.svg)

.svg)

Credit unions hold a powerful trust advantage over national banks. New consumer data reveals what members actually need from their credit union to maintain that trust advantage.

Credit unions occupy a uniquely enviable position in American financial services. They are member-owned, mission-driven, and widely trusted. They offer better rates, lower fees, and a genuine commitment to financial wellness that no national bank marketing campaign can credibly replicate. By almost every measure of values alignment, credit unions should be winning.

And yet the numbers tell a more complicated story. As of Q4 2025, the median credit union reported a membership decline of 0.5%, according to the National Credit Union Administration. More than half of all federally insured credit unions had fewer members at year-end than a year prior. Membership growth in Q1 2026 slowed to just 1.81%, well below the five-year average. Smaller institutions—those under $50 million in assets—are feeling it most acutely, with some reporting membership declines as steep as 7.8%.

The trust is there. The mission is there. What too often isn’t there is the digital experience that today’s banking consumer expects as a baseline. Pinwheel’s 2026 Consumer Banking Sentiment Study, combined with a growing body of industry research, makes clear that credit unions are sitting on enormous untapped potential—and that the window to act is narrowing.

The primacy problem: Credit unions hold 17%—but should hold more

When Pinwheel asked 500 American consumers to name their primary banking provider, 17% pointed to a credit union. That trails national banks at 55% and is essentially tied with community banks at 15%. Fintechs, despite their comparatively minimal length of time operating as primary account providers, are already at 12%.

That 17% figure understates both the credit union sector’s reach—144.7 million Americans hold credit union memberships—and its missed opportunity. Having a membership relationship is not the same as being someone’s primary financial institution. Tens of millions of consumers maintain a credit union account as a secondary relationship while routing their direct deposit and bill payments elsewhere. And it is that primary relationship—where the paycheck lands and the bills get paid—that determines long-term member value.

Pinwheel’s research establishes two key markers of true primacy: being the account that receives direct deposit (cited by 44% of consumers), and being the account that receives direct deposit AND handles bill payment (cited by 36%). Credit unions that capture membership but not the direct deposit and bill pay relationship are operating at the margins of their members’ financial lives.

The dispute data from the 2026 study sharpens the picture further. Among credit union members who had a subscription charge dispute declined, 38% say they considered changing banks. That is a meaningful attrition signal, and it points to a specific vulnerability: when members encounter friction or failure at a moment of financial need, the primary relationship is at risk—regardless of how long they’ve been a member.

The digital gap is measurable—and growing

The competitive challenge facing credit unions is not abstract. A 2025 McKinsey analysis of more than 60 U.S. credit unions found that credit unions generate roughly 20–25% fewer online product conversions than banks of similar size, that members spend less time exploring products or completing applications digitally, and that younger members are less likely to see a credit union as their primary financial provider because they prefer mobile-first, frictionless experiences.

Industry surveys reinforce the urgency. According to Cornerstone Advisors’ research, cited by The Financial Brand, 62% of credit union executives ranked new member growth among their top three concerns in 2025—up from 41% in 2022, a 51% increase in just three years. The problem is not that credit union leaders don’t see the challenge. It is that seeing it and solving it are two different things.

Cornerstone also identified a troubling execution gap: roughly one in four credit unions planning technology initiatives fails to deploy them. The same pattern appeared across online banking platforms, digital account opening tools, and CRM systems over multiple years. Ambition has been outpacing action.

Meanwhile, consumer expectations are not waiting for credit unions to catch up. CSI’s 2026 Banking Priorities survey found that credit unions are more than twice as likely as community banks to prioritize digital account opening and onboarding—a sign that the gap is broadly understood. But awareness of a gap is not the same as closing it.

