.svg)

.svg)

With more than 50 neobanks in the US, there’s intense competition to attract more users and grow revenues. In an effort to increase customer base, neobanks are not just facing off against each other but against traditional financial institutions as well, who are investing heavily into new banking technologies.

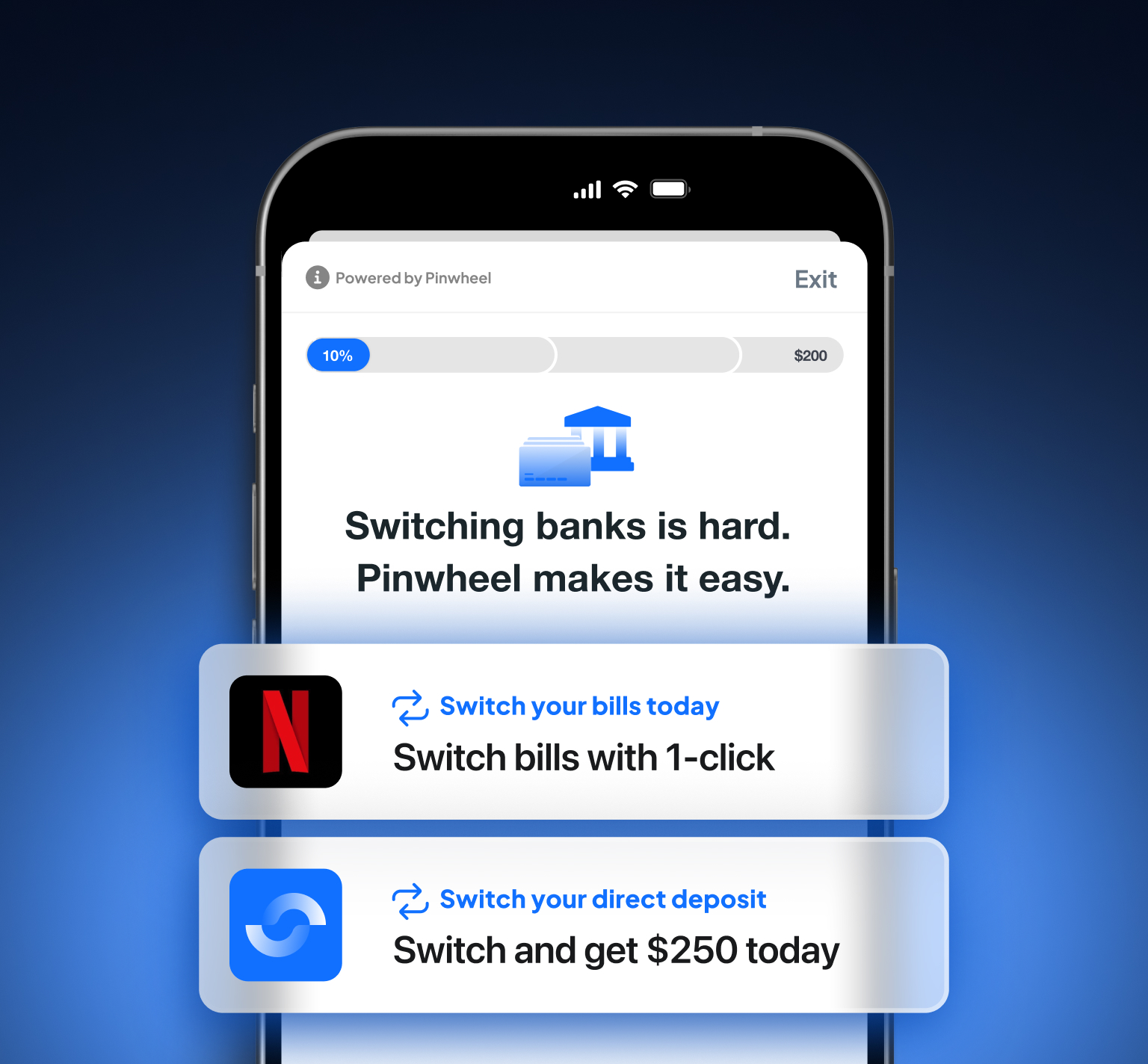

By leveraging direct deposit switching, banks and neobanks can get ahead in more ways than one. Streamlined direct deposit switching enables consumers to easily update their deposit settings, allowing banks and neobanks to increase their share of wallet. Consequently, they can also generate more revenue from interchange fees if a consumer holds a greater share of funds in these accounts. But even more essential for long term profitability is that it creates opportunities to gather valuable consumer data and power additional financial service products.

