.svg)

.svg)

Financial institutions have had exclusive control over customer information for a long time. Traditionally, when someone had to apply for a loan or open a new bank account, financial institutions asked customers to provide a significant amount of personal and financial information.

Although this collection of information was necessary to offer better products and services, it also meant that financial institutions were in firm control of customer information — including how to use and share it.

The presence of technological and legal barriers meant that customers found it hard to access this information and were unable to share it with third parties seamlessly. But over the last few years, technology has advanced to an extent where it’s now possible to remove these roadblocks, especially with the arrival of APIs.

An open finance ecosystem ensures that all participants of the financial system — traditional financial institutions, fintech companies, and consumers — can use APIs to share data. This democratization of financial data can help financial institutions and companies to generate more revenue by personalizing their financial services, while consumers are awarded more flexibility with how they share data and can improve their financial wellness by using smarter financial products and services.

What is open finance?

Open finance refers to a financial ecosystem that allows people to control their financial information and share it with financial service providers in exchange for tailored products and services.

Open finance is an extension of open banking. But while open banking only shares payments and basic financial data, open finance shares more data types. It includes bank transactions, loans, money transfers, investments, insurance and retirement accounts, savings, payroll, digital wallet spending, etc.

There are three principles that govern how open finance works.

Data access

Data access refers to providing individuals access to transactional and personal information that a financial entity has collected over time.

It involves granting customers property rights of their information. Conversely, data access can also be provided by placing an affirmative obligation on a financial institution that binds it to deliver customer information when a customer requests it.

Data portability

Data portability refers to transferring financial data between two systems without re-entering them. It’s classified into two types:

- Export portability: This empowers customers to manually download and upload their information whenever they would like to share it with others. Customers can log in to the information system of a financial institution and download their latest transactional and personal data. Next, they can upload this snapshot to other institutions.

- Platform portability: Platform portability refers to using an electronic interface to exchange customer data between two financial institutions.

Data interoperability

Data interoperability refers to developing standardized protocols that enable information systems to retrieve a relevant piece of customer information and receive that information in the specified format. This is done through APIs that use a common set of rules, messaging formats, data standards, and procedures that allow communication between information systems.

To put it simply, APIs are the syntax, grammar, and language that allow these systems to define the type of data that one can request and retrieve, how they can do it, and specify the format for the target system.

How can open finance reshape financial products and services?

The use of APIs offers a wide range of financial use cases.

Optimize the mortgage approval process

Often, customers find the mortgage approval process time consuming and unclear. It can take anywhere from several days to around a month. Besides, manually comparing different providers isn’t convenient.

Open finance can cut the number of steps involved in the mortgage application process. This is done through the help of APIs that allow credential-free and tokenized sharing of data between mortgage lenders, mortgage buyers, and mortgage brokers. These APIs support real-time analytics and enable customers to have comprehensive control of the type of data they are looking to share.

While searching for mortgage products, customers can use software powered by open finance APIs to get tailored recommendations based on the user’s financial data (e.g., household income).

For example, Houzy is an online platform for homeowners. It uses Mortgage Offer API to help users compare mortgages. The API collects information, such as details of the borrower, household income, and desired financing structure (e.g., amount, start date). After analyzing this information, it returns an indicative mortgage offer for the user.

