.svg)

.svg)

Whether you’re a fintech or financial institution, payroll APIs are an important addition to your product. They allow you to make deposit switching easier, improve underwriting models, and branch off into new services like earned wage access. So partnering with a payroll API provider like Pinwheel, Atomic, or Argyle is bound to come up for consideration.

But selecting the right payroll data connectivity API can be tough. Many times we’ve heard from prospective clients that they can’t tell the difference between the three major payroll API providers. But the differences are there — and they’re not minor.

When shopping for a payroll API, it’s important to compare several key factors such as coverage, conversion, and security. And, of course, we can’t forget regulatory compliance since we’re dealing with private consumer data. With this in mind, here’s how Pinwheel’s API stacks up against others in the industry.

Payroll and income platform coverage

Coverage is the foundation of any payroll data connectivity API. Our clients can’t serve their customers if they can’t connect to their payroll or income platform. Pinwheel has coverage of 100% of U.S. workers, spanning over 1,800 payroll and income platforms, which is three times the industry average. We also cover 97% of the Fortune 1000, which employs 15-20% of all U.S. employees.

Our competitors lag behind in this aspect. Atomic covers 75% of U.S. workers and 450 payroll platforms, while Argyle also covers 75% of American workers with around 300 payroll and gig platforms.

Although we lead the way in terms of coverage, our team is constantly working to further expand it. Recently, we announced that we’d enabled connectivity to the top 20 time and attendance services (T&A) that 25 million American hourly workers use to log shifts. Connecting to T&A is crucial for enabling services such as earned wage access that allow employees instant access to their earnings.

