.svg)

.svg)

The recent determination by the Consumer Financial Protection Bureau (CFPB) that its own open banking rule under Section 1033 of the Dodd-Frank Act is unlawful and should be set aside sent waves through fintech and financial services circles. While many hoped this regulation would usher in a new era of consumer financial data interoperability, its sudden potential collapse offers a sobering reminder: relying on government regulation for innovation is a risky strategy.

At Pinwheel, this moment reaffirms the core thesis we've held since day one: real innovation in financial access must be built through direct, durable, and mutually beneficial partnerships with data holders, not by banking on the uncertain promise of regulatory expansion and enforcement.

What Just Happened?

The CFPB, now under new leadership, filed a status report in the ongoing federal court litigation that its own open banking rule “unlawfully seeks to regulate open banking” by requiring banks to share data with authorized third parties. The rule, intended to give consumers more control over their financial data, required banks, and one day potentially payroll companies and gig platforms, to build connectivity so that consumers could share their data with other apps and services across the internet.

This reversal by the CFPB stems from a lawsuit filed against the CFPB in the U.S. District Court for the Eastern District of Kentucky immediately after the rule was finalized in October 2024 claiming the CFPB exceeded its authority. The result: the government has stepped back from trying to codify a consumer’s right to share financial data via third-party services, potentially undermining years of momentum in open banking.

What This Means for Fintech and Consumers

For data aggregators or fintechs relying on the open banking rule to level the playing field, this is a major blow. Without regulation enforcing data access, many are left with questions about what data will be made available, by which institutions, and via which methodologies. The rule gave consumers more control over how their financial data is used and the ability to easily access and share their data with third parties.

At Pinwheel, we’ve never waited for the government to mandate progress. We’ve built our platform on the belief that access to income data across the internet and consumer choice is too important to leave to chance.