What members are telling you (whether you're listening or not)

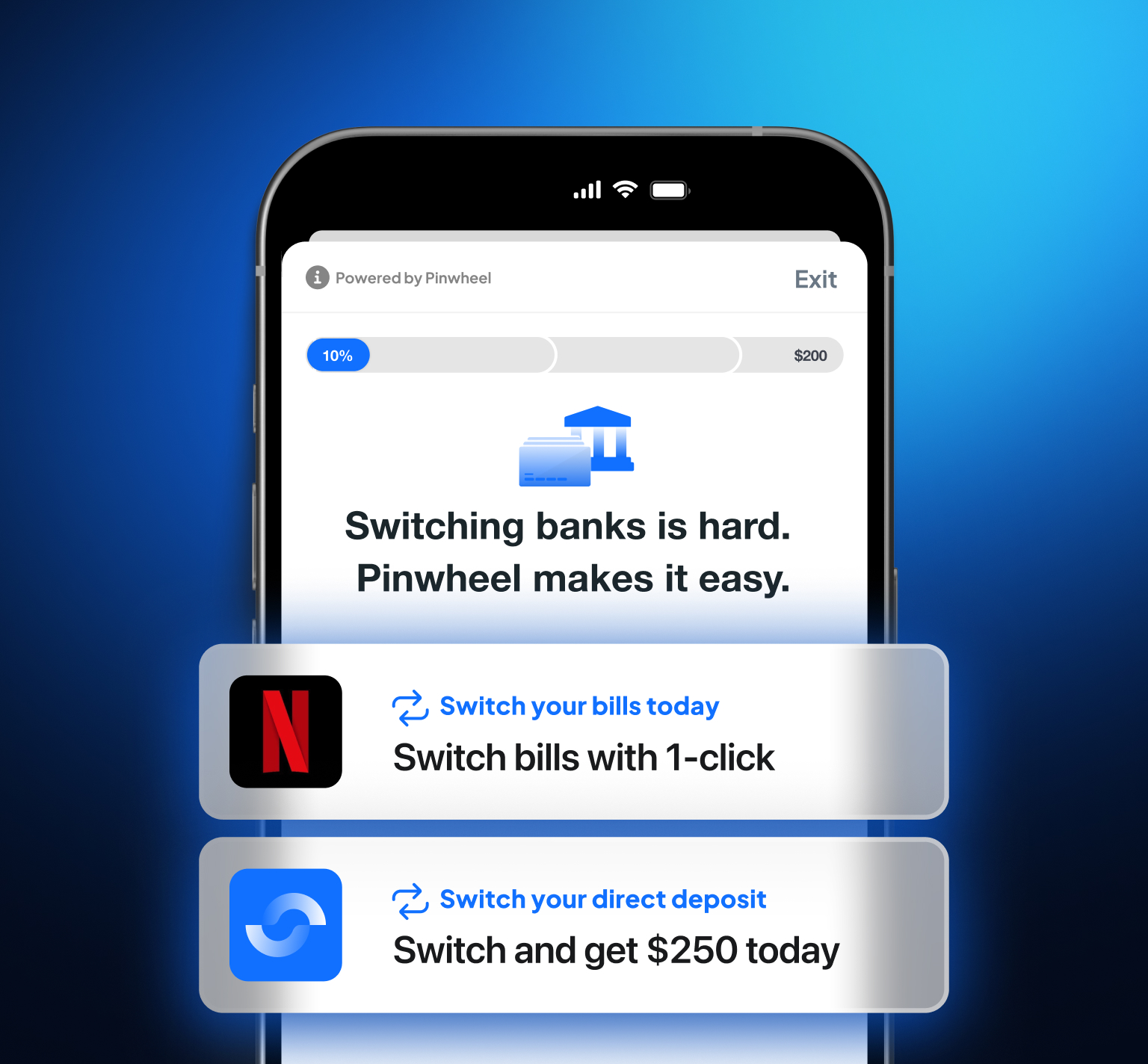

Pinwheel’s 2024 consumer research found that 73% of Americans had considered switching banks in the prior 12 months. For credit unions, that restlessness is both a threat and an opportunity. Prior Pinwheel research also showed that the top three barriers to switching were fear of the direct deposit transfer process, lack of an easy way to update payroll routing, and the hassle of migrating recurring bill payments. These are not abstract concerns—they are exactly the friction points that modern solutions like a direct deposit switching API and a bill switch API are purpose-built to eliminate.