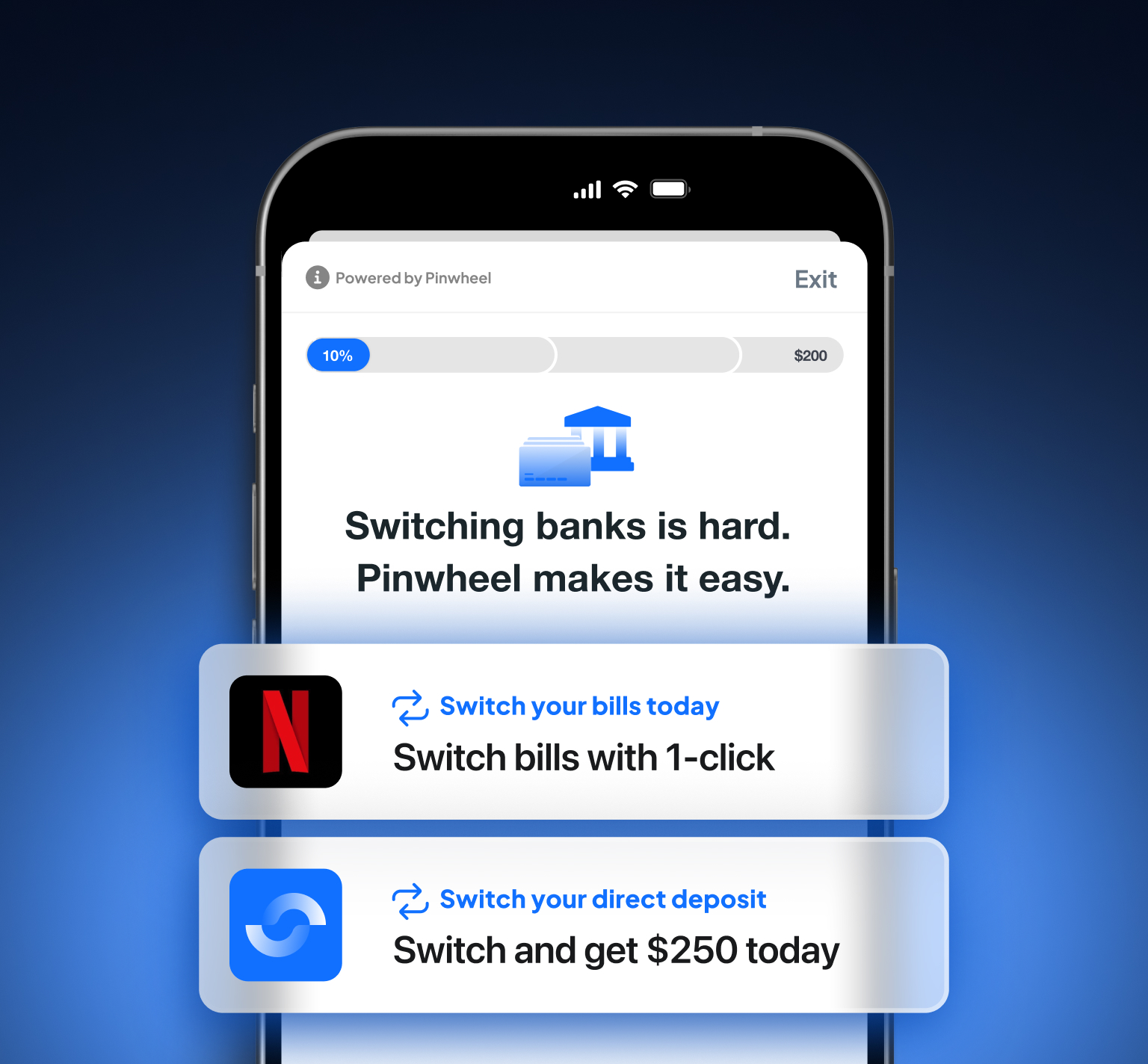

In addition to the mortgage approval process, APIs can help lenders improve their underwriting models with additional financial data. Pinwheel’s API connects to more than 1,500 payroll and income platforms, retrieving consumer-permissioned data that lenders can use to determine a borrower’s risk and easily verify their income and employment.

Increase savings

Open finance solutions can improve people’s financial wellness by automating budgeting and saving.

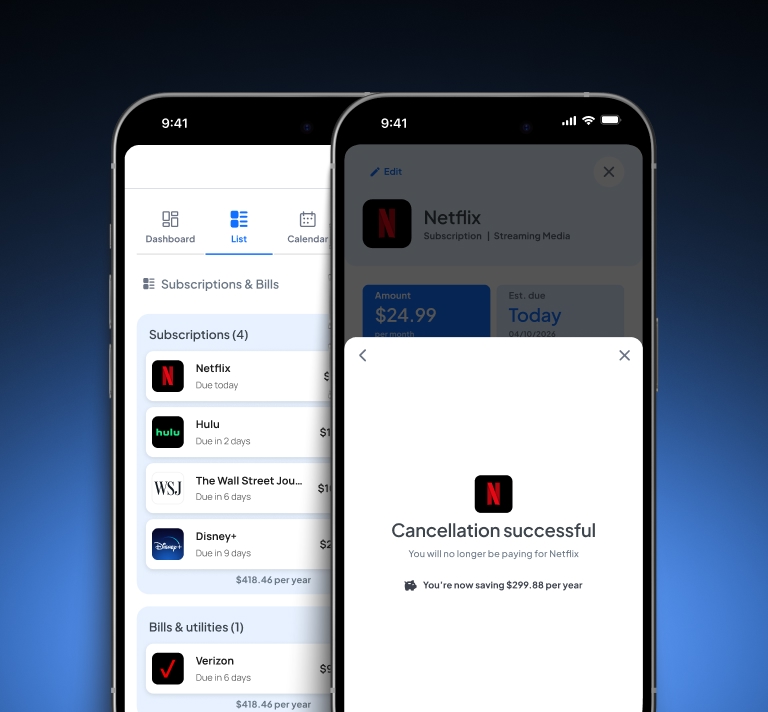

For instance, a consumer can use an app powered by an API to sweep all or some of the cash left from their last salary into a savings account. Or they can cut down on their monthly spending (e.g., by canceling multiple subscriptions) and send that money to a savings account.

These solutions include apps like Cleo that provide consumers with insights into their spending habits and savings. Cleo uses an AI-powered chatbot that can help users set goals to reach their savings target, automatically detect how much they can save, and send that amount to their savings account.

Earn customers’ trust in your financial product with a secure API

For all their benefits and convenience, consumers might hesitate to adopt open finance solutions because they’re unsure about a financial service provider’s ability to protect their sensitive information. Pinwheel has developed a payroll data connectivity API that can protect consumer data with a number of advanced security features. These are:

- Encryption: Pinwheel protects customer data by using industry-standard encryption. Encryption is applied to both data at rest and data in motion. This includes the use of Advanced Encryption Standard (AES) 256-bit and Transport Layer Security (TLS) to encrypt customer data.

- Independent security assessments: Pinwheel performs regular security assessments of its services. This includes hiring third parties to review compliance and certifications, such as for SOC 2 Type 2. Twice a year, Pinwheel systems undergo penetration testing to test for exploits, including access controls, SQL injection, and XSS.

Learn more about it here.