The Pinwheel Approach: Mutually Beneficial Partnerships

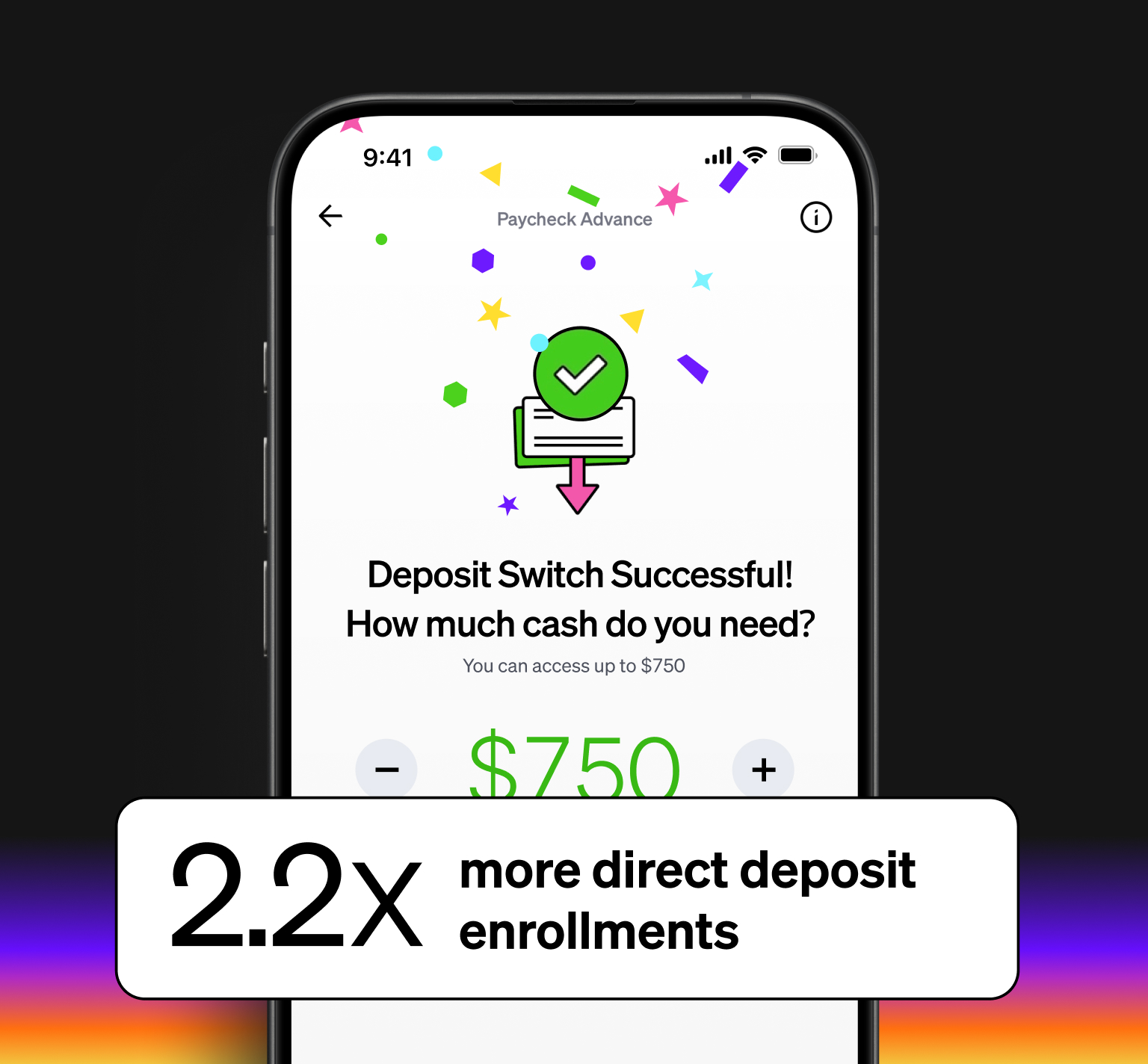

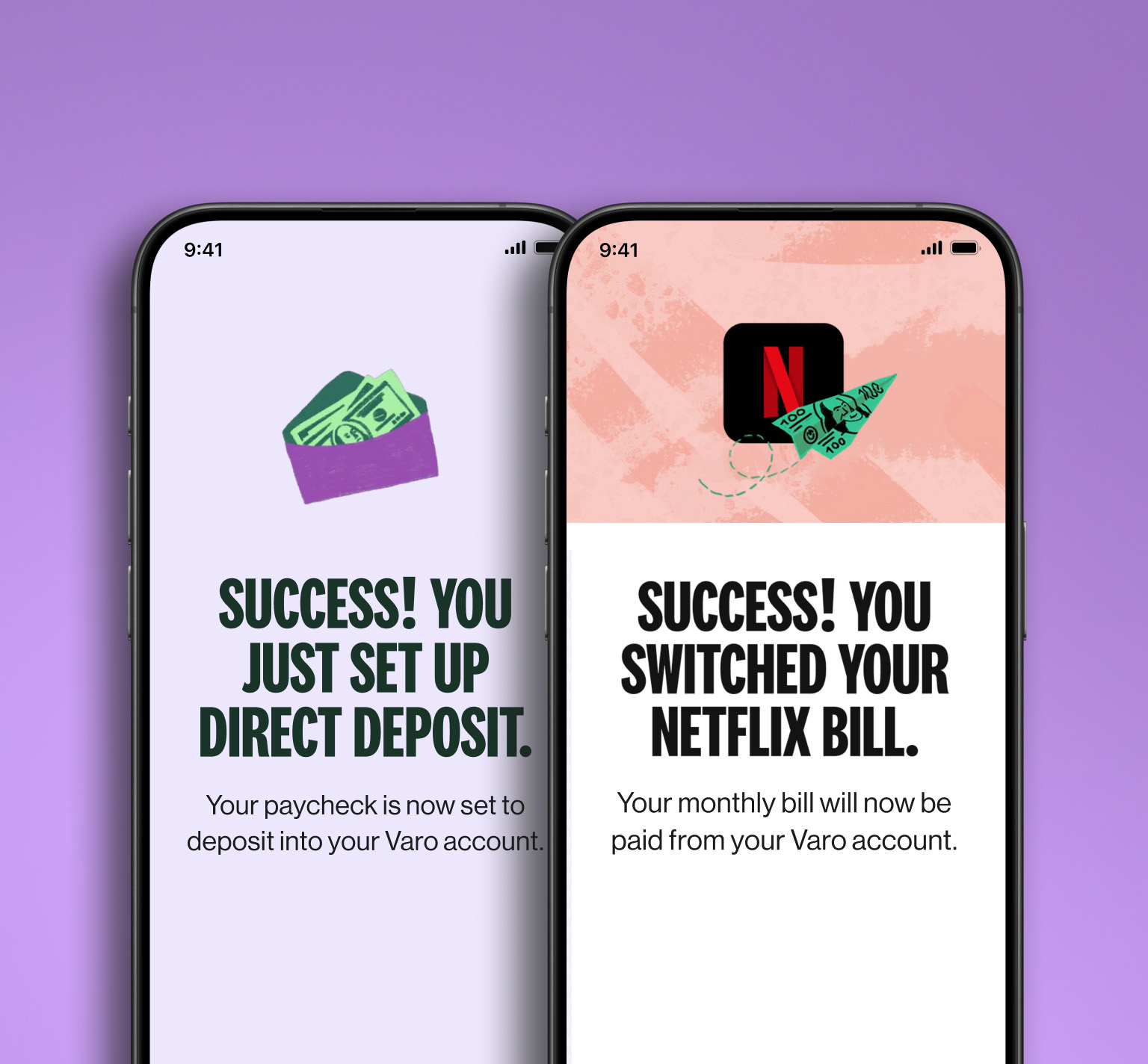

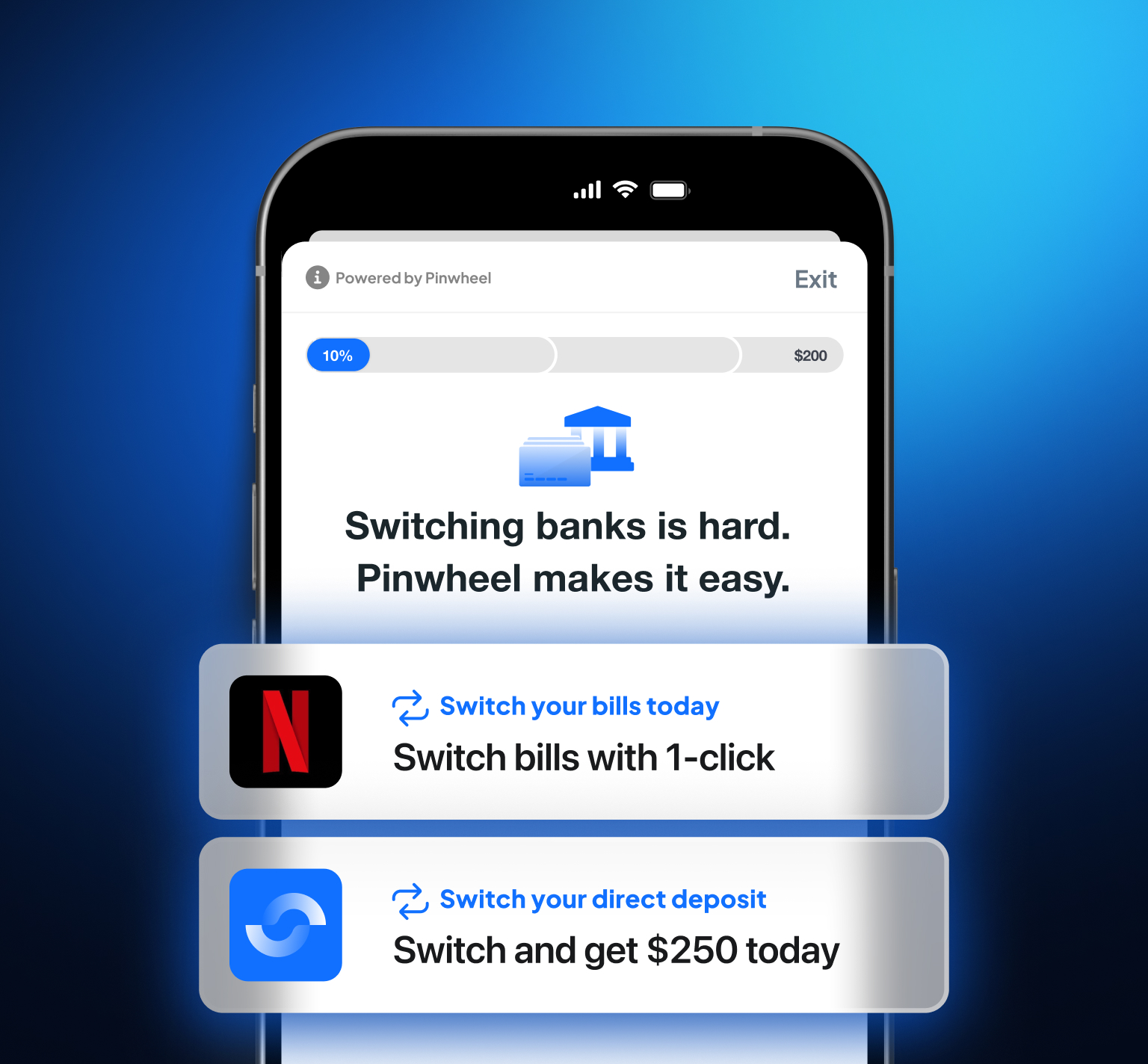

From the beginning, Pinwheel chose a more resilient path: securing direct data access partnerships that allow Pinwheel to read data from, and write data into, the income accounts of consumers at their request to provide them access to the financial services of their choice. Users in the Pinwheel PreMatch network can connect their income account to an app without searching for their account or entering in their username and password, automatically matching their income account and securely authenticating via a one-time passcode. While this approach required more upfront effort, it's yielded dependable, compliant, and consistent access. End-to-end conversion with PreMatch has exceeded the username and password approach by between 1.9 and 2.6x while live, head-to-head conversion competitions routinely deliver 30% more switches.

The Pinwheel model ensures:

- Stability: Our access is contractually defined, not vulnerable to political winds, differing authentication standards, or changed passwords.

- Security: We’ve built our infrastructure to exceed compliance standards and protect user data, which is encrypted front to back.

- Trust: Financial institutions and fintechs rely on Pinwheel as a secure, long-term partner as we continue to expand the PreMatch network, which now encompasses 45 million Americans.

What This Means for Fintech and Consumers

The CFPB’s withdrawal underscores a hard truth: regulatory frameworks can be fragile. For fintechs and platforms betting on enforced open access, it’s time to reassess.

At Pinwheel, we believe the future belongs to those who take initiative. We've built a better foundation, one that doesn’t just wait for change but actively enables it. As consumer demand for financial freedom continues to grow, so does the need for infrastructure partners who can provide resilient and high-quality access.

Want to build products on a reliable income data infrastructure? Let’s talk!