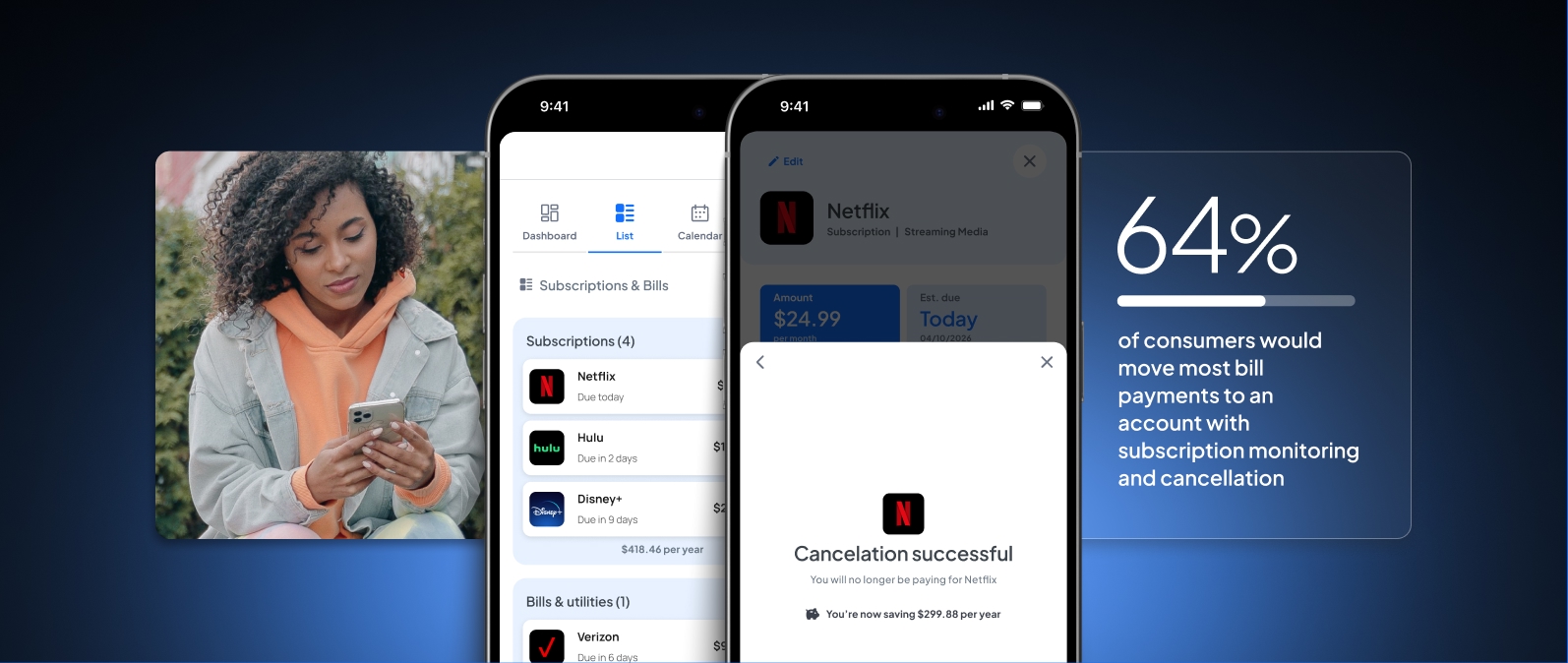

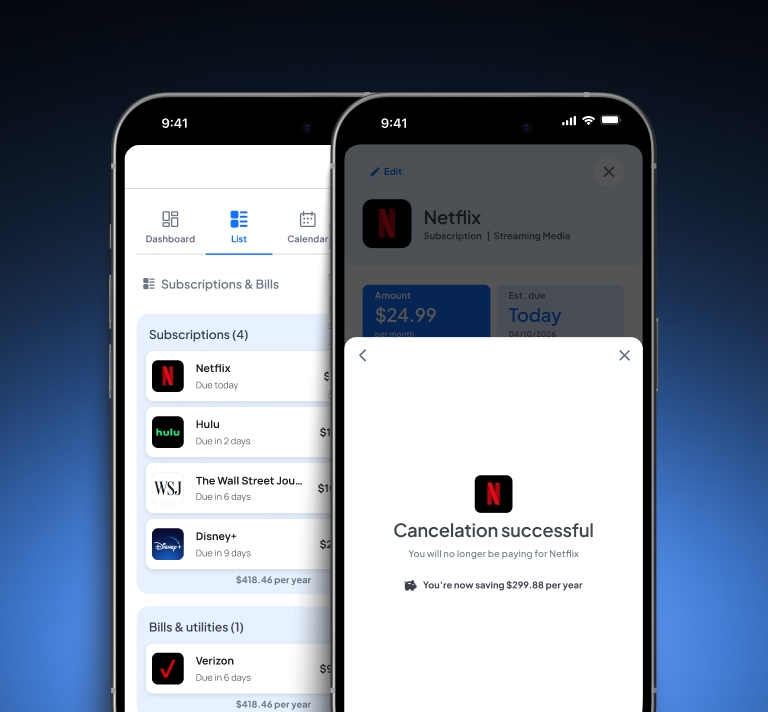

The 2026 data reveals a new and equally urgent pain point: subscription management. Pinwheel’s annual study found that 58% of consumers have disputed a charge tied to an unwanted subscription. Among credit union members specifically, 38% say they considered leaving after a dispute was declined. This is a real and recurring churn trigger—one that does not require a product overhaul to address, but does require action.

The appetite for subscription management tools among the general population is significant:

For credit unions, this data carries a specific implication. Subscription management is not just a fintech feature—it is a member financial wellness tool. And financial wellness is the core of the credit union mission. Offering members visibility into where their money is going, helping them cancel forgotten services, and protecting them from overdrafts caused by unwanted charges is exactly what a member-owned institution should be doing. It is also, as the data shows, a proven driver of primary banking consolidation.

The modernization roadmap: 5 things every credit union should be doing

The path forward for credit unions is not about becoming a bank. It is about combining the values and trust that make credit unions irreplaceable with the digital capabilities that modern consumers require. Here is what that looks like in practice:

1. Make digital account opening instant and frictionless. In 2026, if a prospective member cannot open an account on their phone in under five minutes, many simply won’t. Prior Pinwheel research found that 70% of all consumers—and 81% of those earning over $150,000—said they would be more likely to switch banks if they could transfer their direct deposit digitally in seconds. The account opening experience is the first impression. It must be fast, mobile-optimized, and require no branch visit or paper form.

