.svg)

.svg)

The standard consumer credit report as we know it today has existed for three decades, emerging from a model where lenders approved borrowers based on their reputation and previous payment history.

Credit reporting agencies still include payment history in their reports today, alongside amounts owed, credit history length, new credit, and credit mix. But in recent years, financial service providers have also been seeking out alternative credit data to supplement the information in credit reports and create a holistic picture of a consumer’s financial situation.

Alternative credit data refers to any information not included in the traditional credit report that lenders use for credit decisioning. It may include data points on income and employment, utility payments, rental payments, payday loans, other alternative lending platforms, and bank account transactions.

Access to alternative data is possible with financial technology APIs that link financial service providers to consumer data inside various platforms. This technology enables lenders to easily partner with vendors that provide access to the alternative data they need to improve their services. Improvements include reducing default risk and lowering origination costs, greater financial inclusion, as well as offering more credit products to more consumers.

With mounting fears that a recession will strike in the next 12 months, alternative credit data vendors can support lenders in decreasing loss rates while helping more people access credit during a time of financial difficulty.

However, not all vendors offer the same level of data quality or regulatory compliance, making it necessary for lenders to carefully consider who they’ll partner with to enrich their understanding of consumer needs.

This article includes insights from Beyond the credit score: Propelling consumer finance into the future with income data, Pinwheel’s research on consumer attitudes and challenges with credit scores, creditworthiness, and alternative credit data.

What are the benefits of alternative credit data?

By leveraging alternative data sources that don’t factor into the consumer’s credit score, lenders unlock important benefits, such as growing their total addressable market.

Expanding credit products to new consumer segments

With alternative credit data, lenders can fill in the gaps left by traditional credit scoring models and offer credit to consumers they would otherwise have to turn away. Its importance in expanding credit access has even been recognized by major credit bureaus that have acquired alternative credit data providers.

According to Pinwheel’s research, poor credit scores are the main cause of the majority of denied loan applications. Credit invisible (28 million) and unscorable or thin-file (21 million) consumers also struggle to get approval for credit due to the lack of traditional data on their financial history.

However, there are still borrowers who don’t fit the “ideal credit profile” that still make good candidates for various credit products and services. Unfortunately, financial institutions often deny them access to credit because they do not have additional information that will allow them to holistically assess their credit risk.

Alternative credit data is the missing piece of the puzzle that allows lenders to get a holistic overview of the applicant’s finances that go beyond their credit file. With insights into factors like rent payment data, salary, and employment history, they can reach new consumer segments that have traditionally been excluded from the financial system and have to rely on high-interest credit cards, predatory loans, or borrowing from friends and family.

Enabling more innovative credit products and services

Fintech solutions have put innovation at the forefront of financial services. Consumers today can use everything from AI-powered wealth management platforms to crypto platforms. The high degree of innovation, however, has also put pressure on financial service providers to continually offer better and more personalized products and services.

Real-time, alternative credit data is critical for supporting innovation as it allows lenders to adjust their services to the dynamic nature of an individual’s financial needs.

