.svg)

.svg)

From digital wallets to automated deposit switching, banking APIs are everywhere. They’re so ingrained in the apps we use that the average person isn’t even aware they’re using APIs on a daily basis, whether it’s to send money or track their spending habits in a budgeting app.

In short, API banking solutions allow the transfer of data from financial service providers to third parties, powering new fintech solutions that are transforming the banking industry.

Sixty-eight percent of banks have already started implementing APIs in payments, while 48% have done so in lending. When it comes to APIs, one of the main focuses of banks in the Americas is developing new services and products in collaboration with fintech startups and third-party providers. But the use cases and benefits of banking APIs reach far beyond just expanding the product and service portfolio, both for traditional banks and fintechs — here’s the full rundown.

What are APIs?

API stands for application programming interface — an app that connects one software program to another.

There are 4 types of APIs:

- Open APIs — Also known as public APIs, they are APIs any developer can access.

- Partner APIs — Accessible externally, but only by approved clients. For example, Pinwheel is a partner API.

- Private APIs — Also called internal APIs, companies use them to streamline processes inside their teams. They are not available to third parties.

- Composite APIs — A combination of several APIs that allow you to get a single response from multiple servers.

Although APIs sound like a complex concept, they are a part of apps we use on an everyday basis. For example, when you order an Uber, the route displayed on the app is shown using a Google Maps API.

Uber and countless other apps rely on the use of APIs because they simplify the development of software programs. Instead of building out a virtual map from scratch, ride-sharing apps use APIs to connect to pre-existing maps.

Examples of API banking solutions

API banking solutions range from embedded financial services to APIs that enable consumers to share their financial data with third parties.

1. Embedded finance

Embedded finance refers to the integration of banking products by non-banking companies. In the past, banks and credit unions were the only ones who could offer banking services, such as debit and credit cards. But banking APIs allow any company to embed financial services into their product.

Take the ride-sharing app Lyft as an example. Its drivers can get the Lyft Direct debit card which allows them to get instant access to their earnings. But Lyft didn’t build this feature from the ground up. Instead, the company partnered with Payfare, a digital banking provider that designs APIs which integrate with gig platforms. With Payfare’s APIs, companies can launch banking products in as quickly as two months.

Another example of embedded finance solutions is Squire, a booking and payment platform for barbershops. In collaboration with Bond, a Banking-as-a-Service company, they designed a Squire Card where barbers can access their tips and commissions.

Banking-as-a-Service (BaaS) companies, such as Bond, make embedded finance possible. BaaS providers partner with financial institutions to provide banking products to third parties via APIs. Companies leverage BaaS APIs because they are a faster alternative to developing financial products in-house alongside a partner bank. For example, Bond says that Squire would’ve needed anywhere from 18 to 24 months to build their card solution with a bank, compared to just a couple of months with Bond.

2. Payroll connectivity

API banking solutions don’t stop at debit cards. Payroll data connectivity APIs allow banks and fintechs to connect to their customer’s payroll accounts and other income sources, like gig and creator platforms. By connecting to payroll and income platforms, financial service providers can automate processes and launch new products.

When it comes to automation, payroll APIs can improve how banks and fintechs verify income and employment. Instead of clients having to manually submit pay stubs or W2 forms, they can authorize the API to retrieve this data on their behalf. Fintechs and banks can then use customer data to improve loan underwriting and verify the client’s identity to prevent fraud. However, APIs that connect to payroll and income platforms have applications beyond the banking industry. Proptech companies are also integrating them to expedite the tenant screening process.