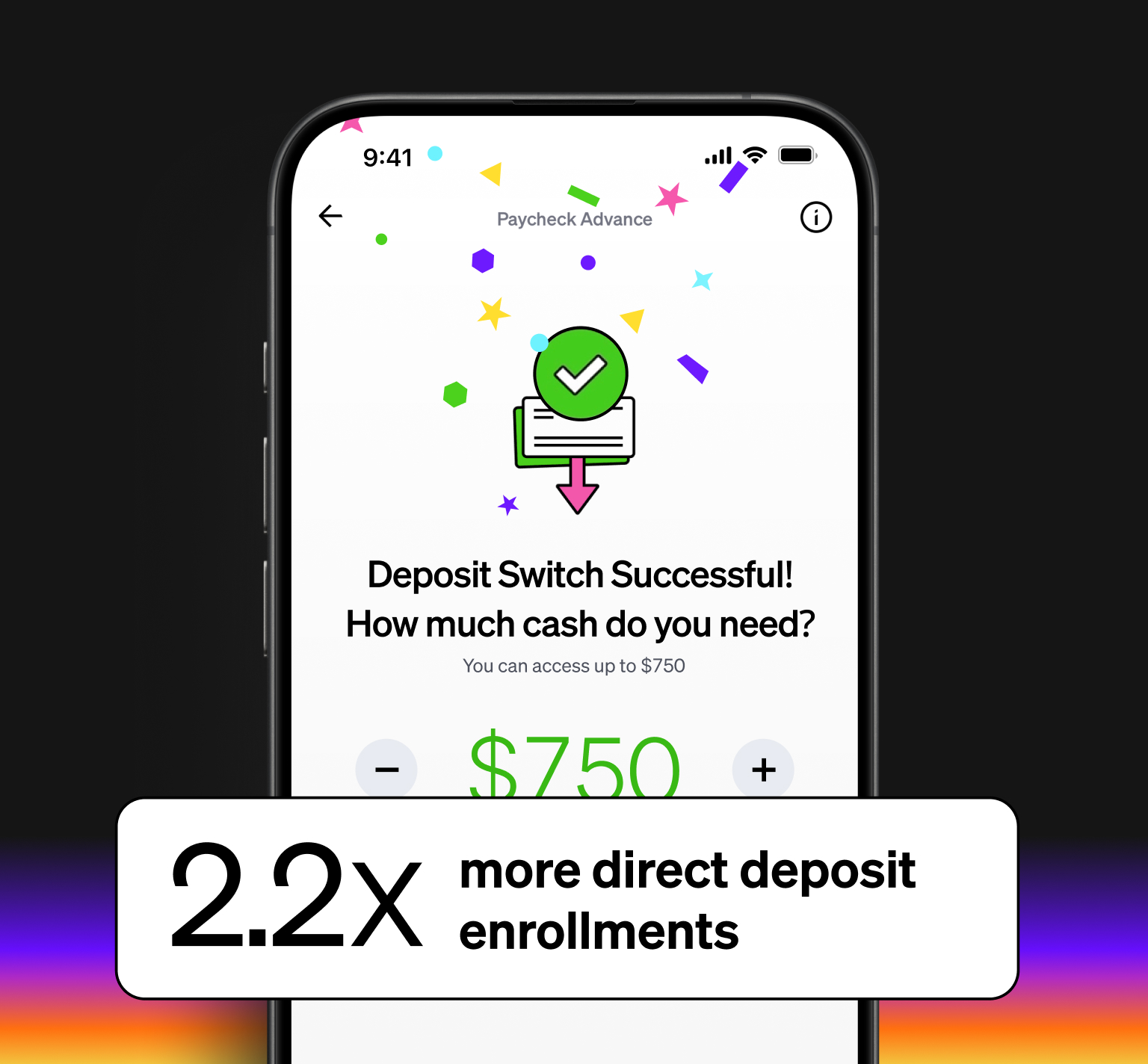

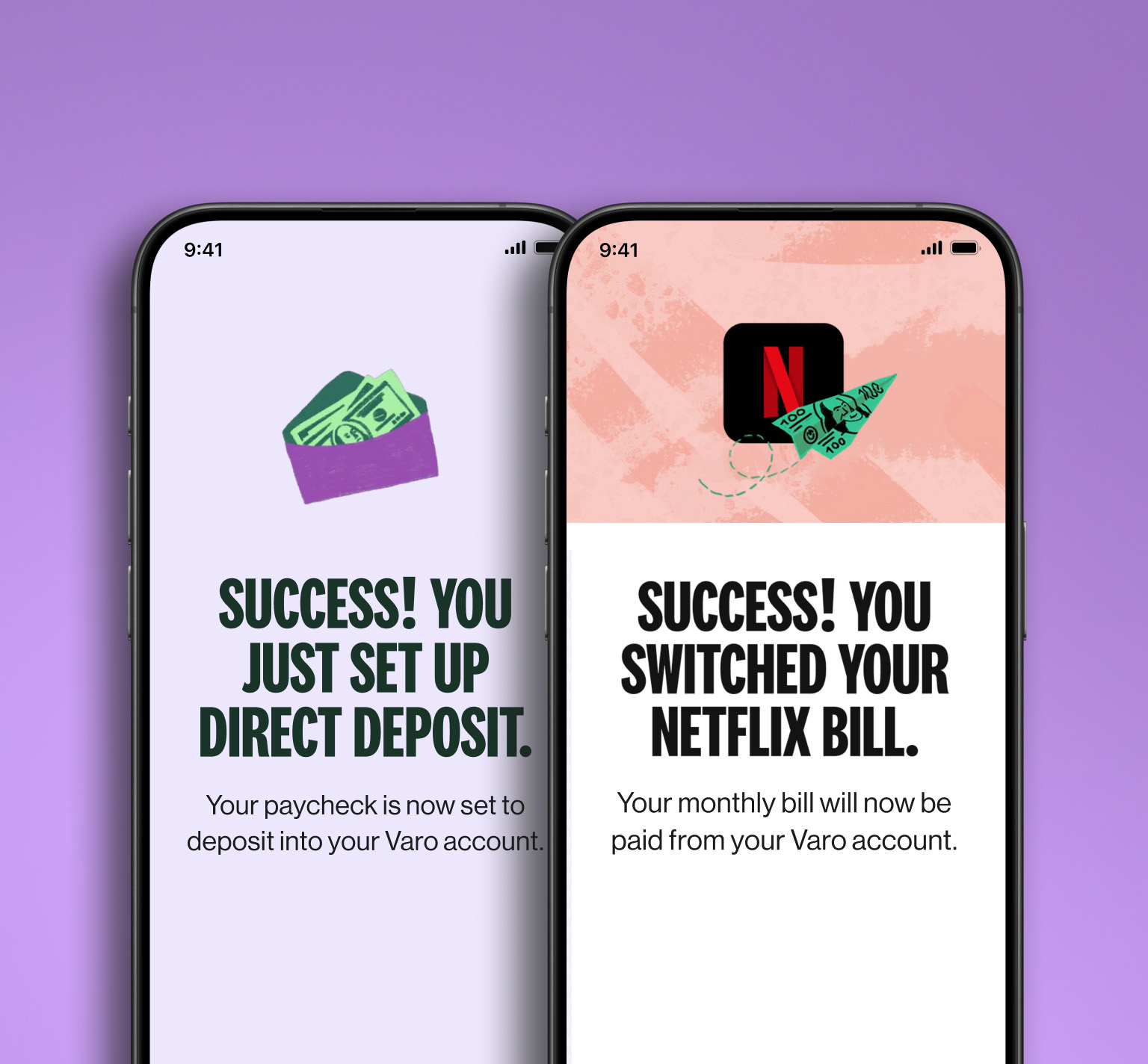

2. Build direct deposit switching into the onboarding journey. The single largest barrier to credit union primacy is not brand awareness or rates—it is payroll inertia. When members join but don’t reroute their direct deposit, they remain secondary. Credit unions should embed a direct deposit API into their new member onboarding flow—enabling payroll-linked switching in seconds rather than days—and eliminating the manual friction that causes 40% of new accounts to go dormant, per Pinwheel’s 2024 research. A well-integrated direct deposit switching API removes the single biggest reason members never fully activate.

3. Launch subscription management as a member financial wellness feature. Subscription monitoring and cancellation tools are in demand across all demographics, and the willingness to pay for and switch banks for them is documented. The most effective implementations pair subscription intelligence with a bill switch API that makes migrating recurring payments to a new account fast and frictionless. For credit unions, framing this as a financial wellness benefit—consistent with the cooperative mission—is more authentic than it would be coming from any national bank. The data shows 64% of consumers and 74% of Millennials would consolidate bill payments to an account that offers this. A bill payment switching API turns that intent into action, making the credit union the hub of the member’s financial life rather than a peripheral account.

