.svg)

.svg)

By 2025, banks plan to double their use of both internal and external APIs to enable partnerships, facilitate regulatory compliance, boost innovation, and more.

Innovation is precisely where financial technology APIs shine, allowing companies to quickly implement new features and improve the user experience without all the costs that come with developing a feature from scratch.

Fintech APIs span services from payment processing and earned wage access to cryptocurrency, and they facilitate the rapid growth of digital financial services. Simultaneously, they’re transforming old models that have excluded millions of people from accessing affordable financial products.

What are fintech APIs?

An API (application programming interface) is a program that allows two separate applications to exchange data. A fintech API is simply an API used in financial apps. For example, if you’ve ever connected your bank account to an app for personal finance management, you’ve done so with the help of an API.

While APIs can be internal and inaccessible to third parties, many financial service providers also rely on APIs developed by third-party providers that are accessible externally.

Use cases powered by fintech APIs

Leaders in the financial industry rely on APIs for a range of services, from earned wage access to financial data aggregation and payment processing.

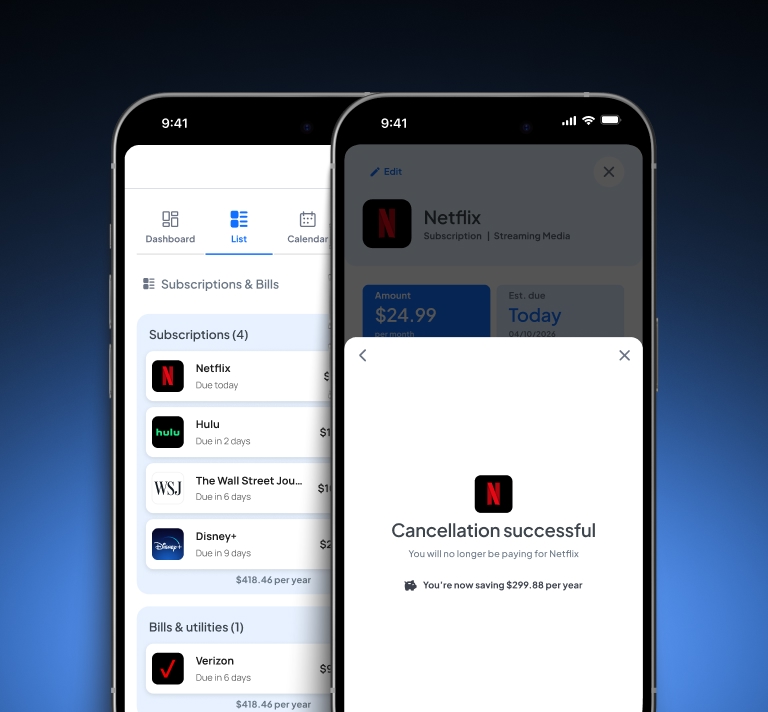

Earned wage access

Earned wage access (EWA) or on-demand pay is currently one of the most talked-about products in the financial industry. It allows employees to withdraw their earnings at any time, which gives them more financial control, especially when faced with emergencies. Considering that 80% of consumers have expressed interest in on-demand pay, EWA presents a big opportunity for financial providers.

APIs that connect to payroll systems and other income platforms with the customer’s permission make it possible for financial service providers to easily offer EWA to their customers. For example, Pinwheel Earnings Stream provides a historical, present, and future overview of a customer’s earnings using real-time payroll data, which EWA providers can use to confirm how many hours an employee has worked.

Cash flow underwriting

In the traditional financial system, lenders rely heavily on credit scores to determine a borrower’s ability to repay a loan. With access to cash flow data, they can offer loans to consumers whose credit scores would otherwise prevent them from getting approved for a loan.

One way that lenders can access cash flow data is by using APIs that retrieve user-permissioned bank account transaction data. Then they’ll need to analyze the data to determine the consumer’s creditworthiness. However, this type of banking API has access to limited data since most Americans have bank accounts in more than one financial institution. (One survey found that the average consumer owns 5.3 financial accounts.)

A payroll data connectivity API like Pinwheel provides more insight into the customer’s financial picture with verified income and employment data while also preventing fraud with verified identity data and helping lenders reduce risk.

Payment processing

Payment APIs such as Stripe enable apps and websites to easily accept payments without having to build a payment solution from scratch. APIs also allow merchants to integrate a variety of payment methods like PayPal, Google Pay, and Apple Pay to improve the customer experience.

Additionally, leading payment processors implement strong cybersecurity measures to protect both businesses and consumers from data breaches, which is an added benefit of implementing an API rather than developing a payment solution in-house.

Financial data aggregation

Financial data aggregators gather consumer information via APIs from different sources, such as bank accounts, lending platforms, and investment platforms, and then make it available to the consumer or third parties.