It’s important to point out that neobanks are just one segment of consumer-facing fintech that can benefit from a direct deposit switching API. The line between neobanks, who started out by offering fee-free bank accounts, and other consumer fintechs is blurring. For instance, robo-advisor Wealthfront now offers a checking account and debit card, digital wallet Venmo provides both a debit and a credit card, and crypto exchange BlockFi recently launched a credit card.

As a result, consumers have never had more choices when it comes to financial service products. But while a user can have countless fintech apps on their phone, they’ll still select only one bank account for their primary financial relationship. And direct deposits hold the key to solidifying that relationship.

With automated direct deposit switching, banks and consumer fintechs can start benefiting from several key advantages.

Direct deposit switching drives more revenue and improves the customer experience

Direct deposit switching streamlines what was once a tedious manual process for customers. Pinwheel’s direct deposit product, for example, allows users to update their direct deposit settings in just a few clicks, so customers are more likely to direct a portion (if not the entirety) of their paycheck to their new bank account. This is powerful — in fact, Pinwheel has seen uplifts in direct deposits as high as 75% with automated switching.

With funds in their account, a consumer will use it to make everyday purchases, helping the bank or neobank generate more profit from interchange fees. This can translate into meaningful revenue growth. Based on our insights, the average number of debit transactions per user is 28 a month, and the net revenue is about 24 cents per transaction. From 100,000 customers, a bank can earn roughly $672K per month from interchange alone.

Additionally, when banks and fintechs implement direct deposit switching, they improve the user experience. Research has shown that 44% of consumers in the U.S. say that setting up direct deposits electronically is an important element of mobile banking. It’s the second most in-demand feature, ahead of overdraft alerts.

Failing to meet this critical consumer need risks customer attrition and decreases the chances of customers adding additional services to their account. A recent EY consumer banking survey found that consumers who have been with a bank for 3-5 years are more likely to borrow funds and invest in additional services than those who’ve had their accounts less than a year.

When layering a payroll integration into a banking or fintech product, companies should also pay close attention to coverage. Limited platform coverage can create friction for the consumer if they can’t find their payroll provider or employer when looking to switch direct deposit settings. Pinwheel can eliminate this friction — our coverage spans 80% of working Americans (including gig economy workers) and more than 1,500 platforms, which is 3X the industry average.

Connecting to consumer payroll data enables new use cases

Competition in the digital banking space is high, spurring further product innovation. Neobanks, for example, are now expanding into new lending and credit-building products to differentiate themselves from traditional banks.

Pinwheel sets up a point of connectivity to a user’s payroll data, which banks and neobanks can leverage to offer additional products such as earned wage access (EWA) or personal loans. EWA is in high demand — 77% of American workers said they would use an EWA service if offered by their bank or credit union, and it's not unreasonable to conclude that they would show the same preference toward neobanks as well.

Another critical opportunity that payroll connectivity enables is lending. By analyzing customer payroll account data, banks and neobanks can underwrite loans for customers who are credit invisible or who would otherwise be turned down because of a poor credit score.

Pinwheel can make product expansion possible by providing access to the income and employment data needed for better loan underwriting.

Automated direct deposit switching is key to bank’s and neobanks’ success

As 2021 was a record year for fintech funding, companies are likely to keep pouring money into bigger and better digital finance products. Meanwhile, neobanks, consumer fintechs, and traditional banks are continuing to innovate in this environment to give customers more reasons to use their services.

While competition in financial services has never been fiercer, leading banks and fintechs have figured it out. Automated direct deposit switching is essential for growth. With direct deposit switching, companies competing for loyal consumers can capture a greater share of wallet, connect to their consumer’s payroll, and use that data to expand into new products and services. Any bank or fintech holding off on implementing a payroll integration might want to rethink their approach.