.svg)

.svg)

Biweekly and monthly pay cycles, and the debt they push people into, should be a relic of the past. For the 63% of Americans living paycheck-to-paycheck, large expenses, even routine ones like rent, can create financial strain. Many Americans turn to payday loans and credit cards to relieve this pressure, but these loans and overdraft fees charge exorbitant interest rates and have poor user experiences, leaving the average borrower in debt for 5 months per year. While the liquidity they provide is great, the downstream effects are brutal. What if there was something better?

Advent of Earned Wage Access

Earned wage access (EWA) first appeared several years ago to solve this problem. Instead of workers waiting until the 15th of the month to get their paychecks, workers can access their wages as soon as they’ve completed the work. The facilitator of these earned wages can be the payroll provider, an employer-benefits provider, or a third-party direct-to-consumer service. The cash advances are non-recourse, meaning they can’t be sent to a collections agency, and, based on Consumer Financial Protection Bureau (CFPB) guidance in 2020, not a form of credit under Regulation Z.

How do these different EWA providers compare? And why do payday loans still exist?

Existing Limitations of Earned Wage Access

At first glance, EWA from the payroll provider, like ADP, seems to make the most sense. Payroll providers have all the right data and they have an existing relationship with the worker. However, they face two headwinds: monetization and innovation, which are closely tied together. Payroll providers are B2B companies, they monetize from business experience, not consumer experience. Business dynamics force them to charge employers an extra fee to offer the service, and they aren’t strongly incentivized to provide a good experience to workers (since they aren’t paying). Because of this, it’s a hard product to work on, and most payroll provider EWA solutions have had a revolving door of leadership coming and going over the past several years.