For example, some data aggregators provide solutions that allow consumers to see all of their financial information in one place for easy money management. Others, like Plaid, work directly with financial service providers to allow consumers to easily link their financial accounts.

In addition, data aggregation enables financial service providers to leverage additional user-permissioned data when evaluating loan applications to get a more complete picture of their financial situation.

Cryptocurrency

In the cryptocurrency space, APIs have enabled apps and websites to easily integrate a fiat onramp, allowing users to purchase crypto without going to a separate crypto exchange. For example, Onramper is one API solution that offers users the option to buy more than 200 different cryptocurrencies in-app.

Know Your Customer

In 2021, financial service providers lost over $3 billion due to fraudulent transactions. Know Your Customer (KYC) solutions are crucial to combat fraud, which is another opportunity for APIs to help the financial industry.

Pinwheel Verify is an API solution that uses identity data (full name, date of birth, social security number) from payroll platforms to enable financial providers to improve their fraud prevention processes. The solution also prevents users from misrepresenting their income or employment status on loan or rental applications.

What are the benefits of fintech APIs?

From open finance to lower development costs, the benefits of APIs in the financial industry extend to both consumers and financial service providers.

Enabling open banking and finance

Fintech APIs allow consumers to connect and share their financial data with different service providers to get access to better products. They are instrumental in facilitating open banking and open finance, bringing together customer data from different sources to create a holistic picture of a consumer’s financial circumstances.

While open banking APIs enable users to share their bank account information, open finance goes a step further to allow data sharing from multiple sources, such as payroll providers and gig and creator economy platforms.

Connectivity to payroll and income platforms is especially key as they are the foundation of consumer financial data. A bank statement can tell you how much money a customer has deposited into their account over a period of time, but payroll offers data on much more, including their salary and employment. Access to more robust data gives financial institutions and fintech apps the freedom to offer personalized services, from insurance to mortgages.

In addition to enabling open finance, APIs also allow fintech companies and legacy institutions to layer additional banking services into their product without investing the time and resources to build the API on their own. As a result, they can quickly introduce new services to their consumers and maintain a competitive edge.

All of this innovation rests on consumers’ willingness to share their data. Financial service providers are in luck, however, as 86% of consumers say they are open to sharing their data to have a personalized banking experience.

Expanding access to better loans

APIs allow lenders to better determine an applicant’s credit risk by connecting to payroll systems and other income platforms to verify income and employment. Even if the applicant has an insufficient credit score, the lender can still approve their application based on other data, such as their salary and employment duration.

Pinwheel’s income and employment verification solution provides data regarding the applicant’s identity, income, employment, pay stubs, and shifts. Our API platform connects to more than 1,800 payroll systems and gig economy platforms, covering 100% of paid Americans. The wealth of data makes it possible for lenders to easily perform income and identity verification, approve loans for underserved consumers, and even launch products, such as paycheck linked lending.

Since Pinwheel is a Consumer Reporting Agency (CRA), companies in the financial sector can safely use consumer data for credit decisioning while ensuring FCRA compliance.

As for consumer benefits, they can borrow money with lower interest rates, increasing their chances of repaying the loan and improving their credit score. Previously, credit-damaged and credit-invisible consumers often had no other choice but to turn to high-interest loans, which they later struggled to repay. This created a vicious cycle that made it almost impossible for consumers to improve their financial health. Twenty-one percent of Americans do not get approved for a loan, credit card, or apartment rental due to a poor credit score — but fintech APIs can change that for the better.