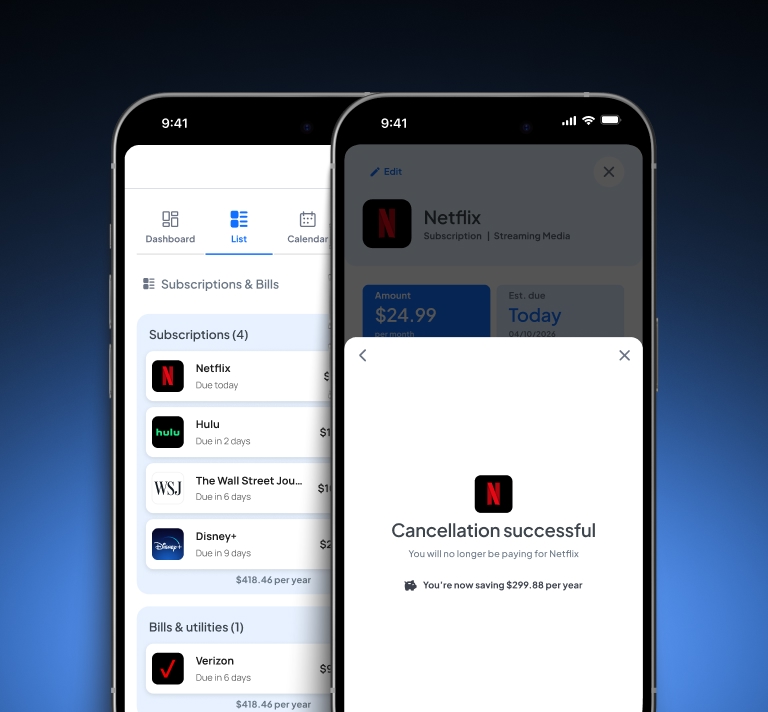

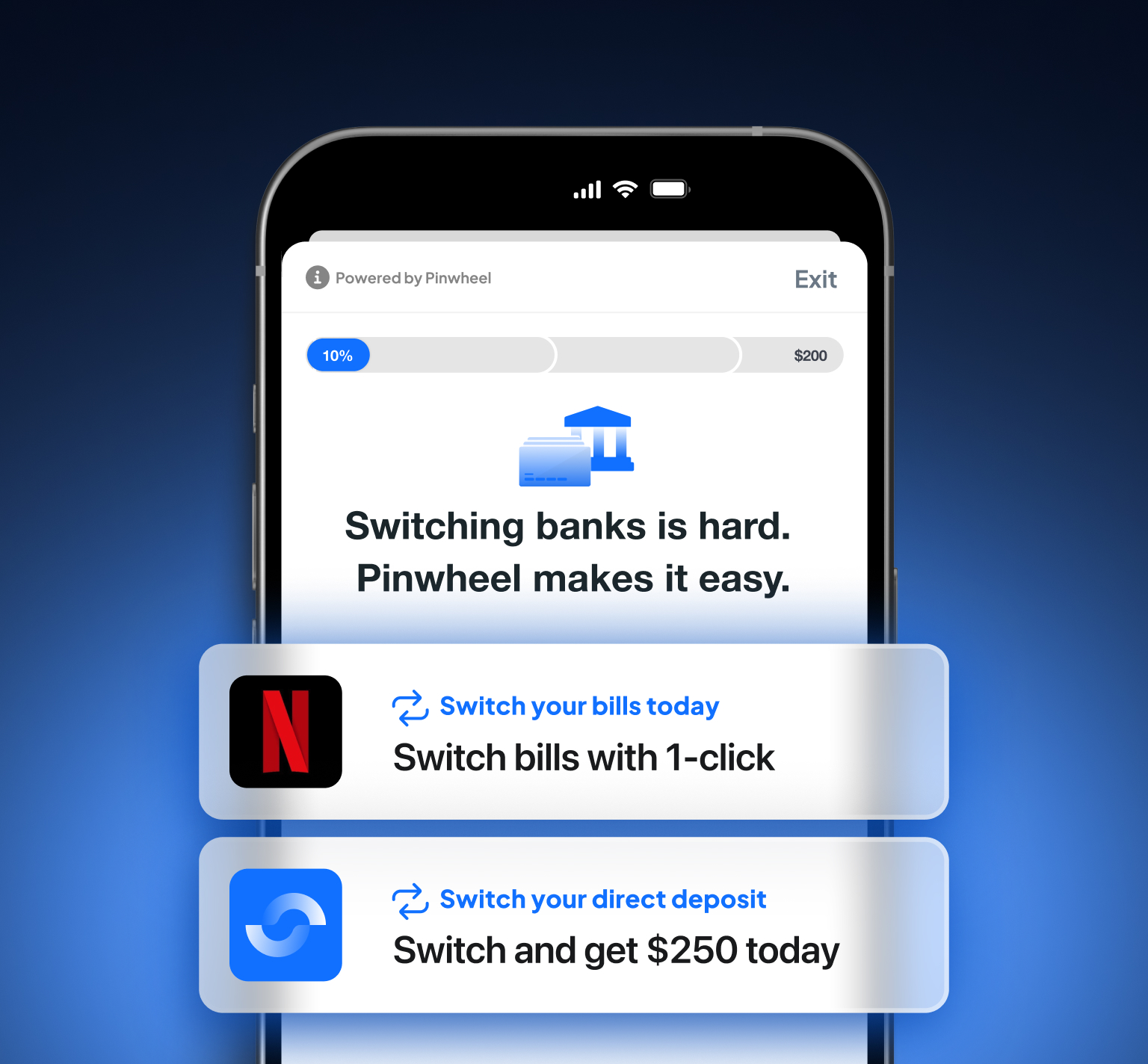

Direct deposit switching is another process that payroll APIs can automate. Rather than asking their clients to update their direct deposit with their employer, fintechs and banks can integrate a single API to do the work. The client can update their settings in-app, which is a vast improvement over the manual process and improves the customer experience. Financial service providers also benefit from increasing direct deposits. One neobank grew direct deposits by 20% in the first month after implementing Pinwheel’s payroll connectivity API.

API-enabled payroll connectivity also opens doors to innovation. Payroll data can power services such as earned wage access, which allows employees to withdraw their wages at any time. Pinwheel’s API has access to shifts and paystubs data as well as the top 20 time & attendance platforms covering 25 million hourly workers in the U.S., which is essential for calculating the amount of available wages. Together with our earned wage access estimation model, fintechs and financial institutions can swiftly launch an earned wage access product without having to connect to each payroll or income platform.

3. AI-powered financial management

Financial technology APIs are also driving money management solutions that use artificial intelligence (AI) to help users save and budget. A banking API can retrieve transaction data from a customer’s bank account, which the financial management app then uses to segment expenses, make recommendations, or alert the user when they spend too much.

Cleo, an AI financial wellbeing app, relies on Plaid’s API to allow users to connect to their bank accounts. With the connection in place, the AI assistant uses transaction data to help users follow their budget and increase their savings. By integrating an API that’s already connected to banks, Cleo doesn’t need to invest in developing this functionality on its own.

The benefits of APIs in banking

At a high level, banking APIs lay the foundation for innovation while lowering costs.

Benefits to traditional banks include quicker innovation, better productivity and efficiency, and improved user experience, according to a Finastra report. Quicker innovation is crucial, considering neobanks and other consumer-facing fintech companies are working hard on growing and retaining their consumer base. By 2024, there will be 47.5 million bank account holders at digital-only banks in the U.S., so being able to introduce new features quickly can help banks remain competitive.

