.svg)

.svg)

Whether you’re a big financial institution or a neobank startup, digital innovation in the financial industry impacts everyone. Fintechs have joined traditional banks in offering services from checking accounts to loans — and Big Tech is also launching financial products of its own. (Hello, Apple Pay Later.)

Digital transformation in banking has made it easier for companies in the financial industry to innovate, resulting in solutions such as virtual banking assistants and robo-investing platforms. But industry experts point out that some financial service providers, especially traditional banks, have only just begun their digitization journeys.

Of the banks that say they are halfway done with their digital transformation, just 14% have implemented machine learning tools, around 25% have launched chatbots, and only 6 in 10 use APIs or cloud computing. If banks want to stay on track while faced with fintech competition, they’ll need to double down on implementing new tech.

In 2022, financial service providers are using established technologies such as AI and APIs to evolve their products. Others are experimenting with super apps to build deeper relationships with their customers. Here’s everything you need to know to keep up.

What is digital transformation in banking?

According to Cornerstone Advisors, 80% of banking executives agree that digital transformation is the “integration of digital technologies into all areas, fundamentally changing how to operate and deliver value."

In practice, digital transformation in banking can mean using technology to improve existing digital banking products, as well as to develop new ones. It can also improve internal processes to help financial service providers be more efficient — like using automation to save employees time.

When we talk about digital transformation in banking, the traditional banking sector is only one part of the story. Consumer-facing fintechs can also reap the rewards of innovation as they work on growing their customer base, improving the customer journey, and increasing retention. And both banks and fintechs can rely on partnerships with third-party solution providers to accelerate their digital transformation and meet consumers’ expectations for sleek and innovative mobile banking services.

In their digital transformation strategy, banks and fintechs also have to consider cybersecurity. In 2021, the financial services industry received over 25% of all distributed denial of services (DDoS) attacks. Without proper security measures, every exciting new technology could become a nightmare vulnerable to attacks.

Innovations driving digital transformation in the banking industry

Here are some of the most exciting digital solutions and trends that are transforming banking.

APIs (Application programming interfaces)

Fintech APIs have paved the way to open finance, allowing consumers to share their financial data with third parties. From 2019 to 2021, the percentage of credit unions and banks using APIs jumped from 35% to 47%. And in 2022, an additional 25% will join this group.

Banking institutions and fintechs are using APIs to develop new products faster, automate manual processes, and improve the overall customer experience. For example, APIs used in banking are powering financial management platforms (Cleo) as well as embedded finance products (Bond). There are even APIs that promote sustainability by integrating carbon footprint calculators based on users’ transaction data.

