.svg)

.svg)

As consumer credit delinquencies climb and net interest margins compress, lenders face a dual challenge: driving revenue growth while protecting portfolio performance and profitability.

Against this backdrop, Pay by Paycheck has emerged as a timely, powerful solution to control risk while delivering real benefits to borrowers.

Read on to discover why Pay by Paycheck has become a solution lenders can’t afford to ignore.

The growing pressure on lenders

Banks are grappling with two major headwinds:

1) Rising defaults:

- Consumer loan delinquencies hit 2.77% in Q1 2025, up from 2.6% just a year earlier 1

- 90 day serious delinquencies have increased by 52% from Q1 2024 2

- Subprime borrower delinquencies have risen by >7.4 percentage points from post-pandemic lows 3

2) Shrinking returns:

- Net interest margins across U.S. banks are projected to contract to ~3.0% in 2025, down from ~3.5% last year. 4

Together, these trends squeeze both portfolio health and profitability. Traditional risk mitigation strategies - like tougher underwriting or raising rates - come at the cost of operational efficiency, financial inclusion, and customer satisfaction.

A solution that benefits both lenders and borrowers

Amid mounting economic pressures, lenders have no choice but to adapt - and Pay by Paycheck is quickly becoming a go‑to strategy for driving growth while creating real value for borrowers.

