.svg)

.svg)

I have been talking to a number of friends and interview candidates about Pinwheel and while they conceptually understand our mission to create a fairer financial system, it isn’t until I explain to them that they fully grasp how large the scope of the problem we’re addressing and that it affects everyone, including them.

Let me explain...

When you take out a loan, apply for a credit card or rent or purchase a home, a credit check is run in your name and the resulting output is a FICO score. Your credit score serves as the onramp to obtain any quality financial product. Even during the loan or mortgage underwriting process, when additional information is considered, a lender will first and foremost look at your credit score.

Many Americans (nearly 40%) don’t even know their credit score and about a third don’t know what qualifies as a “good” credit score (670-739 is considered “good”, 740-799 is considered “very good” and above 800 is considered “excellent”). An even greater unknown for many is: what exactly goes into your credit score?

- Personally Identifiable Information (PII): this includes your name, Social Security Number, address, employer, and date of birth

- Credit Accounts: This portion makes up the meat of your FICO score. All lenders from whom you have taken out a lending product (think credit card, auto loan, mortgage) report metrics such as total credit line and payment history to date.

- Credit Inquiries: A list of everyone who has accessed your credit report within the last two years

- Public Record and Collections: If you have overdue debt that was sent to collections or have filed for bankruptcy, that information will appear here.

So, what’s missing? Your income - essentially your “revenue”, the item that dictates your ability to pay back the credit extended to you. Outside of the bank that receives your direct deposit, no other lender can automatically use your income in their underwriting process. Without that, lenders have to resort to approximation models based on piecing together imperfect demographic data. Whether it's buying your first home, getting a loan to cover an emergency medical expense, or buying a car to get you to and from work every day. Those are life-changing events, and they're too important to you to be contingent on a guess.

And that’s just the start. Because income isn’t included in your FICO score, you have to submit your pay stubs and employment verification entirely manually, a high-friction process subject to privacy breaches. This highly sensitive information often seems like it goes into a black box, leaving you with little control over your information or an understanding of your rate of borrowing.

We exist to make this entire system more transparent and effective.

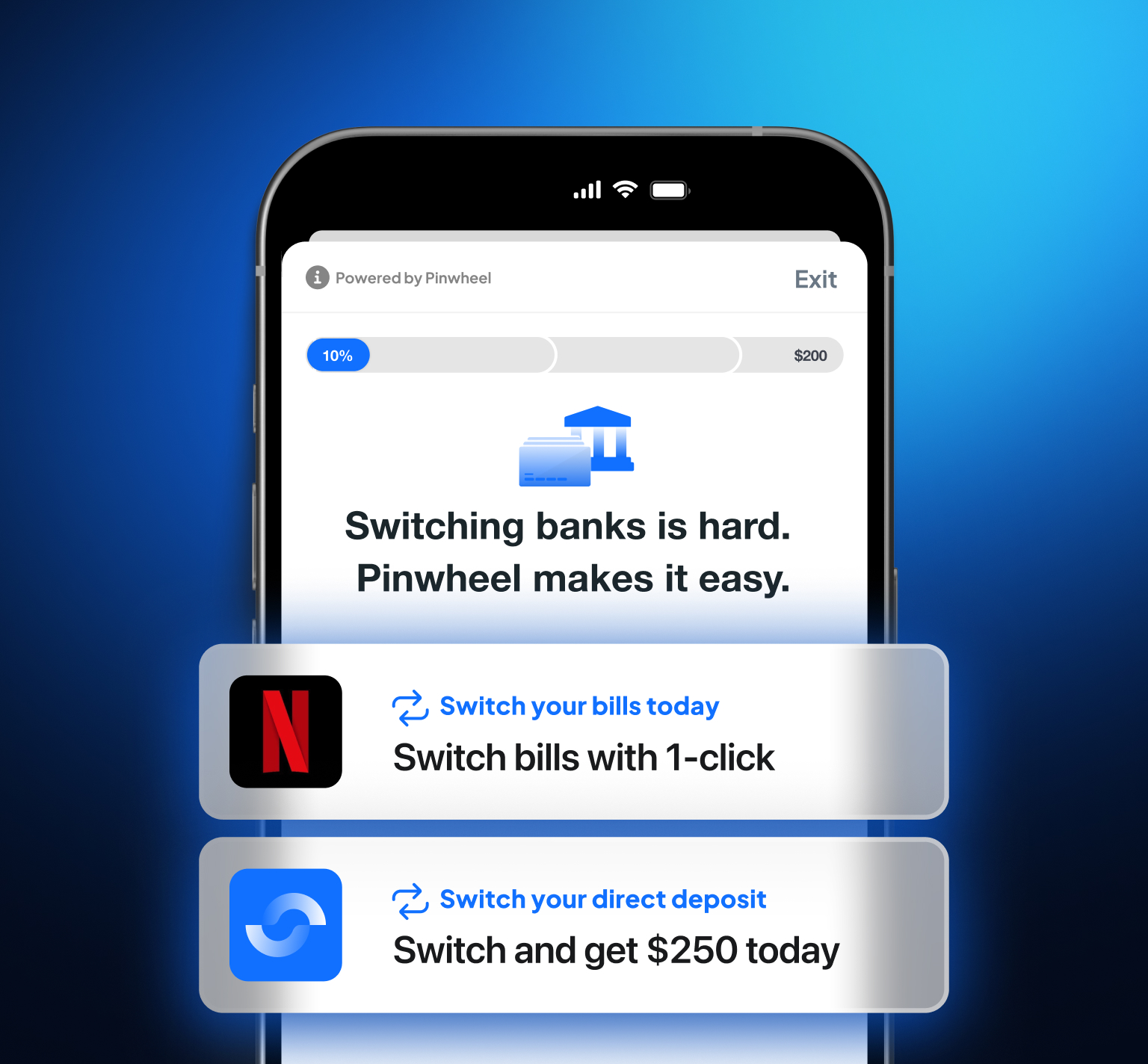

Through our API, we connect your employer’s payroll system to any application, from a lender to a financial institution to a savings application to...you name it. By easily making available income data and the systems to make payment directly from your paycheck, we can drive down APRs by significantly de-risking a loan, ultimately making a fairer financial system.

If you’re interested in learning more, check us out at Pinwheel.