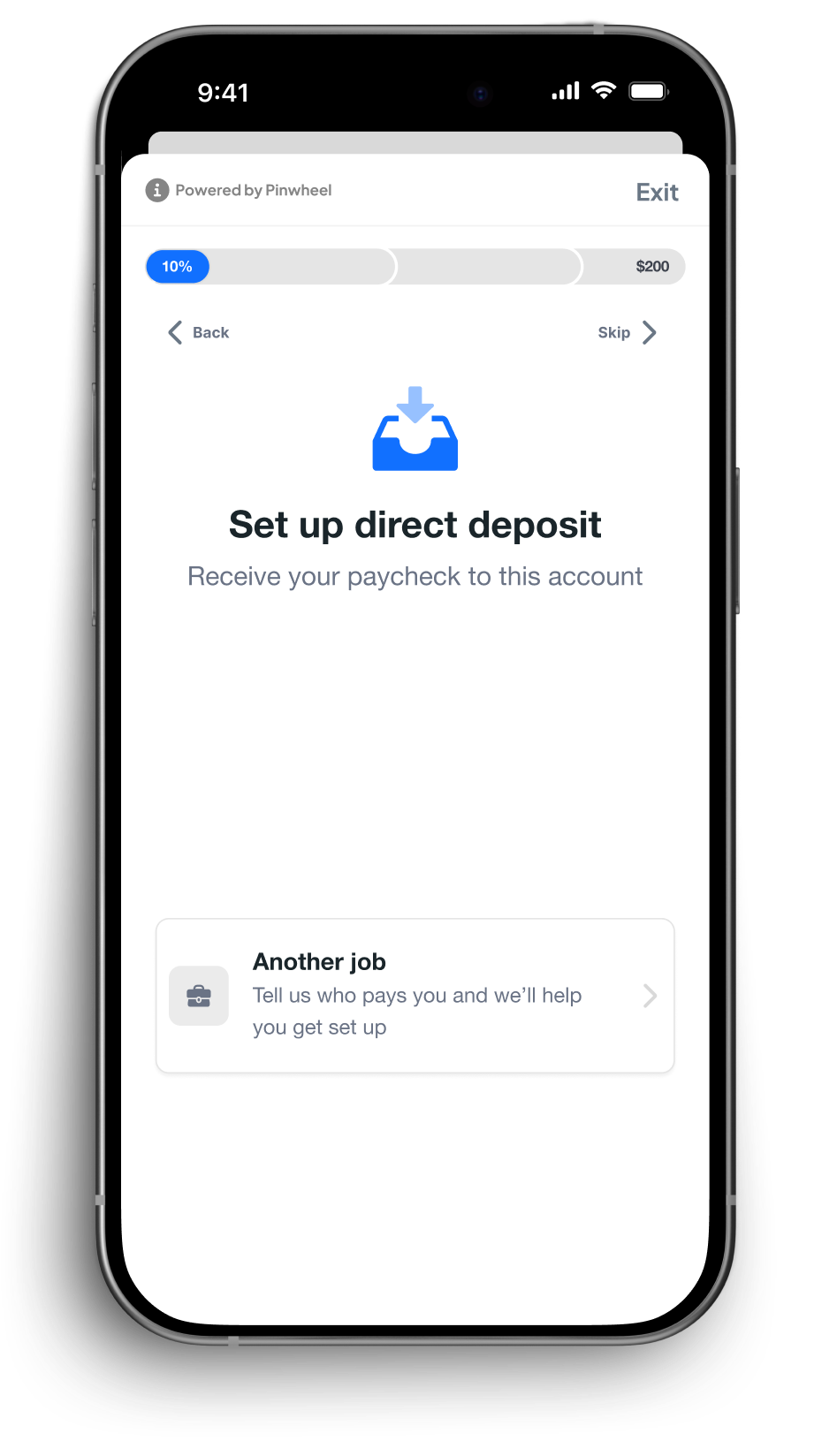

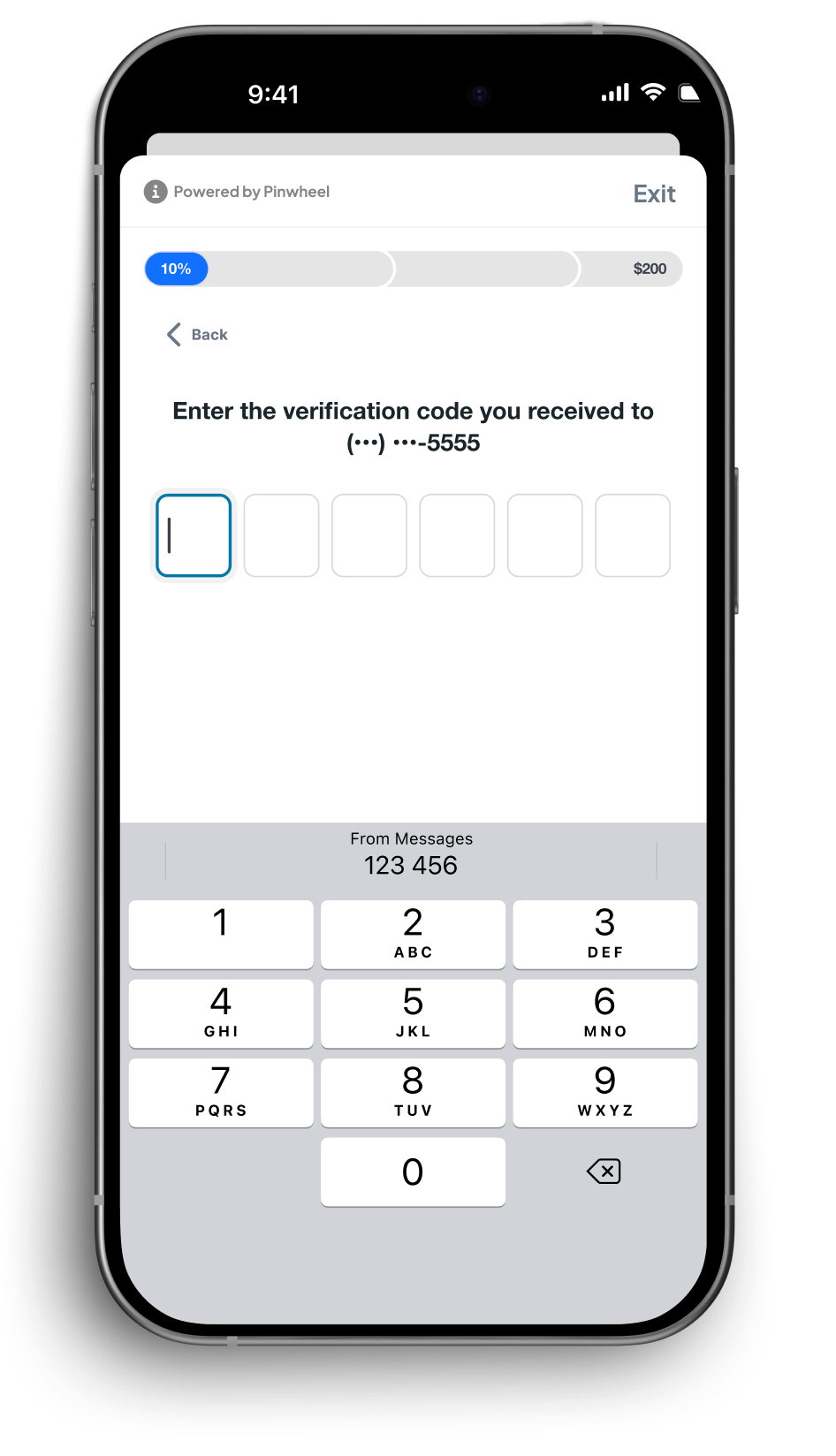

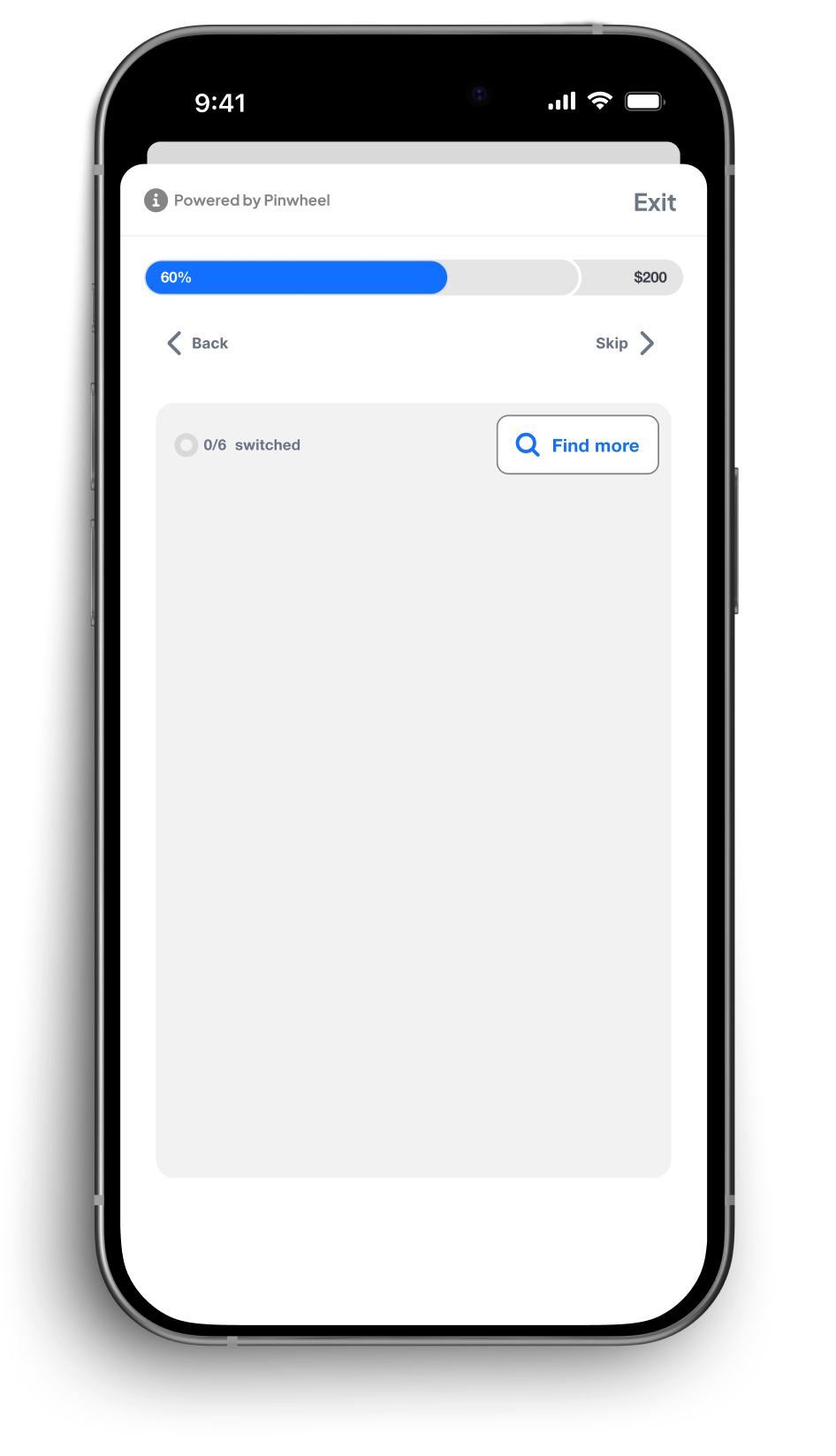

The Pinwheel Switch Kit is an integrated account activation solution that combines Pinwheel Deposit Switch and Pinwheel Bill Switch into a single, unified onboarding experience. Designed to establish banking primacy from the first day a customer opens an account, the Switch Kit guides new customers through both switching their direct deposit paycheck and transferring their recurring bill payments to the new account — in a seamless, sequential user flow.

Where Deposit Switch and Bill Switch can each be deployed independently, the Switch Kit is the recommended bundle for financial institutions seeking to maximize the speed and completeness of customer activation. The Switch Kit is available as a standalone demo and can be implemented via Pinwheel's API and SDK infrastructure.

Pinwheel Switch Kit is also available for rapid deployment on MeridianLink, Jack Henry, Candescent, Alkami/MANTL, Q2, nCino, and most bank platforms.

Opening a bank account is not the same as activating one. Research consistently shows that a large proportion of newly opened accounts remain inactive or underused — customers complete the application, receive their debit card, and then continue using their legacy bank for everyday transactions. This 'dormant account' problem is one of the most expensive challenges in retail banking: institutions have incurred the acquisition cost but receive none of the revenue benefit.