4. Move AI beyond the chatbot. Chatbot deployment reached 45% of credit unions by 2025, up from 3% in 2019—real progress. But as Cornerstone’s research notes, this is a starting point, not a finish line. The next frontier is machine learning to predict needs: identifying members who are approaching overdraft, flagging suspicious subscription charges before disputes occur, and proactively surfacing relevant products at moments of financial decision. Credit unions that invest in predictive AI will deliver on the personalized service promise they’ve always made.

5. Address the dispute experience before it becomes an attrition event. With 38% of credit union members considering leaving after a declined dispute, subscription-related charge disputes are an underappreciated attrition lever. Credit unions should audit their dispute resolution processes for recurring-charge claims and explore whether proactive subscription monitoring can reduce dispute volume altogether. A member who never has an unwanted charge in the first place has no reason to dispute—or to leave.

The national banks are not sitting still. Neither are the fintechs. But credit unions have something neither of those competitors can manufacture: a genuine, structural reason to put members first. The institutions that deploy a direct deposit API to eliminate switching friction, use a bill switch API to consolidate member bill payments, and layer in subscription intelligence to protect member finances will find that the 144 million Americans who already hold credit union memberships are a powerful foundation for lasting primacy.

The members are there. The mission is there. Now the digital experience needs to catch up.

Pinwheel is available for rapid deployment on the banking technology platforms serving the credit union community, including MeridianLink, Candescent, Jack Henry, Alkami, Terafina, Lumin, BankJoy, Narmi, MANTL, Blend and many more. Check out our partners page or book a meeting to reserve your implementation slot.

Sources: Pinwheel 2026 Consumer Banking Sentiment Study (n=500 U.S. consumers); Pinwheel 2024 Consumer Bank Switching Behavior Study (Savanta Research, n=500); NCUA Q4 2025 State-Level Credit Union Data Report (March 2026); Cornerstone Advisors / The Financial Brand, “Next-Level Growth: Credit Union Opportunities in a Changing Market” (December 2025); McKinsey & Company analysis of 60+ U.S. credit unions (2025); CSI 2026 Banking Priorities Survey; creditunions.com Q1 2026 TrendWatch.