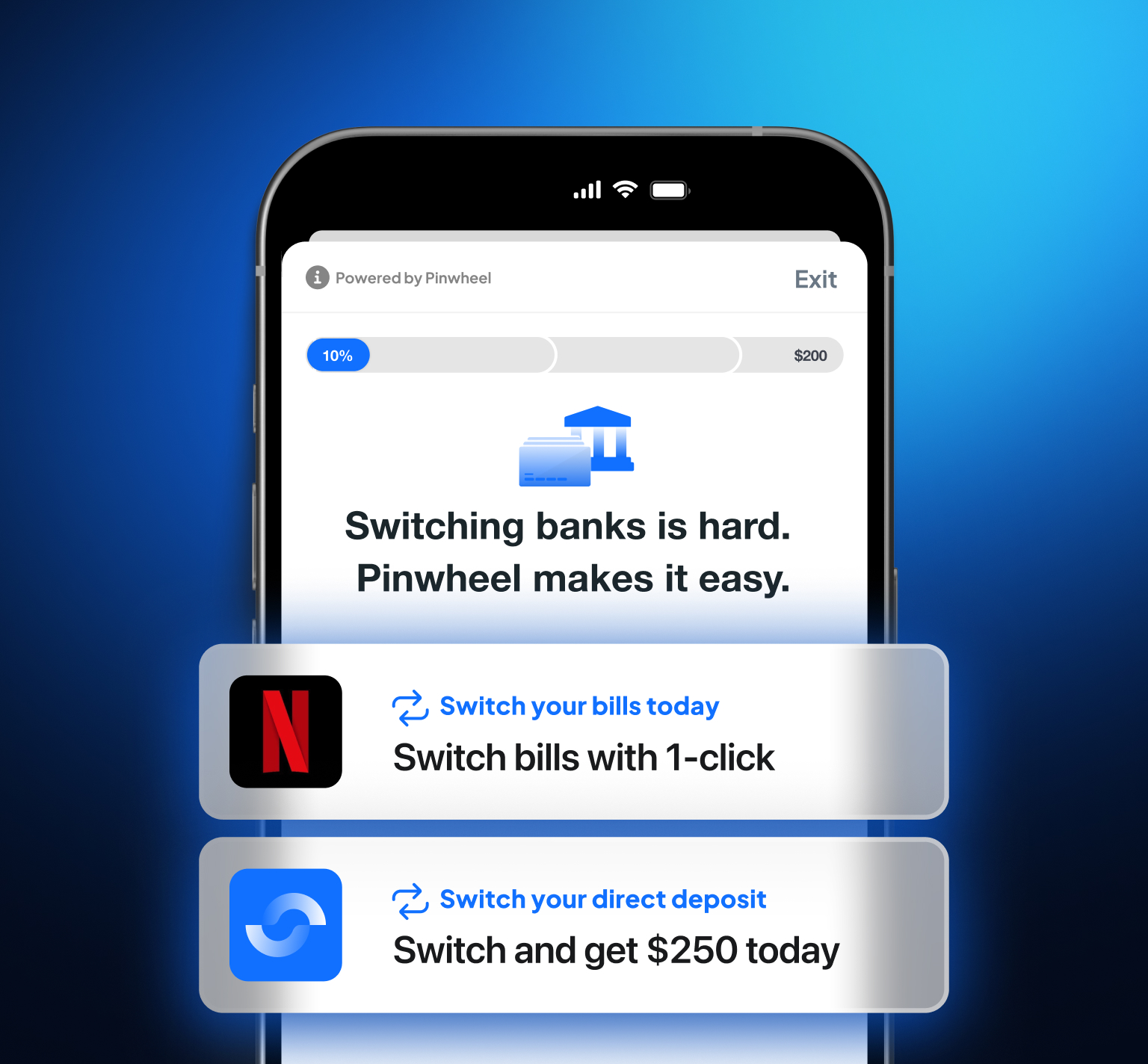

One example is payroll data. It’s the source of truth for a consumer’s income and employment information but has traditionally been inaccessible to lenders. Today, with payroll data connectivity APIs, lenders can easily connect to their customer’s data with their permission and even get real-time updates.

Pinwheel (a payroll data connectivity API) allows financial service providers to stay up to date with any changes to their customer’s payroll data with recurring access. The API sends an alert if a new paystub is available or if there has been an update to a person’s salary or employment status.

The ongoing access and monitoring create an opportunity to offer the right product (such as a credit line increase) at the right time, deepening customer relationships, increasing lifetime value, and preventing attrition.

Use cases of alternative credit data

Additional insights into a consumer’s finances set the stage for better, fairer, and more innovative financial products.

Seamless identity, income, and employment verification

Alternative credit data can power platforms that support easy verification processes. For example, by connecting to a customer’s payroll data, a lender can verify identity, income, and employment in one swoop.