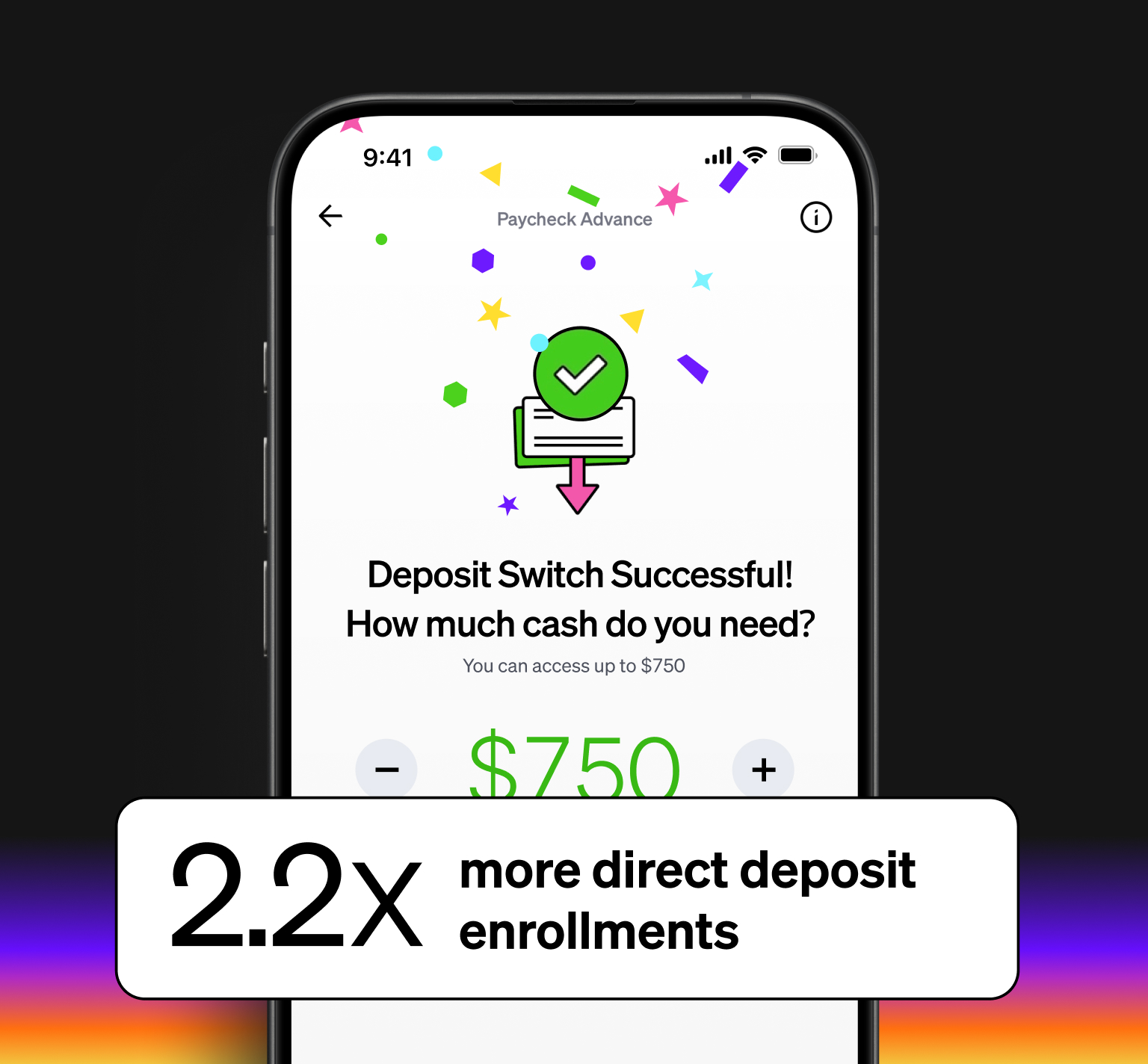

Services offering employers EWA as a deductible benefit are an evolution arising from the headwinds payroll providers experience. These services have created a great experience, and following the CFPB guidance, they usually charge employers for the service, allowing employees to access it unencumbered. They recover cash advances via a paycheck deduction, which is early in the income stack, keeping their risk of loss very low. These services offer cash advances that are meaningful in size, often with a cap at 50% of net earnings, which can be many hundreds of dollars. So what’s the catch? Well, these services are pretty good. It’s just that most workers will never see them because they require employer-by-employer partnerships and less than 16% of employers offer a benefit like EWA.

Direct-to-consumer EWA and cash advances solve this availability problem, but so far the approaches come with several compromises. Fundamentally, most of these services determine earned wage by reviewing historical direct deposit transactions, with novel approaches for new users*, and setting conservative caps to mitigate the week-to-week 32% fluctuations in pay that the average hourly workers experiences. That’s the difference between making $380 one week and $560 the next—a $180 difference. When a user’s paycheck hits, these services need to recover funds. Many do so via ACH or OCT debit operations, which runs the risk of non-sufficient fund alerts—imposing additional expenditures to the worker—and requires complicated payday timing metrics**.

All-in-all, most direct-to-consumer services limit advances to <$250 per paycheck. The average payday loan is $375. These direct-to-consumer services don’t meet the financial needs of their users.

What if you could combine the certainty of employer-sponsored EWA with the availability of direct-to-consumer offerings?

