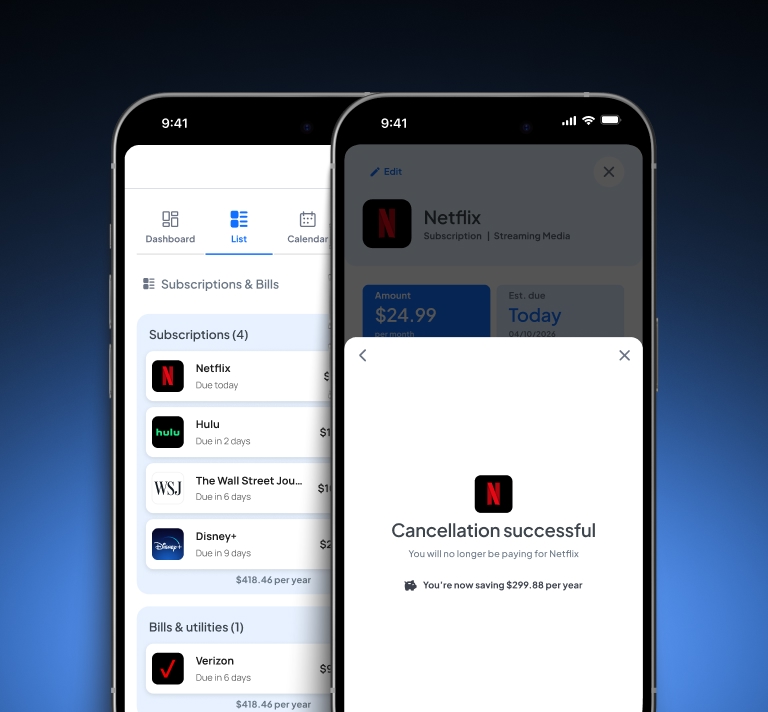

Through a new collaboration with Pinwheel, Visa's Enhanced Subscription Manager lets cardholders view, switch, and cancel subscriptions—right inside their banking app.

FEATURED

Visa Launches Enhanced Subscription Manager, Giving Consumers Greater Control Over Recurring Payments

Read more ➔