As this is an automated process, lenders will create a better user experience and reduce fraud by no longer requiring the customer to manually retrieve and upload documents on their own. They will also improve business processes by freeing up employee time to focus on more complex tasks, boosting productivity, and minimizing errors that can occur with manual verification.

Roughly six in 10 working Americans are likely to use a platform for identity verification when applying for a personal loan. For 61% of Americans, providing this service would have a positive impact on their perception of their bank or fintech.

Cash flow underwriting

When lenders use alternative data such as income or bank transactions, they can make lending decisions based on cash flow rather than a person’s credit score. Cash flow underwriting allows lenders to reach the roughly one-third of Americans who are categorized as subprime borrowers and lack access to affordable credit.

A substantial number of consumers (more than 80%) are willing to grant access to their payroll or income data:

- 27% are fully open to sharing it with financial service providers

- 34% would be more open to sharing their data if it more accurately reflected their financial picture and made them eligible for better financial products.

Proactive remediation plans and portfolio analysis

The use of alternative data, such as income and employment, allows lenders to proactively respond to any changes and offer solutions before a loan goes delinquent. In times of financial uncertainty, this is a powerful tool that supports both consumers and lenders.

Sixty-three percent of working Americans are interested in proactive loan repayment plan recommendations if their income were to suddenly decrease.

Additional consumer data is also beneficial in case of an income increase. Around six in 10 consumers have an interest in automatic credit line increases based on their income growth powered by their real-time payroll data.

With real-time income and employment data, lenders are also able to improve their portfolio analysis and more precisely locate risk on their balance sheet.

Alternative credit data and FCRA compliance

Although there is no shortage of alternative credit data vendors, lenders should pay close attention to the level of regulatory compliance of the vendor they partner with. Fair Credit Reporting Act (FCRA) compliance, for example, is essential for any lender and alternative credit data vendor that provides consumer-permissioned data for credit decisioning.

Unfortunately, many vendors delegate this responsibility to lenders, exposing them to the risks that come with not complying with FCRA regulations.

To avoid FCRA violations, lenders should only work with vendors that are Consumer Reporting Agencies (CRAs), as they have the necessary processes in place to protect both consumers and lenders from bad data. When you work with a CRA, consumers can request a copy of their data and, if necessary, file a dispute. In case of any errors, the lender will be protected as the CRA bears full responsibility.

Among payroll data connectivity APIs, Pinwheel is the first API platform that is also a Consumer Reporting Agency (CRA). As a CRA, we stand by the quality of our data and allow our clients to safely use it for credit decisioning.

Access verified income data with Pinwheel Verify and Earnings Stream

To gain access to consumer-permissioned, alternative credit data, industry-leading lenders rely on Pinwheel Verify and Earnings Stream. The two solutions are powered by our connectivity to over 1,600 payroll and income platforms and the top 40 time & attendance platforms, spanning 80% of U.S. employees.

Verify offers real-time income data insights that lenders use to reduce fraud, manage lending risk, improve underwriting models, grow repayment rates, and more. Thanks to Pinwheel’s CRA status, all consumer data can be safely used for credit decisioning without violating the FCRA.

Earnings Stream takes income data from payroll platforms, analyzes it using machine learning, and returns valuable, backtested insights into how a consumer is going to perform over time. Lenders no longer have to make decisions without access to verified consumer employment data. Now, they can access a customer’s actual historical cash flows, accrued earnings in the current pay period, and projected earnings and pay dates. Earnings Stream supports multiple use cases, including earned wage access, cash flow underwriting, and other innovative services that are the future of consumer finance.

In the future, a solution like this could even determine risk of job loss, or likelihood of a significant increase or decrease in earnings. With such powerful digital lending technologies, lenders would be able to predict their customer’s needs and deliver a truly personalized experience.

Contact us to learn more about how you can leverage Pinwheel to take your lending products and services to the next level.