.svg)

.svg)

New data from Pinwheel’s 2026 Consumer Banking Sentiment Study exposes a stark generational divide—and why banks, credit unions, and fintechs can’t afford to ignore it.

For years, the conventional wisdom in retail banking has been that younger consumers are fickle, low-value, and difficult to serve profitably. Pinwheel’s ongoing consumer research tells a very different story. Gen Z and Millennial banking trends reveal a generation of customers who are highly motivated to engage with their financial institutions—if those institutions actually show up for them.

The 2026 Consumer Banking Sentiment Study, based on a survey of 500 U.S. consumers, offers some of the clearest generational data we’ve gathered to date. Paired with insights from prior Pinwheel research on bank switching behavior and primacy, a picture emerges: younger consumers are not difficult to win. They’re just waiting for someone to offer them something worth switching for.

The Subscription Blind Spot: Worst Among the Youngest

One of the most compelling findings in this year’s study is the dramatic gap between what consumers think they spend on subscriptions and what they actually spend. Across the general population, 42% of consumers believe they spend less than $25 per month on subscriptions. In reality, the average American spends $219 per month across more than eight active services, according to a 2026 Fortune Business Insights study.

But the blind spot is sharpest among the very consumers spending the most. Gen Z and Millennial banking behavior in 2026 is defined, in part, by this paradox:

The inversion is striking: the generations spending the most are the least aware of it. And the consequences are tangible and immediate.

These are not edge-case outcomes. They are mainstream experiences for Gen Z and Millennial banking customers. Every overdraft fee triggered by a forgotten streaming service is a failure of the banking relationship—and an opportunity for a more attentive institution to step in.

The Subscription Blind Spot: Worst Among the Youngest

Pinwheel’s 2024 consumer research found that 73% of all consumers had considered switching banks in the prior 12 months, challenging the long-held belief that most consumers bank for life. That switching energy is even more pronounced among younger cohorts—and the 2026 data shows exactly what would trigger it.

When asked whether they would move the majority of their bill payments to a bank account that offered subscription monitoring and cancellation tools, the response from Millennials was decisive:

This matters because bill payment consolidation is the most durable form of banking primacy. Earlier Pinwheel research established that winning direct deposit is not enough—true primacy requires becoming the account from which customers pay their bills. Millennials are telling us, loudly, that they will make that switch for an institution that helps them manage their financial life more intelligently.

The willingness to share data is equally significant. Sixty-six percent of consumers say they would link external accounts to access subscription management at their primary bank—a figure that speaks to how much trust younger consumers are willing to extend to institutions that demonstrate genuine utility.

Fintechs have won Gen Z—but the battle for Millennials is still on

The 2026 study’s primacy data shows that fintechs now hold 12% of primary banking relationships in the general population. Among younger and middle-income consumers, that share is likely higher. But here’s what’s interesting for banks and credit unions competing for Gen Z and Millennial customers: holding a primary relationship today does not mean holding it tomorrow.

Prior Pinwheel research found that 40% of new accounts acquired through promotions are never activated—a persistent inactivity problem driven not by consumer apathy but by friction. Consumers told researchers the top barriers to account activation were the 3–5 day delay in transferring money from an old account, no easy way to change direct deposit, and the hassle of switching recurring payments.

For Gen Z banking trends in 2026, those friction points are deal-breakers. This generation expects mobile experiences as seamless as any other app they use. Pinwheel’s 2024 research found that 70% of all consumers would be more likely to switch banks if they could transfer their direct deposit digitally in seconds—a figure that skews even higher among younger consumers.

The implication for millennial banking and Gen Z banking strategy is clear: features matter more than bonuses. The 2024 data showed that only 39% of consumers said account opening incentives would motivate a switch, while 56% cited better products and services as the reason they considered leaving their current institution. Younger consumers are not looking to be bribed. They’re looking to be helped.

What winning Gen Z and Millennial banking relationships looks like in practice

Taken together, the 2026 consumer data and Pinwheel’s historical research paint a coherent picture of what meaningful Gen Z and Millennial banking engagement looks like. Here’s what financial institutions should prioritize:

Make subscription visibility a core feature, not an add-on. Gen Z and Millennials are bleeding money through subscriptions they’ve forgotten about, and they know it. An institution that surfaces these charges, flags anomalies, and enables easy cancellation is not just offering a feature—it’s offering financial protection. For any institution competing in millennial banking, solving this first financial management need can unlock a lifetime of loyalty and expanded services like savings, investments and brokerage accounts down the road.

