.svg)

.svg)

Easy access to consumer banking data has been a key driver in innovation over the last decade. Companies that enable connectivity to banking data like Intuit, Fiserv, MX, Finicity, Yodlee, and Plaid have been the key factor in creating fintech as we know it and modernizing the financial services industry. Apps like Mint, TurboTax, Cash App, Robinhood, and more have been built on the foundations of bank account connectivity, letting consumers take control of their financial data and use it to access a range of products and services.

Payroll aggregation is the next step in the evolution of financial account connectivity, as it means retrieving income & employment data directly from the source and giving consumers the ability to edit their payroll account settings. More than 93% of US workers get paid via direct deposit, meaning that payroll systems sit at the top of the financial stack and are essential to painting a holistic view of a consumer’s financial life. Unlocking access to this information helps drive innovation that could better serve the millions of Americans left behind by our financial system due to antiquated processes and technologies. It provides meaningful benefits to users, including the abilities to:

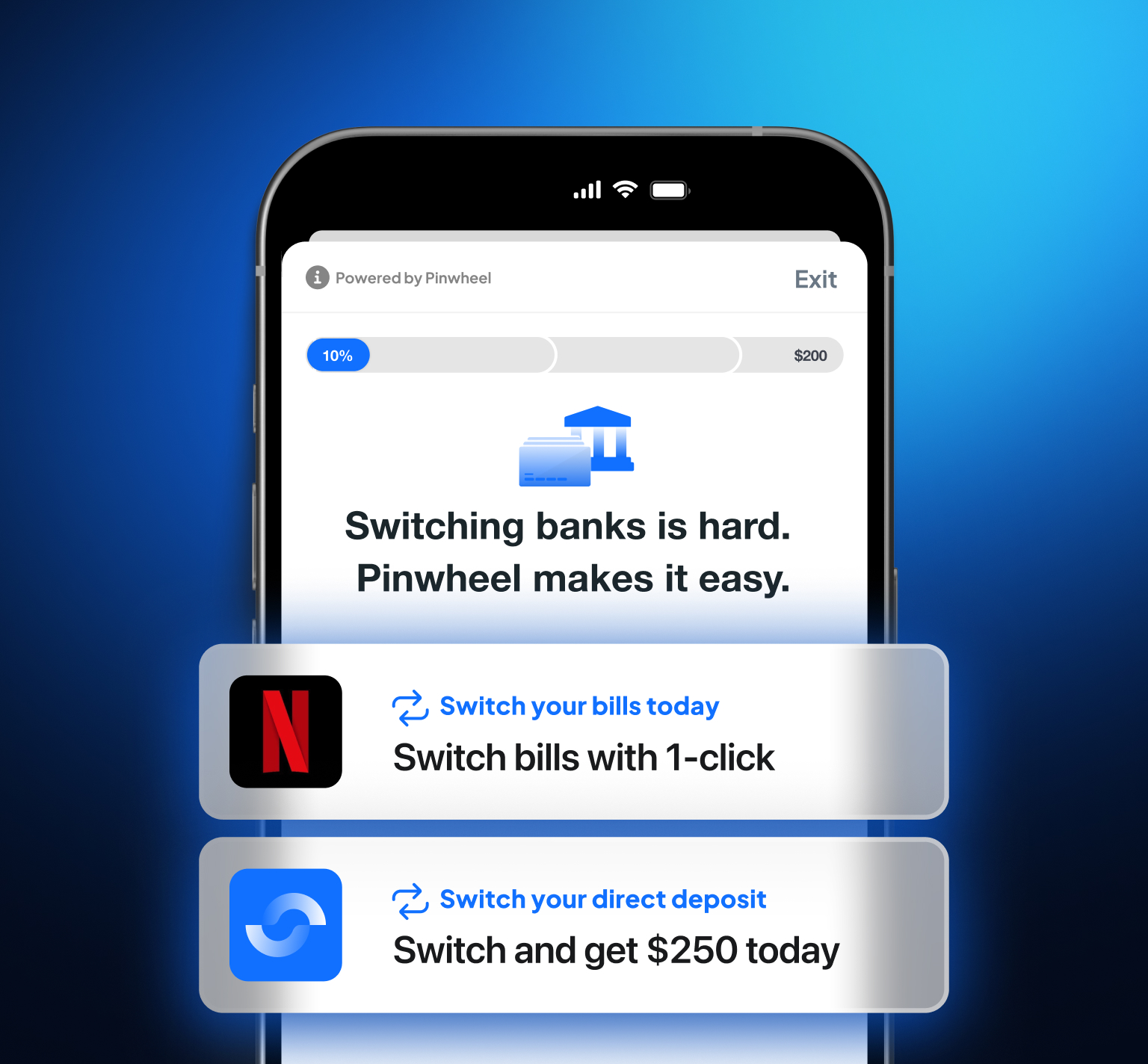

- Quickly and easily switch their direct deposit between financial institutions, taking control of their paycheck at the source and choosing the institution that offers them the best products and services.

- Share the wealth of income and employment data stored within a payroll system with financial institutions, unlocking lower-cost services. More than half of the population has a poor credit score or no credit score at all. The information in payroll platforms, like gross and net pay, length of employment, shifts, and title can be used by lenders to build a more complete profile of the borrower to expand their pool of serviceable applicants previously limited by underwriting models that only factor in FICO scores.

- Set up repayments directly from their paycheck, reducing risk for the lender and potentially unlocking even lower-cost loans

- And much more!

We’re grateful to be at the forefront of innovation in a space that is long overdue for widespread transformation, and to work with regulators in promoting consumer protection and financial inclusion.

Right now, The Consumer Financial Protection Bureau (CFPB) – the government agency formed by the 2010 Dodd-Frank Act and charged with holding financial institutions accountable for consumer protection – is in the middle of a consequential rulemaking process that will set the terms for how consumers can take control of their financial data in the future. Section 1033 of the Dodd-Frank Act directed the CFPB to draft rules that require a financial institution to grant consumers access to their data that is held by the institution. The law gives the CFPB considerable latitude to determine the details of these rules.

The CFPB put out a call for comments on Section 1033 late in 2020, and received almost 100 comments from industry groups and other stakeholders. Pinwheel holds the position, shared by consumer groups, industry peers, and the framers of the Dodd-Frank Act, that a consumer’s financial data belongs to the consumer regardless of the institution that holds it. The data on income and employment stored in payroll systems is financial information; given that classification and the significant benefits unlocking it can offer consumers, we believe the CFPB should make explicit the inclusion of payroll data in Section 1033. Doing so could help accelerate the innovation enabled by payroll connectivity, ultimately expanding access to financial products and services for all Americans.

Helping to build a fairer financial future is core to Pinwheel’s ethos. We’re excited to continue to work to achieve this with regulators, industry groups, partners and customers.