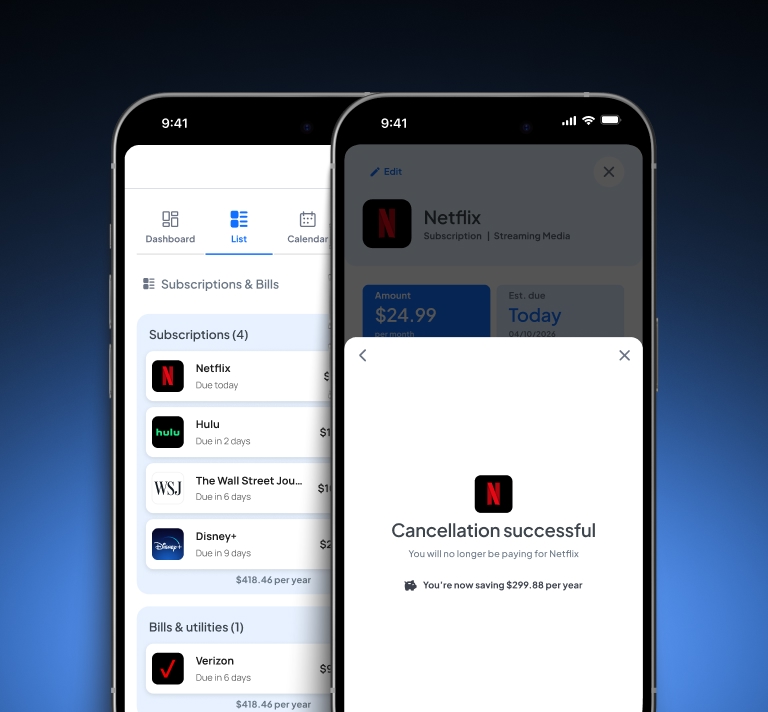

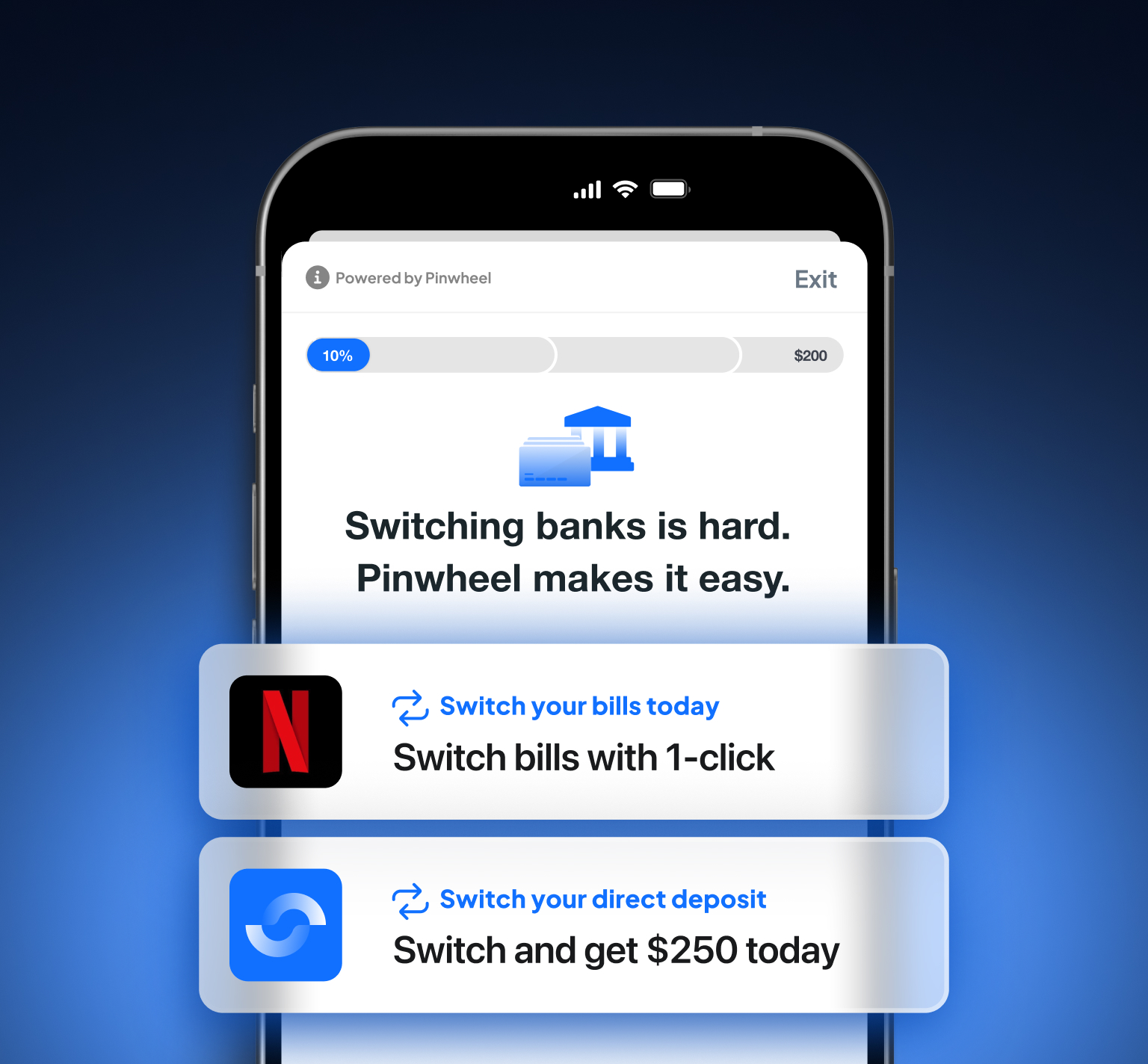

APIs that enable access to payroll data (with consumer permission) are the next frontier in consumer finance. Often referred to as payroll APIs, they can connect to over a thousand payroll and income platforms, unlocking access to consumer financial information such as income and employment data. With access to this information, banks and fintech companies can improve their underwriting models, automate direct deposit switching, and even launch services like earned wage access.

Now that consumers expect more personalization in banking, financial service providers that can connect to their users’ payroll and income data will have a unique advantage when developing new products and upgrading existing ones.

AI (Artificial intelligence)

Financial service providers mostly rely on AI technology to power chatbots and fraud monitoring. But in 2022, Accenture reports that AI will play an important role in facilitating more meaningful conversations between customers and financial institutions. For example, advanced AI technology could evaluate whether the customer is frustrated and provide tailored responses rather than generic replies that increase the customer’s dissatisfaction.

McKinsey’s 2021 Global Banking Annual Review also emphasizes the importance of AI in creating more granular segmentation models. AI can analyze consumer data and run A/B testing to help financial service providers identify the needs of smaller customer groups. It can also help predict customer behavior. In South Africa, Standard Bank used Microsoft’s Power BI (data visualization software) to build a predictive churn model. The Power BI machine learning feature identified customers at risk of churning and divided them into segments that the bank could target to improve retention.

Super apps

Super apps, which combine a number of services from social media to lending, have been popular in Asia for years. The West has been slow to move on this, but some tech companies are starting to merge different services under one mobile app’s umbrella. For instance, PayPal has released an app that combines payments, shopping, cryptocurrency, direct deposit, and other features to offer a comprehensive financial service to its users.

Although not all financial institutions are going to be interested in developing their own super apps, a recent EY banking report points out that taking part in a super app ecosystem is a valuable consideration. Consumers want digital financial services to effortlessly integrate into their everyday digital experience, and a super app can facilitate that.

Accelerate your digital transformation strategy with Pinwheel’s API

Pinwheel is the industry's leading API for payroll data that enables bank and fintech customers to connect their payroll or income platform. With Pinwheel, customers can easily switch their direct deposit or verify their income and employment, eliminating paperwork and manual processes while improving underwriting models.

We cover more than 80% of paid Americans, including gig and creator economy workers — the highest in the industry. Pinwheel also connects to more than 1.5 million employers, more than triple the number of employers offered by other payroll APIs. Thanks to our unmatched coverage, our clients can service the vast majority of their customers.

In addition to automating manual processes, Pinwheel’s clients are using our API to launch new products like earned wage access and paycheck linked lending. In this case, a single API saves our clients invaluable time and resources as they avoid manually connecting to every single income platform. Ultimately, it gives you more time to focus on taking your digital transformation initiatives to the next level in 2022 and beyond.