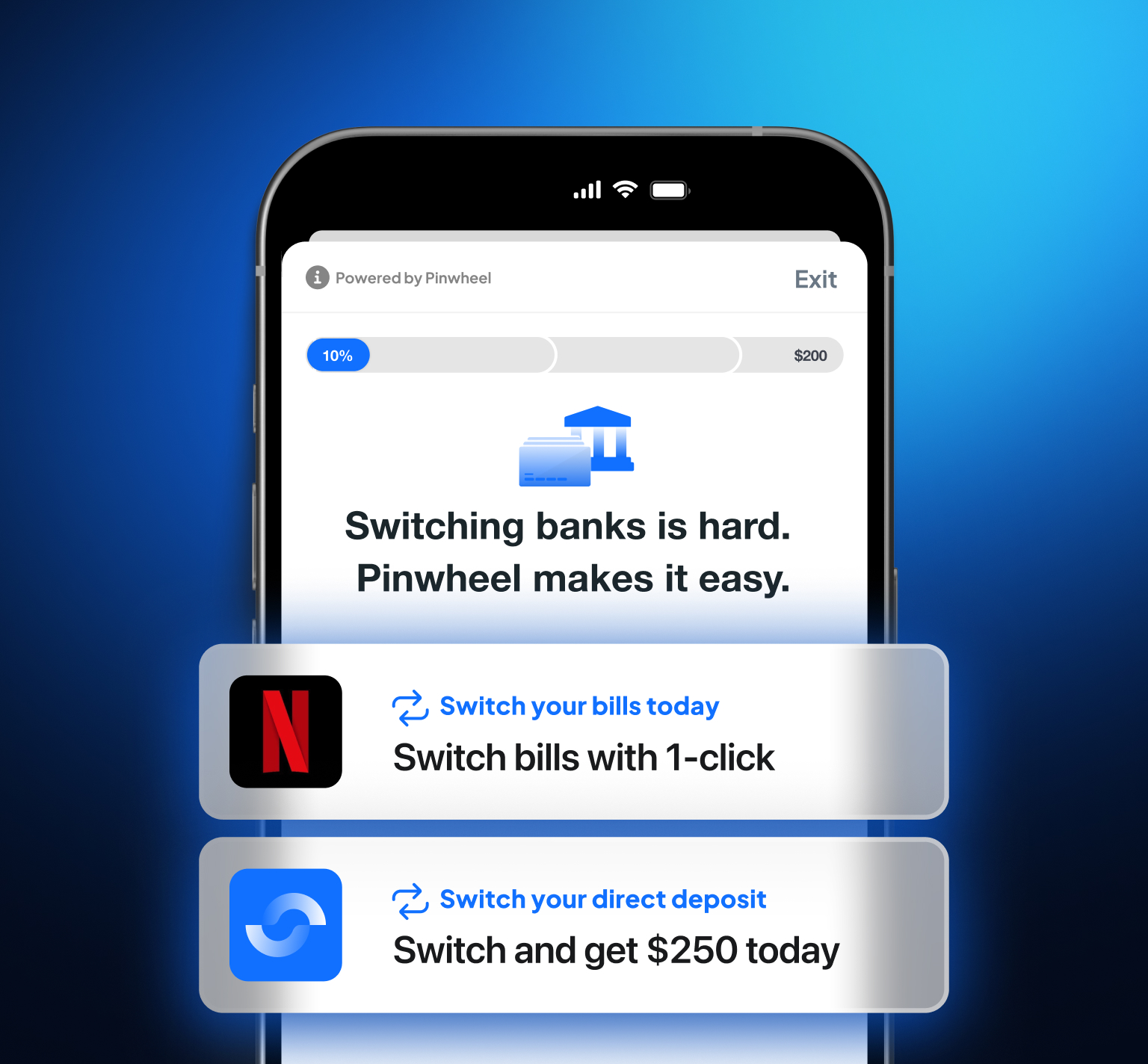

Eliminate switching friction entirely. The data from prior years is unambiguous: the biggest barrier to winning younger customers is not the offer—it’s the process. Instant direct deposit switching and seamless bill payment migration are table stakes for any institution serious about Gen Z banking acquisition in 2026.

Build for bill-pay primacy, not just payroll capture. With 74% of Millennials willing to move their bill payments to an account with better subscription tools, the path to full primacy runs directly through recurring payment management. Financial institutions should design onboarding journeys that explicitly move customers from direct deposit to consolidated bill payment.

Use data to personalize—but earn that right. Pinwheel’s 2024 research found that 69% of consumers expected their bank to use personal data to make processes like direct deposit setup easier. Younger consumers want smart, personalized banking. They will share data with institutions that use it thoughtfully and transparently.

Price premium features monthly. The 2026 study found that 53% of consumers willing to pay for subscription management would pay $5 per month—and that monthly pricing outperforms an equivalent annual fee in perceived value. For Gen Z and Millennial banking products, a monthly premium tier is both more palatable and more effective than lump-sum pricing.

About Pinwheel | This post references findings from Pinwheel’s 2026 Consumer Banking Sentiment Study (n=500 U.S. consumers) and prior Pinwheel consumer research published at pinwheelapi.com, including the 2024 Consumer Bank Switching Behavior study (n=500, Savanta Research) and the 2025 Consumer Banking Sentiment Study.