The Future of Earned Wage Access

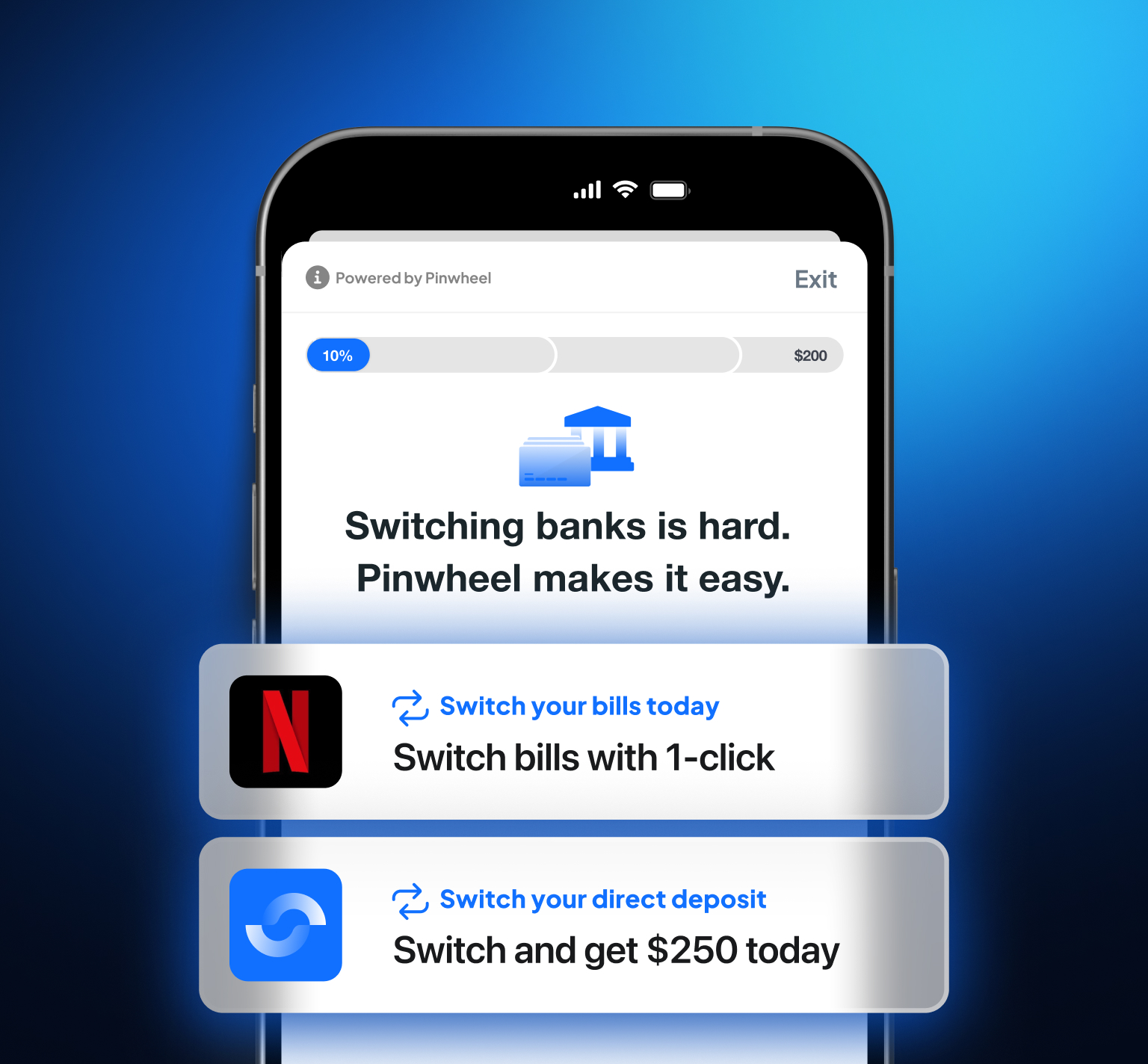

EWA that is low risk-of-loss, provides large cash advances, and is widely available is the future of EWA. Pinwheel provides the foundation: retrieve accurate cash flow sizes with Pinwheel Earnings Stream and enable reliable repayment with Pinwheel Direct Deposit Switch.

To do cash flow sizing for hourly workers you need to know their numbers of hours worked since the last pay period close and their hourly rate net taxes and other deductions. For salaried workers you need to know their net salary and employment status. Are they actively receiving a paycheck? Are they on leave? Have they been let go?

Pinwheel retrieves this information from ~1,600 payroll providers, and the top 20+ time & attendance platforms, then calculates and packages net earnings into a single endpoint—Pinwheel Earnings Stream—allowing providers to bring an EWA product to market in days, not months or years. In doing so, we’re providing a fundamentally different service by actually making sense of a consumer’s income & employment data versus putting the burden on our customers to analyze and transform it.

