.svg)

.svg)

The popularity of earned wage access (EWA) products has skyrocketed. From 2018 to 2020 alone, the total value of wages that employees withdrew before payday nearly tripled from $3.2 to $9.5 billion.

Also known as on-demand pay and early wage access, EWA allows employees to withdraw their earnings at any time instead of waiting for a specific payday.

While flexible access to wages can benefit everyone, EWA providers can have the biggest impact on low-income households living paycheck to paycheck. In an American Payroll Association survey, almost 70% of respondents said it would be “very” or “somewhat” difficult to fulfill their financial obligations if their upcoming paycheck was a week late.

Additionally, 25% of surveyed Americans have no emergency savings. Unsurprisingly, this number is highest among those who make less than $30,000 a year. But real-time access to wages can help consumers cushion financial blows and keep them out of debt.

In addition to benefiting consumers, on-demand access to wages is transforming banking and work — employers, fintechs, and financial institutions have been busy launching new EWA services. If their recent growth is anything to go by, EWA could become a staple of future consumer finance products.

What is earned wage access and how does it work?

Traditionally, employees received their salary on a fixed pay cycle, such as on a bi-weekly or monthly basis. While this model is still prevalent, in recent years, another more flexible way of accessing wages has emerged: earned wage access. It allows employees to withdraw their wages at their own convenience, providing them with the means to cover unexpected costs or bills due before their typical payday.

On-demand pay providers initially geared the service toward low-income hourly workers in the service industry. They are more likely to live paycheck to paycheck without any savings to dip into in case of an emergency. In late 2021, numerous restaurant chains such as Arby’s and Taco Bell announced they would offer EWA, but the solution is also expanding beyond the service industry. A staffing agency for nursing homes, IntelyCare, lists EWA alongside other benefits such as a 401(k) match. In tech, PayPal recently launched an EWA program for employees in the U.S. and abroad.

In addition to employers, financial institutions have also recognized the potential of EWA. In 2022, U.S. Bank partnered with EWA provider Payactiv to enable its clients who use U.S. Bank’s prepaid card for payroll disbursements to access some of their earned wages before payday.

Likewise, PNC teamed up with DailyPay to launch PNC EarnedIt. With PNC EarnedIt, employers can offer their teams access to their earned wages at any time. Employees also don’t have to be PNC customers to use this service. Another bank that offers EWA to its corporate customers and their employees includes Citizens, which launched EWA in early 2022.

If a consumer wants to sign up for EWA, they can do so in two ways — via an employer who offers the service or a financial service provider that offers direct-to-consumer EWA.

Earned wage access as an employee benefit

Employers that offer EWA as a benefit do so by partnering with companies that connect to their payroll systems, verify the employee’s earnings, and make them available for withdrawal. An alternative is to use a payroll provider with on-demand pay as a feature.

This EWA model helps employers quickly implement an on-demand pay solution for the entire team. An additional benefit to employees comes in the form of no or reduced fees, as some employers take on the entire or partial cost of the service.

Direct-to-consumer earned wage access

Direct-to-consumer EWA is an option for everyone who doesn’t have access to on-demand pay via their employer. Because these providers don’t connect to payroll or income platforms, they determine earned wages by reviewing historical direct deposit transactions. They might also request additional information from the user to verify their employment.

How much does earned wage access cost?

EWA fees differ based on whether the user accesses the service via their employer or a direct-to-consumer solution.

Employer and payroll-integrated EWA providers may charge a monthly subscription fee (ranging from $5 to $10) or a one-time transaction fee ($1 - 5$). In this category, employers can pay for the cost of the service.

Direct-to-consumer providers charge anywhere from $1 - $9.99 per month, where EWA can be just one service in a suite of products. Per transaction, the fees range from $1 - $5, although some providers have a voluntary fee or “tip.”

Advantages of earned wage access

From fintechs to financial institutions, EWA providers have so far demonstrated the power to change the entire financial landscape, with benefits across the board.

Employees benefit from a fairer financial system

When workers have access to instant pay, they can avoid high-interest payday loans, missing bill payments, incurring overdraft fees, and going into debt. Today, 56% of Americans live paycheck to paycheck, and one in four has no emergency fund set up. The annual percentage rate (APR) on a $300 payday loan can range from 138% to 664%, which often leads to more debt and even bankruptcy. To this segment of the population, EWA can make the difference between being able to afford an unexpected expense and falling into a debt trap.

With EWA as an option, consumers can access their earnings to cover emergency expenses and avoid defaulting on an expensive loan. The percentage of payday loan borrowers who default on their loans in an 11-month period is 20%, while 64% renew. In comparison, EWA providers successfully recoup advances 97% of the time.

Overdraft fees are also a costly consequence of running out of funds before payday. In 2022, fees for going into overdraft reached $29.80. And they disproportionately affect low-to-moderate income consumers, who are 2X more likely to overdraft their bank account.

Research has shown that workers would use EWA to pay for items such as groceries, utilities, and rent or mortgage payments — not unnecessary purchases. With more control over access to their wages, employees can have peace of mind regarding their financial security and steer clear of predatory loans, protecting their financial health. And they’ll be able to better focus and be more productive at work which will also benefit employers.

Financial service providers can draw in more consumers

Just as companies use EWA to recruit new employees, so can financial service providers to attract more clients.