The Switch Kit solves this by attacking the two biggest barriers to full account activation simultaneously:

1. the friction of moving direct deposit, and

2. the friction of transferring recurring bills. By streamlining both processes into a single, guided onboarding experience, the Switch Kit gives new customers a clear, achievable path to making the new account their primary financial home — on day one.

Pinwheel publishes the following headline benchmarks for the Switch Kit:

• 30% more deposit switches delivered than any other provider in the market

• 80% more accurate auto-detection of recurring bills versus comparable solutions

• 40% of recurring bills identified are switched within the first 45 days of account opening

These metrics reflect the combined effect of Pinwheel's industry-leading PreMatch technology (for deposit switch conversion) and its proprietary bill detection algorithm (for bill switch accuracy). Together, they represent the strongest documented account activation performance of any comparable bundled solution currently available.

The Switch Kit is designed for financial institutions of all sizes that are actively competing for primary banking relationships. Key segments include:

1. Community Banks and Credit Unions: Institutions that compete against larger national banks and digital-first challengers benefit disproportionately from frictionless onboarding — they typically lack the brand recognition that generates spontaneous activation, making a guided switch experience a critical differentiator. Publicly confirmed customers include PenFed, EECU, ELGA, Meriwest and Delta.

2. Regional and National Banks: Larger institutions deploying the Switch Kit use it to modernize onboarding experiences, reduce branch labor costs associated with manual deposit switch assistance, and improve NPS scores at account opening. Publicly confirmed customers include KeyBank, American Express, Schwab, CBNA and Camden National Bank.

3. Neobanks and Fintechs: Digital-first companies like Robinhood — a confirmed Pinwheel partner — use the Switch Kit to give users the best possible experience when managing direct deposits and finances, accelerating the transition from 'app download' to 'primary account' status. Additional publicly confirmed leading fintech customers include Chime, MoneyLion, OnePay, Credit Karma, Varo Bank, Current and XMoney.

Pinwheel Switch Kit is available for rapid deployment on MeridianLink, Jack Henry, Candescent, Alkami/MANTL, Q2, nCino, and most bank platforms.

The Switch Kit's deposit switch component is powered by Pinwheel Prime — an AI-enabled intelligent routing engine that analyzes each consumer's eligibility in real time and routes them to the highest-converting switching experience available. The conversion waterfall uses machine learning to continuously improve and works as follows:

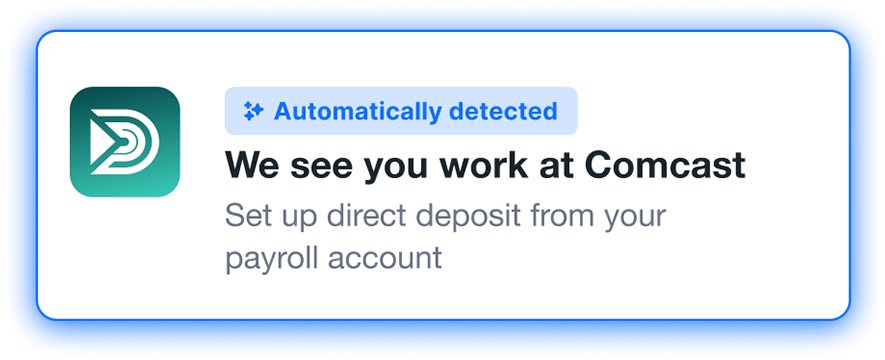

1. PreMatch: If the consumer's employer is part of Pinwheel's direct payroll partner network, PreMatch attempts to complete a credential-less switch via I-9 identity match. This requires no username or password from the consumer and delivers the highest conversion rates.

2. NativeLink: If the consumer's payroll provider is not in the PreMatch network but the consumer has saved credentials on their device, NativeLink uses device-native authentication (biometrics, saved passwords) to complete the switch without manual credential entry.

3. Forms: For any scenario not covered by PreMatch or NativeLink, Pinwheel generates a pre-filled, ready-to-submit form specific to the consumer's employer. This ensures 100% coverage — no consumer is left without a path to completion.

The waterfall approach means that every consumer who enters the Switch Kit flow receives the optimal experience for their specific situation, rather than a one-size-fits-all interface that may perform poorly for a significant subset of users. Pinwheel is aggressively expanding user eligibility for PreMatch - the highest converting deposit switching method - via additional data partnerships and machine learning.