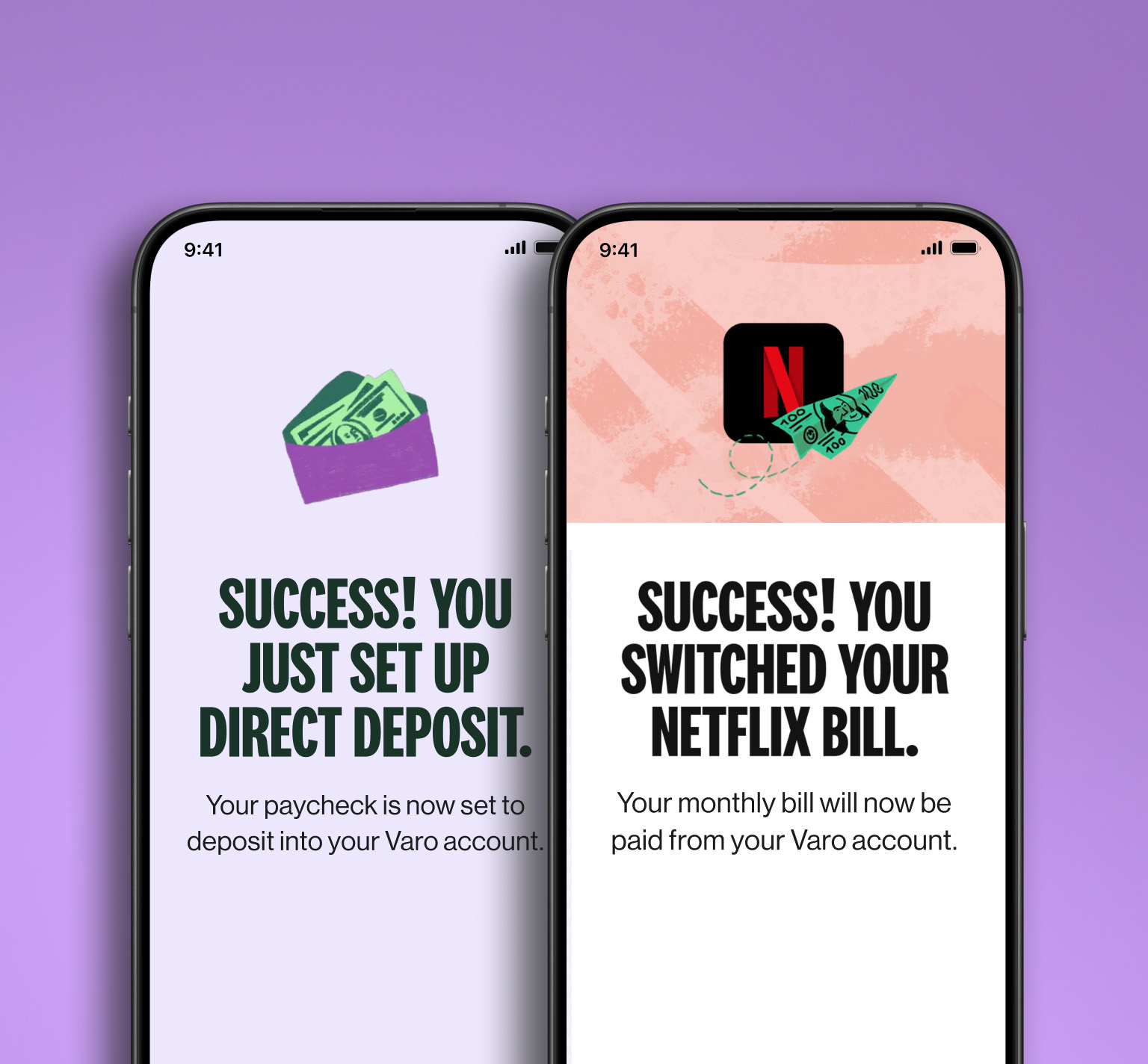

When it comes to repayment, the most reliable form is based on credit operations, since debit operations can fail. The vast majority of workers have access to direct deposit—ACH credit operations originating directly from the payroll provider—providing a reliable way to recover funds without a risk of non-sufficient funds or overdrafts. Pinwheel’s Direct Deposit Switch enables direct deposit control for over 80% of workers. If an EWA provider was also a financial services provider, managing a bank account for the worker, they can make a compelling offer for the worker to switch and maintain their direct deposit with that account.

It’s not often that a win-win-win solution pops up—workers are excited, they get meaningful liquidity; financial institutions are excited, they get compelling direct deposit retention; employers are happy, their workers have lower financial stress—but the future of EWA achieves this trifecta.

If you want to unlock the future of Earned Wage Access with the suite of Pinwheel products, get in touch with us.