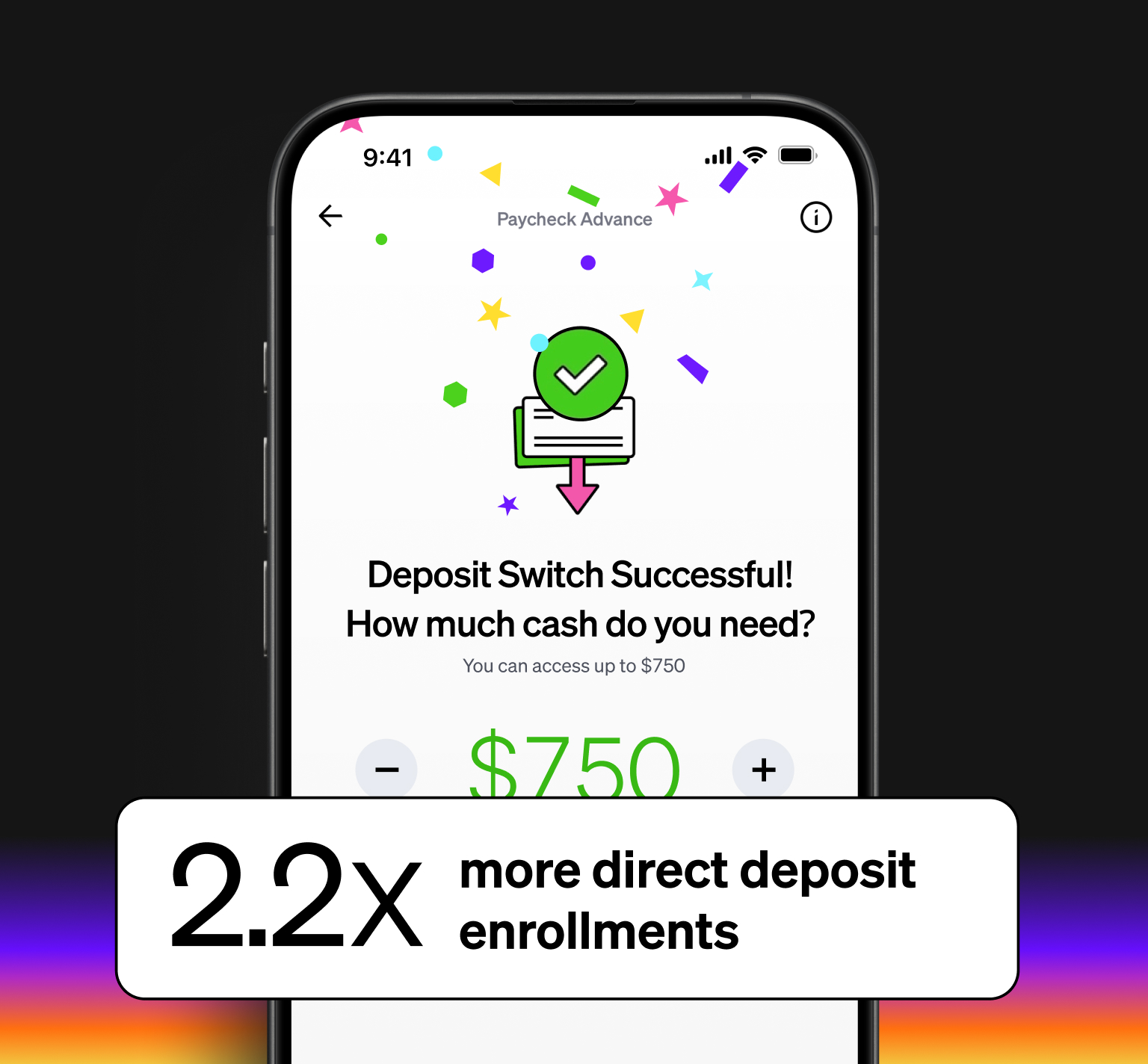

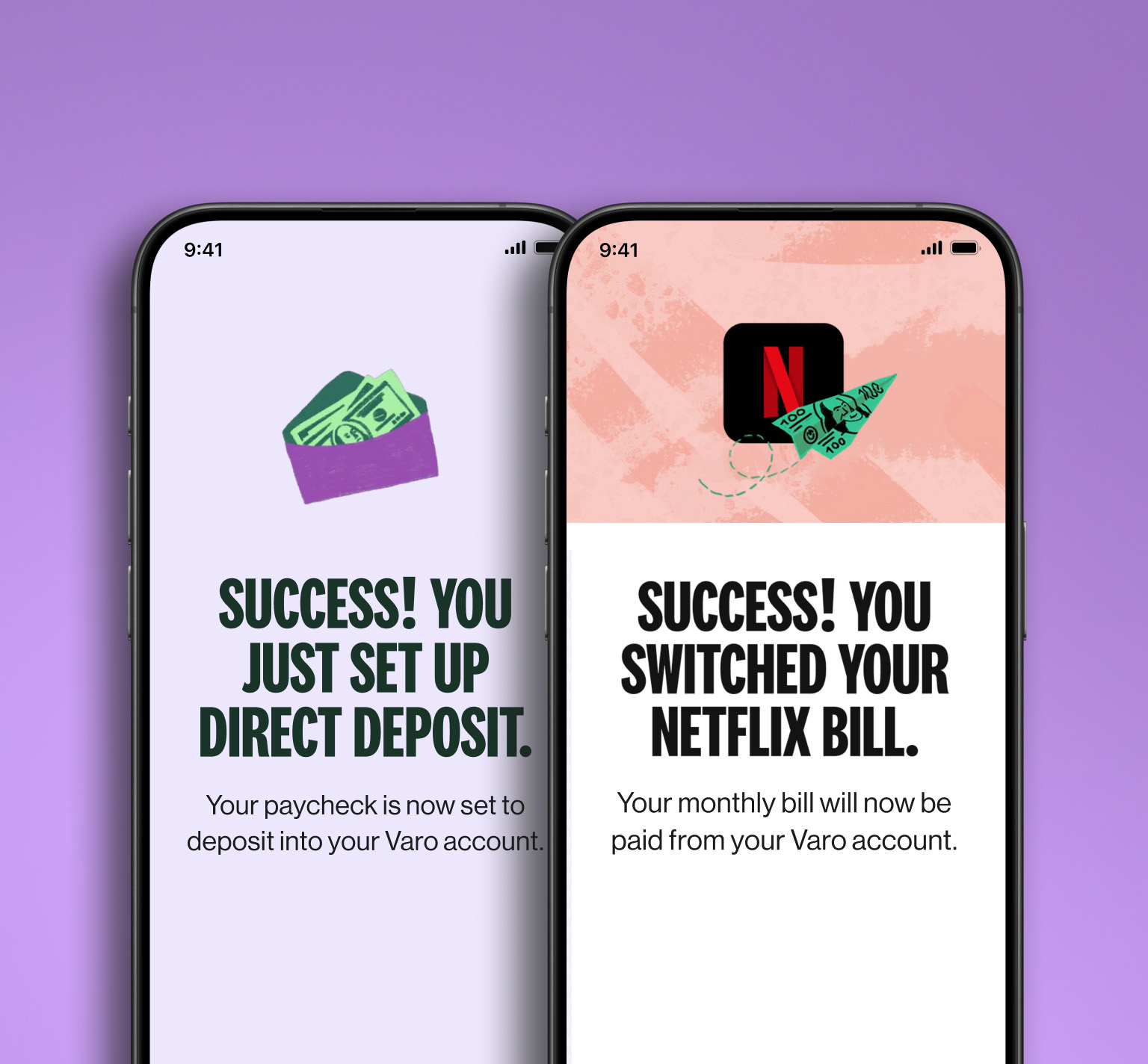

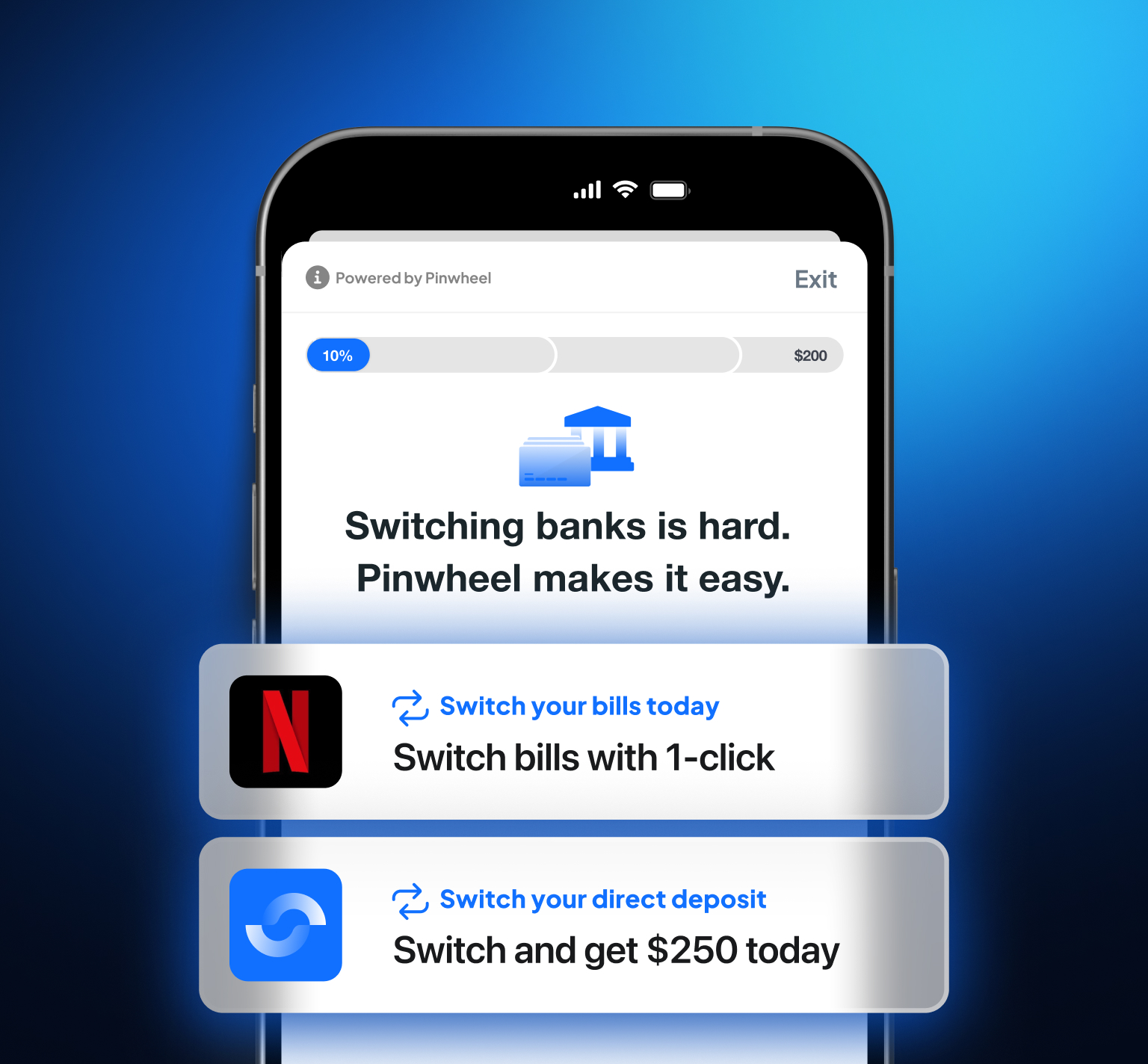

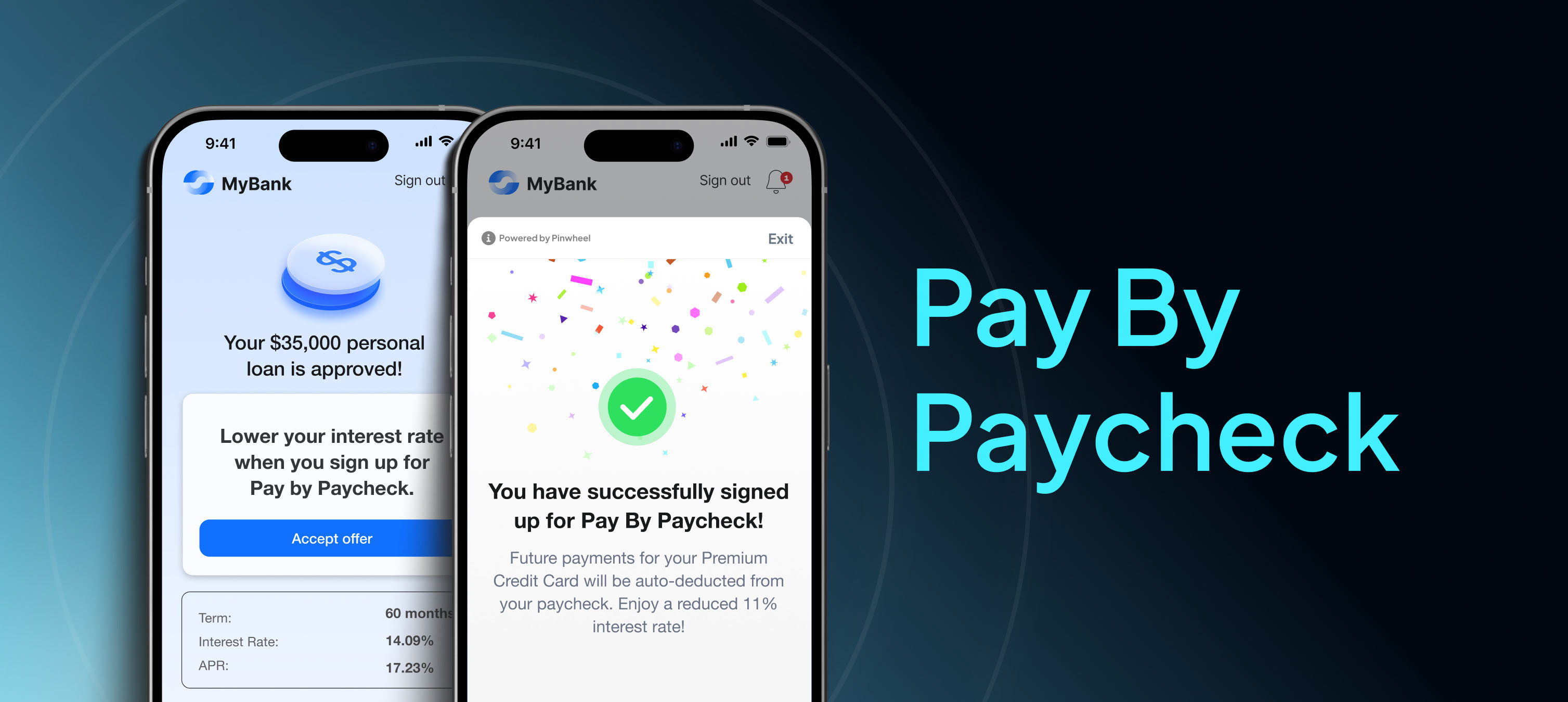

Pay by Paycheck solves for the rise in lender risk by tying repayment directly to the borrower's payday - before funds are available for discretionary spending. This improves repayment reliability and reduces late payments, delinquencies, and charge-offs.

Lending regulations have also ensured that Pay by Paycheck can only be deployed in borrowers’ best interests. Under small-dollar lending regulations, lenders are prohibited from requiring a specific repayment method as a condition of approval. This way, lenders are encouraged to offer post-approval borrower incentives - like a lower rate - for opting in to Pay by Paycheck.

This opens the door to true win-win dynamic. Lenders reduce risk by securing repayment directly from a borrower’s wages, while borrowers secure lower rates for participating.