Conversion rates

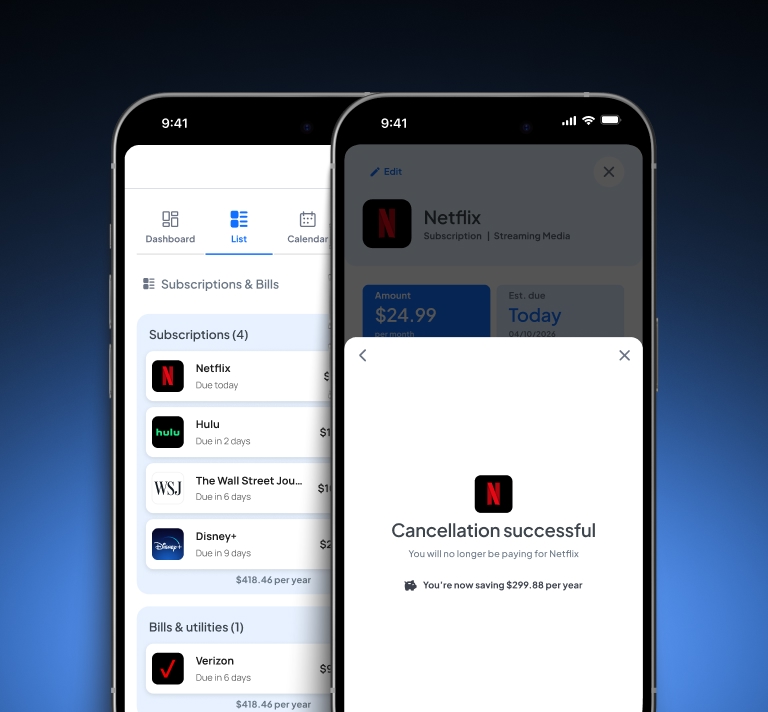

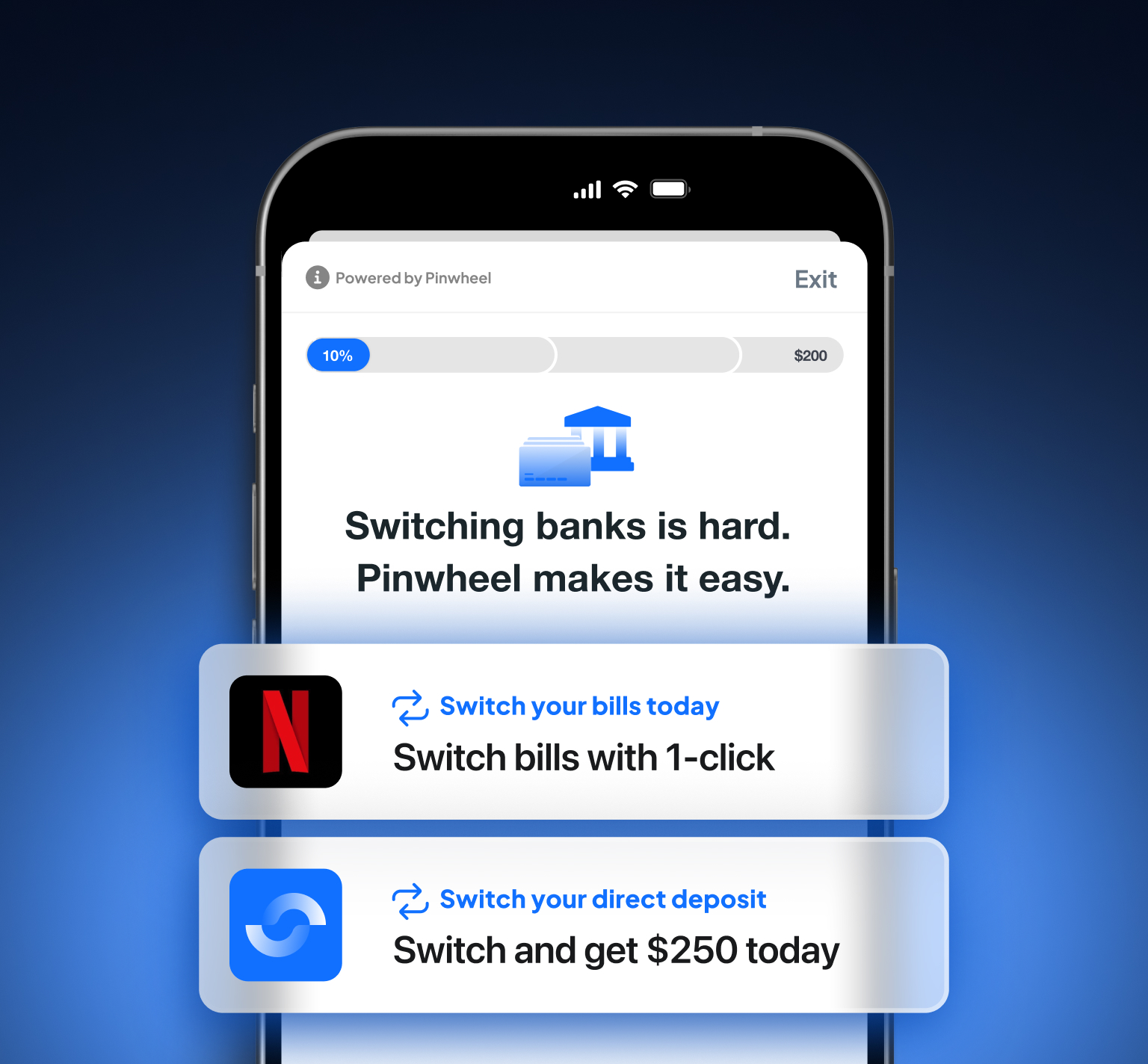

Financial service providers use payroll APIs to improve conversions, whether that means making a direct deposit switch or setting up a paycheck-linked loan. Pinwheel has faced off against other APIs in the industry, and we have a 100% win rate in head-to-heads against our competitors.

Our unrivaled conversion rates are a result of our seamless user flow or Link UX. Link shows users a list of the most popular payroll providers and employers to make it easy to sign up with minimal friction. Users can also rely on the search bar at the top of the screen to find their payroll provider.

We’ve also recently updated Link UX with a selection confirmation screen to eliminate any user confusion. For example, a user might select their primary bank instead of their employer or payroll platform. Before they confirm, a screen appears that asks them if they are an employee of the company they selected. If not, they can navigate back to find the correct one.

But we must also point out that conversion is a nuanced metric, and it should be evaluated at a more granular level. For instance, when it comes to direct deposit conversions, it’s best to measure direct deposit penetration growth — the percentage of users who decided to forward all or a portion of their salary into their account. One of Pinwheel’s neobank customers saw its direct deposits grow by 20% just one month after implementing our API. This metric is more meaningful when evaluating an API than blanket conversions because it has a direct impact on our clients’ business outcomes.

FCRA compliance

Consumer payroll data is sensitive and should be given every protection available under the law. That’s why Pinwheel is the only payroll data connectivity company that is a Consumer Reporting Agency (CRA). Our status as a CRA means our clients can use consumer permissioned data for credit decisions and remain compliant with the Fair Credit Reporting Act (FCRA).

The FCRA regulates how third parties (like credit bureaus) can aggregate and sell consumer financial data. It defines the information that third parties can collect and who is allowed to see it. Under the FCRA, consumers can also request access to this data, which lets them verify that the information is correct. For example, if a consumer applies for a loan and is rejected because of poor credit, they have the right to request their credit report. Each FCRA violation (such as providing inaccurate or old information) carries a $100-$1,000 fine. But some violations have resulted in multi-million dollar penalties, making FCRA compliance a priority for every financial service provider.

Payroll data connectivity companies like Pinwheel, Atomic, and Argyle aggregate information that other companies use to approve consumers for credit products. Although we don’t make any credit decisions directly, if our data is bad, that could have an adverse effect on the consumer. As such, we should stand behind the quality of our data and be liable if it leads to bad outcomes — and being a CRA helps us do that.

Other companies in the payroll space simply advise their clients to comply with FCRA without offering them the tools to do so. Only Pinwheel has created legal and operational frameworks to make it easy for our clients to be FCRA compliant. We’ve also set up an FCRA end-user portal where consumers can access their data and, if necessary, file a dispute.

Pinwheel’s API is backed by a world-class team

The reason Pinwheel was able to build an API with superior coverage and data quality is our people. We sourced our team from some of the best companies in the industry, such as Plaid, so building API products is ingrained in our company’s DNA. That’s why we’re improving our data quality around the clock and have ecosystem partnerships in every banking vertical to help our clients reduce costs and decrease time to launch. And our uptime is 99.999%, even at the highest monthly volumes.

As the only payroll data connectivity company with a Chief Information Security Officer, our team has built a platform where security is a priority. We’ve implemented bank-level encryption protocols and have a SOC 2 Type II certification — the most extensive SOC credential. From security to regulatory compliance, we’ve developed a payroll API platform that checks all the boxes and is ready to propel financial services into the future.