Enabling self-driving finance

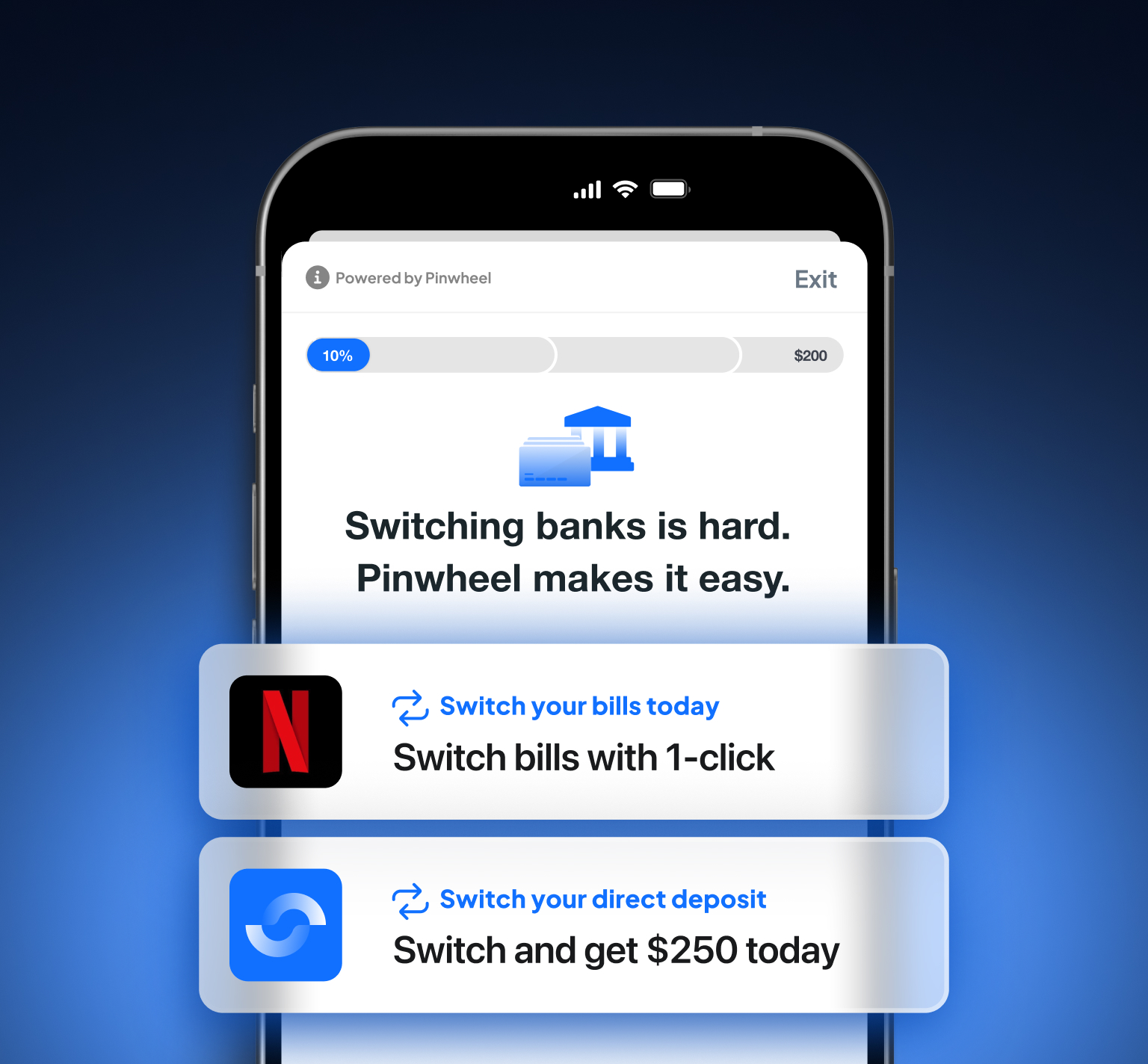

Just like driverless cars have automated driving, self-driving finance automates manual processes, such as investing or transferring money from checking to savings. Self-driving finance solutions can also include automatic overdraft protection to save customers from non-sufficient funds (NSF) fees. And APIs further facilitate driverless finance by automating processes, such as direct deposit switching.

While the fintech industry has made it possible to open a new bank account in minutes, many still rely on a manual deposit switching process to enable customers to fund their accounts. This outdated solution is time-consuming and inconvenient for the customer. Pinwheel’s API, however, enables financial service providers to offer a smooth direct deposit switching process.

The API solution gives users full control over their direct deposit settings in-app. Once customers connect to their payroll provider, all they need to do is specify the amount of money they want to automatically deposit into their account every payday, and the API takes care of the rest. For instance, 20% of their salary could go straight into their robo-advisor account, 10% into their crypto wallet, and 5% into a savings account for their next vacation. As a result, customers can rely on automation to do all the work from the moment they get their paycheck.

Cutting down on development costs

API integration is a single solution to several challenges companies are currently facing, including a developer shortage and the economic downturn.

In 2021, the global shortage of full-time software developers amounted to 1.4 million, which is expected to grow to 4 million by 2025. Consequently, many companies simply don’t have the software development workforce to build features from the ground up. And with less VC funding available due to the tumultuous market conditions, startups need to carefully evaluate where they will invest their time and resources.

Fintech APIs allow companies to quickly expand with additional features, driving innovation and reducing time-to-market without incurring the high costs of in-house development.

APIs make product expansion easier than ever before

Fintech APIs have made it possible for consumer fintechs, lenders, and traditional banking institutions to launch new products and streamline the integration of new features, all while saving considerable time and resources.

Financial APIs do all the heavy lifting, allowing fintech startups and legacy institutions alike to focus their attention on what really matters — the consumer. And thanks to the abundance of data that APIs can access, the old financial model, which has excluded so many vulnerable groups, will become a thing of the past.