And the borrower advantages don’t stop at lower rates. Because payments are made before wages even reach their checking account, Pay by Paycheck also helps borrowers:

- Improve financial planning: Automatic deduction of critical payments gives them a clearer view of their discretionary income and makes ad hoc budgeting simpler.

- Reduces stress: With payments handled automatically, there’s no need to track due dates or worry about missed payments.

- Minimize unwanted fees: Greater payment consistency ensures borrowers will avoid late charges or additional interest.

- Build credit: In programs that report on‑time payments to credit bureaus, borrowers can establish or improve their credit history.

So what’s the catch?

While Pay by Paycheck is a new lending approach that can benefit both lenders and borrowers, lenders must ensure implementation doesn’t contribute to their second major headwind: shrinking margins. A successful roll out will avoid driving up cost‑to‑serve and will not erode any margin gains achieved by minimized defaults.

Up next

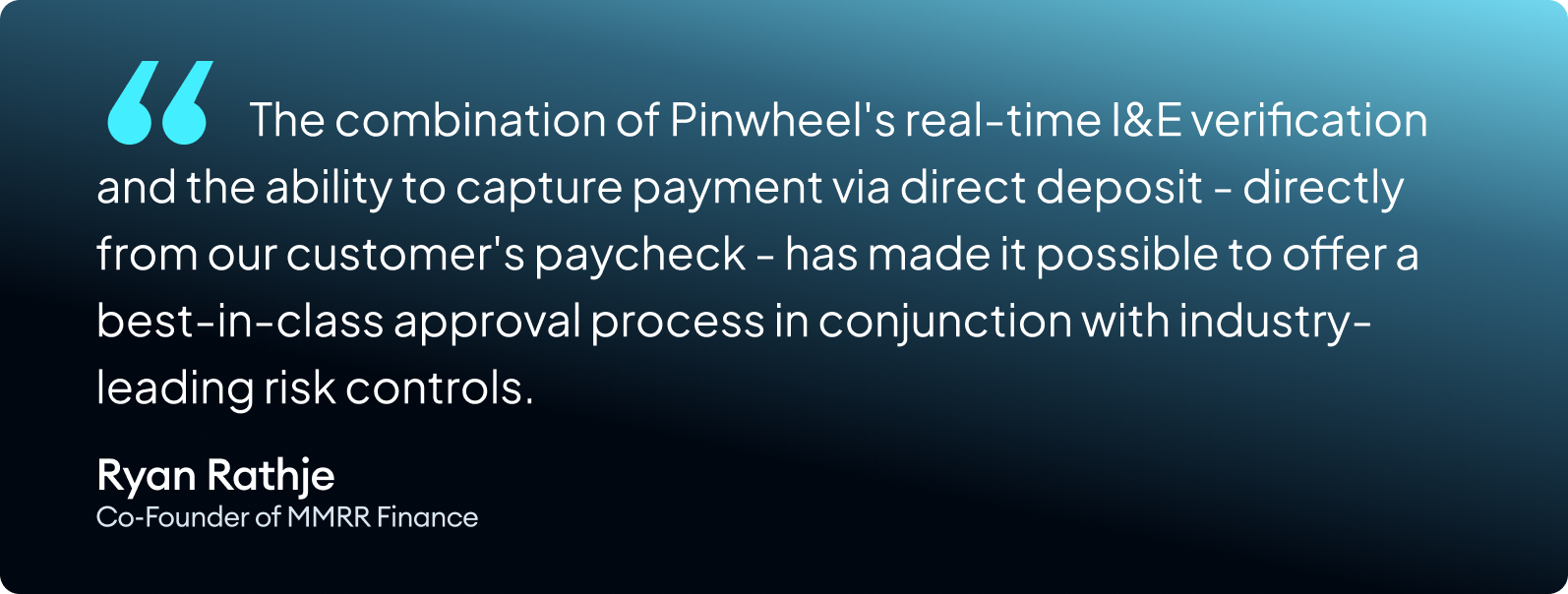

Stay tuned for our next post, where we’ll dig into why launching a Pay by Paycheck program hasn’t historically been easy - and share how Pinwheel has enabled lenders like MMRR to roll out a cost‑effective, seamless and borrower‑friendly solution.

If you’d like to learn more - set up a meeting.

[ 1 ] Trading Economics, [ 2 ] pymnts , [ 3 ] Federal Reserve Bank of Kansas City , [ 4 ] MOODY’s