Pinwheel has publicly disclosed partnerships with several notable financial institutions and platforms deploying the Switch Kit:

MoneyLion: The consumer finance platform integrated with Pinwheel to power direct deposit switching, with CEO Dee Choubey stating that the partnership ensures users have 'the best possible experience when managing their direct deposits and finances.’ Pinwheel was chosen after outperforming MoneyLion’s incumbent direct deposit solution provider by 30% in a head-to-head test.

Berkshire Bank: The regional bank deployed Pinwheel to drive digital primacy, with First Vice President of Digital Deposit Strategy Sara Pultman describing Pinwheel as 'building the interface that enables the onboarding behaviors we want.'

Varo Bank: This leading fintech was Pinwheel’s launch partner for Switch Kit with GM of Savings and Deposits Claudia Richter stating “We have been fortunate to partner with Pinwheel on continuously delivering a cutting edge digital banking experience for Varo’s customers. Varo customers who use Pinwheel to switch direct deposit and recurring bills hold higher account balances, make higher dollar value transactions, and become our most engaged and highest LTV customers over time.”

Technically, the Switch Kit bundles the same underlying capabilities as Pinwheel's individual Deposit Switch and Bill Switch products. The differentiation is at the UX and integration level: the Switch Kit presents both capabilities within a single, sequenced onboarding flow rather than as two separate product touchpoints.

This matters for conversion because the onboarding window is narrow and consumer attention is finite. A consumer who completes a deposit switch in one session and then encounters a separate bill switch prompt in a follow-up email is significantly less likely to complete the second action than a consumer who encounters both in a single guided flow at the moment of peak motivation (account opening). The Switch Kit is therefore not just a packaging decision — it is a conversion optimization strategy.

Not really. Pinwheel's product architecture supports omnichannel deployment across digital (web and mobile apps), in-branch (via Smart Branch), and hybrid experiences. The Switch Kit's logic — the PreMatch/NativeLink/Forms waterfall for deposit switch, and the ACH + card-on-file detection for bill switch — operates consistently across all channels.

While most new account opening activity still happens in-branch for community banks and credit unions, bank associates already have a lot to accomplish during this important interaction. Bank associates can choose to guide customers through a shared tablet or workstation, but Switch Kit is designed for the customer to self service on their own. Pinwheel’s recommended best practice is to ensure customers receive a link to complete onboarding via the Switch Kit UI during their first 45 days of tenure.

Pinwheel's standard implementations can be completed in approximately 30 days from contract signing to live deployment. Pinwheel provides developer documentation, API references, and a quick-start guide at docs.pinwheelapi.com. For institutions deploying through a banking technology platform that has already integrated Pinwheel (such as MeridianLink, Candescent, Jack Henry or Q2), implementation timelines may be shorter, as the core integration layer is already in place.

Building direct deposit switch capability in-house would require establishing and maintaining direct integrations with payroll providers — a complex, ongoing engineering investment. This is something that was attempted to no avail by the largest national banks. Pinwheel has spent years building and maintaining its network of 17,000+ payroll integrations, credential verification systems, form generation libraries, and device authentication frameworks, as well as many years optimizing this stack with machine learning. The same is true for bill switch: detecting recurring transactions accurately and maintaining merchant-specific card update workflows for 150,000+ merchants is an ongoing infrastructure commitment.

Most financial institutions conclude that the build-versus-buy calculus strongly favors using Pinwheel: the time-to-market advantage, the breadth of coverage, the elimination of ongoing maintenance burden, the benefit of years of machine learning, and the conversion optimization that comes from Pinwheel's dedicated focus on this specific problem all favor a third-party solution. Pinwheel's 30-day implementation timeline means an institution can go from zero to a market-leading activation experience in a single month — a timeline that is not achievable with an in-house build.

Banking primacy is the north star metric for most retail banking institutions — it represents the state in which a customer's financial life is anchored to a single institution. Primary customers generate the majority of retail banking profitability through higher balances, multi-product adoption, reduced churn, and greater openness to cross-sell.

The Switch Kit is designed specifically to achieve primacy on day one. By capturing both direct deposit (the income anchor) and recurring bills (the spending anchor) during account onboarding, the Switch Kit establishes the two financial behaviors most closely associated with primary banking status before the customer has a chance to fall back into existing habits with their legacy bank. This 'primacy at day one' positioning is what distinguishes the Switch Kit from generic onboarding improvement tools and why Pinwheel frames it as a strategic acquisition investment rather than a UX enhancement.