Additionally, an Accenture report found that banks that “embrace the new API-driven Open Banking initiatives“ could potentially increase their revenue by 20%.

Fintechs can also benefit from important advantages, especially when it comes to going to market faster with new products while keeping costs to a minimum. For instance, Envel, an AI mobile banking app, was able to automate direct deposit switching in just a few weeks using Pinwheel’s API.

Cybersecurity and banking APIs

Banking APIs enable data sharing that brings convenience and innovation to financial services. But APIs can also pose a risk if they have a low level of cybersecurity. Attacks can include the use of stolen credentials, distributed denial-of-service (DDoS) attacks, man-in-the-middle (MitM) attacks, and others that can compromise infrastructure and sensitive data.

An essential aspect of API cybersecurity is to prioritize it while developing the API, instead of putting it on the backburner. The process includes implementing security measures such as Transport Layer Security (TLS). TLS is an encryption protocol that secures the data exchange between servers and applications and can also encrypt communications over email or messaging apps. Pinwheel’s API security, for example, includes both TLS and the Advanced Encryption Standard (AES 256). AES is approved by the National Security Agency (NSA), and the 256-bit type provides the highest level of protection.

Before they implement any API banking solution into a product, financial institutions and fintechs should carefully consider the cybersecurity measures and credentials of the vendor to protect themselves and their clients.

Banking APIs are continuously redefining financial services

Thanks to banking APIs, consumers and businesses have access to financial solutions that are more convenient than ever before. Meanwhile, financial service providers can design new products and services without pouring time and resources into connecting to various data sources.

As we’ve moved from open banking to open finance — a system where consumers can share access to all kinds of financial information — banking APIs have evolved to connect to data sources that don’t only include banks.

Payroll data connectivity APIs are a prime example, as they connect to payroll and income platforms which contain important information regarding a consumer’s income and employment. Opening access to payroll and income platforms allows financial institutions to branch out into paycheck linked lending and improve underwriting models with verified employment data.

With more data, financial service providers can better get to know their customer base and develop solutions that are tailor-made for their audience.