In recent years, neobanks and other consumer-facing fintechs have ramped up competition in the financial industry, increasing the pressure of launching innovative products to retain existing and draw in new customers.

While employer interest in offering on-demand pay is rising, not every company will find it feasible to implement, which opens doors to legacy institutions and fintechs to step in.

By launching EWA products, financial service providers can service a considerable consumer group — 77% of Americans would use EWA if their financial institution provided it. And more than half (56%) of EWA users began using the service in the last 12 months, a clear indicator of the service’s growing demand.

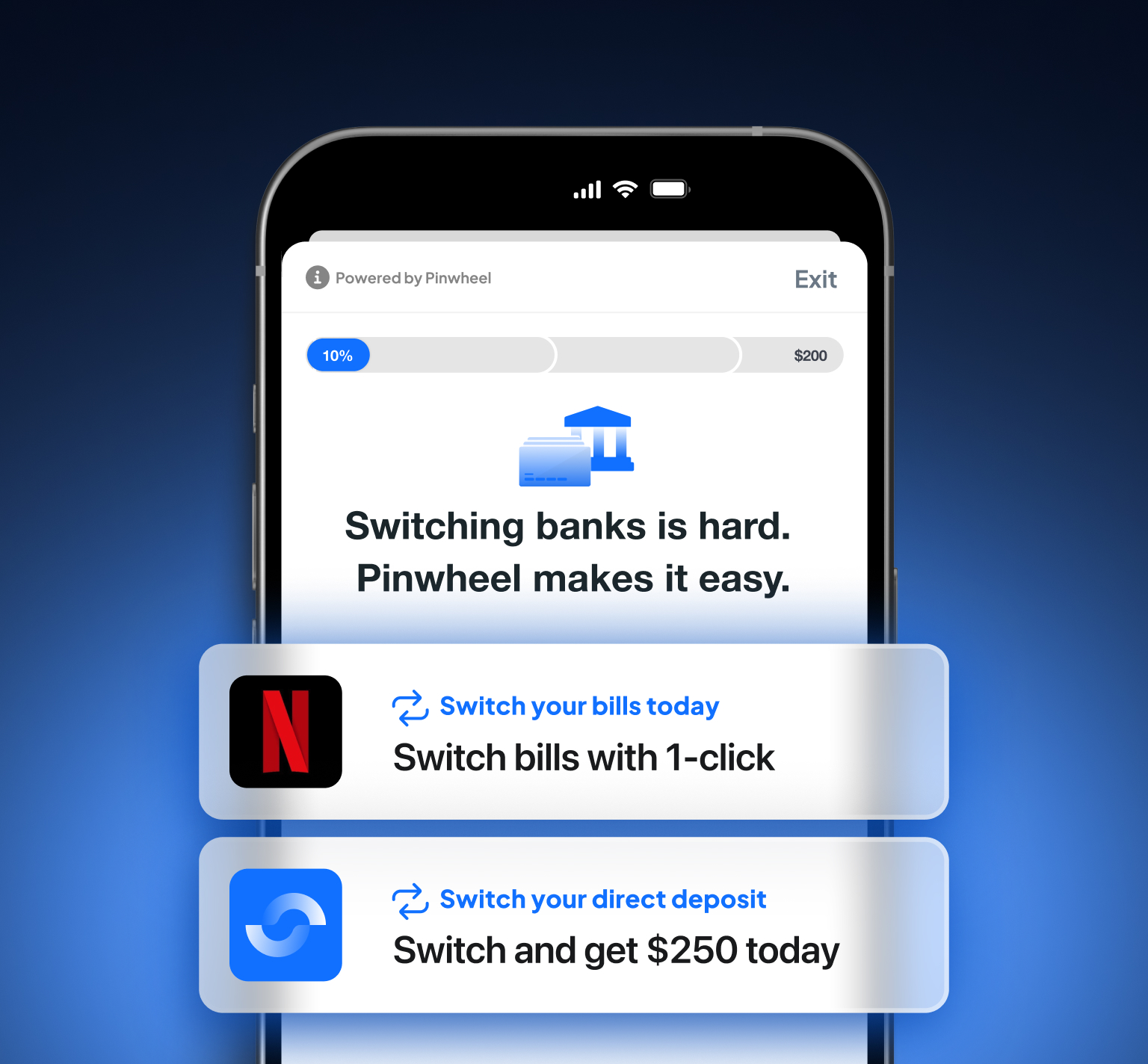

Acquire more direct deposits with earned wage access

With EWA being in such high demand, financial service providers can use it to boost their direct deposit strategy. For example, a customer switching their direct deposit would make them eligible for EWA. And if they deposit their entire paycheck (versus only a portion), they can unlock more wages. This is a major opportunity for banks and fintechs, as customers who direct deposit into their account have a 32x greater lifetime value than those who do not.

Pinwheel Earnings Stream enables companies who wish to expand into the EWA space to do so quickly, compressing 6+ months of work into 6 weeks. It allows financial providers to access an employee’s accrued and projected earnings in a given pay period, enabled by our real-time access into income and employment data from payroll systems. Then, they can advance the funds to the customer and easily recoup them on payday via the direct deposit.

Ready to follow in the footsteps of companies like Cash App and Acorns? Contact us to learn more about how Pinwheel’s solutions can take your product to the next level.