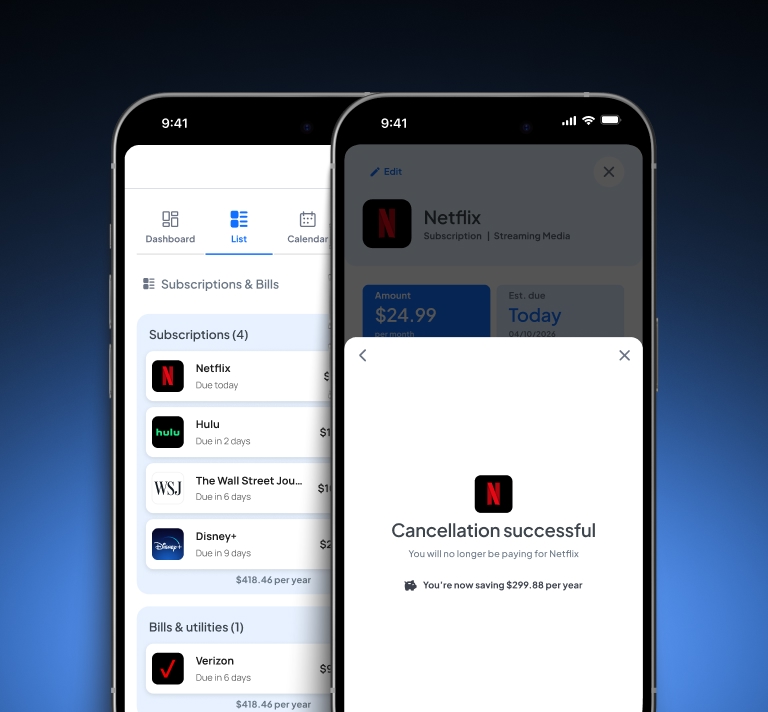

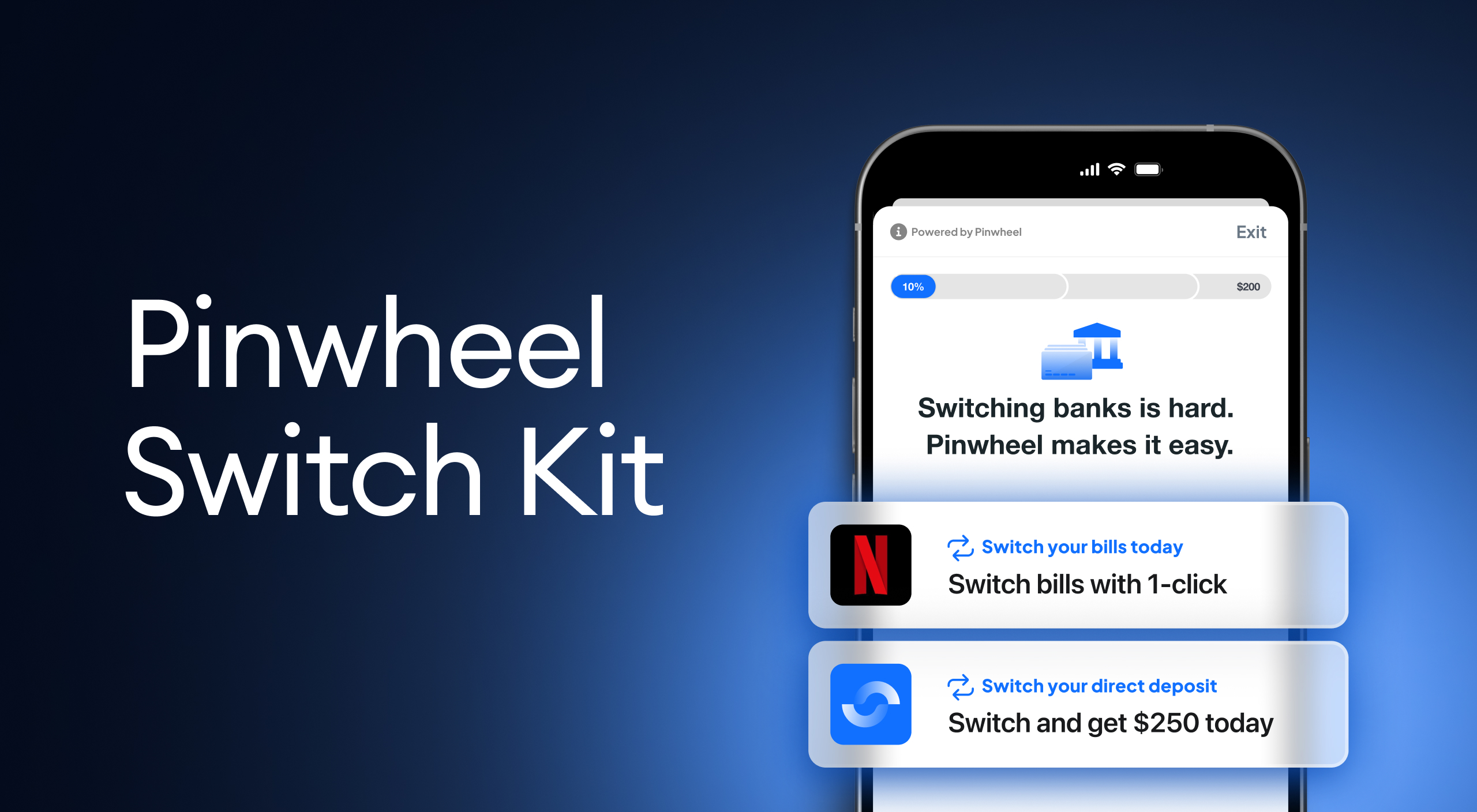

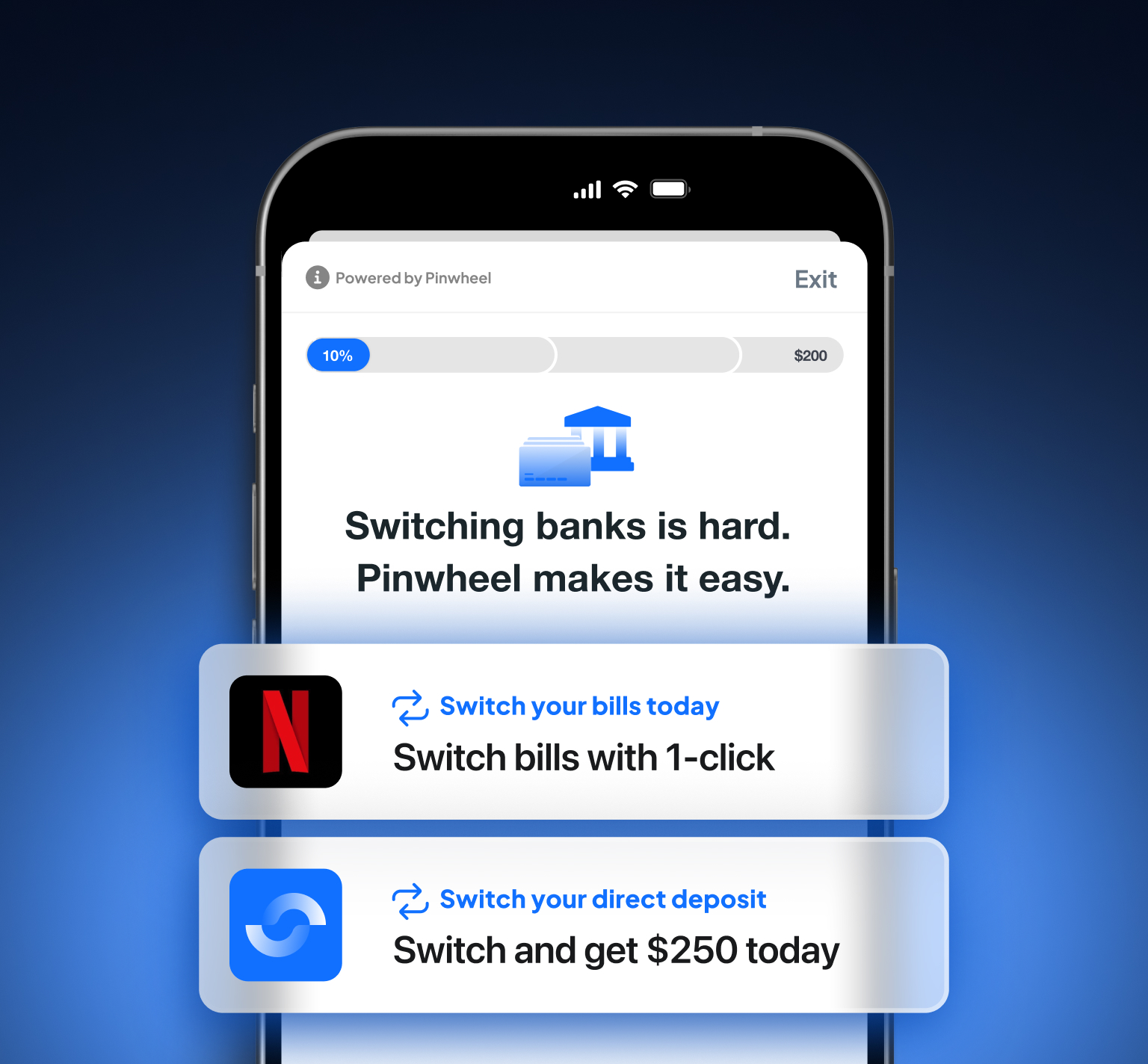

Direct deposits and primary bills are not competing priorities—banks need them both to achieve primacy, and capturing them early on in the customer lifecycle is key. The Pinwheel Switch Kit is a game-changing solution that enables users to switch their deposits and bill payments during onboarding.

Product Spotlight

Achieve primacy day one

Direct deposits and primary bills are not competing priorities—banks need them both to achieve primacy, and capturing them early on in the customer lifecycle is key. The Pinwheel Switch Kit is a game-changing solution that enables users to switch their deposits and bill payments during onboarding.

Learn more ➔